After several years of turbulence, the global cruise industry has found its rhythm again. Pricing power remains firm, onboard spending is rising, and debt levels are moving lower. As of November 2025, global cruise capacity is on track to reach an all-time high, yet profitability remains strong due to disciplined pricing and healthy demand across key markets.

The Gainify Cruise Stock Tracker spotlights seven cruise stocks shaping this new phase of growth, ranging from large operators expanding their fleets to service providers powering the onboard guest experience.

To find stocks like that, just use the Gainify stock scanner and filter by “Hotels, Resorts and Cruise Lines” under Industry.

Highlights: What’s Driving Cruise Stocks in 2025

- Record Capacity and Strong Margins: Global capacity growth is accelerating, while occupancy and yields remain above pre-pandemic levels.

- Onboard Revenue Expansion: Spending on premium dining, entertainment, and wellness continues to lift margins and customer lifetime value.

- Balance Sheet Recovery: Free cash flow generation is improving, allowing companies to reduce leverage and restore shareholder returns.

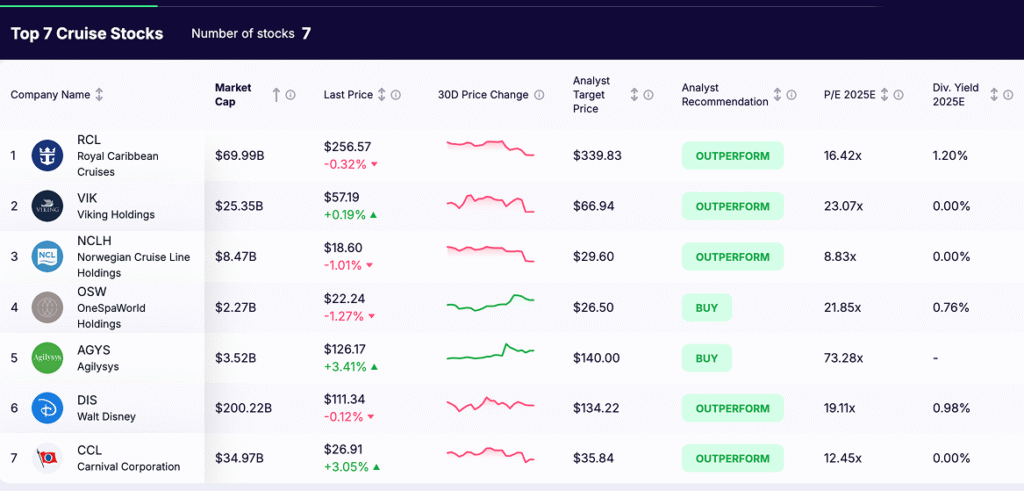

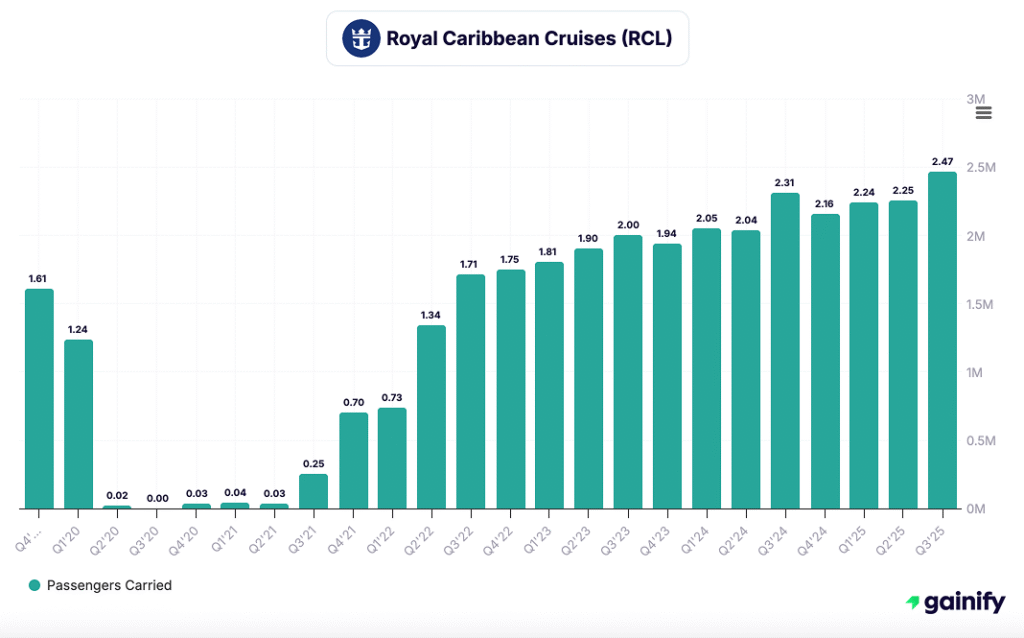

1. Royal Caribbean Cruises (NYSE: RCL)

Overview

Market Cap: $69.99B

P/E 2025e: 16.4×

Dividend Yield: 1.2%

FCF Yield 2.3%

Analyst View: Outperform

Royal Caribbean (RCL) operates the world’s largest and most profitable cruise portfolio, including the Oasis, Quantum, and Icon class vessels, as well as the Celebrity Cruises, Silversea, and TUI Cruises brands. The company’s scale, innovation pipeline, and premium customer base position it as the clear global leader in leisure cruising.

Investment thesis

RCL’s integrated model captures value across ticket pricing, onboard spending, and exclusive destinations, driving sustained margin expansion. Its fleet renewal strategy emphasizes large, efficient ships that deliver high per-berth economics and superior guest satisfaction. Continued yield growth, capacity optimization, and balance sheet deleveraging underpin the next leg of earnings compounding, with management guiding for sustained mid-teens ROIC and steady free cash flow growth through 2026.

Latest developments

In Q3 2025, Royal Caribbean reported adjusted EBITDA of $2.3 billion, up 7% year over year, and adjusted EPS of $5.75, both ahead of expectations. Net yields rose 2.4% year over year in constant currency, with full-year growth now guided between 3.5% and 4.0%. Occupancy remained above 105%, reflecting robust close-in demand. Management maintained its 2025 EPS outlook of $15.58–$15.63, representing roughly 32% year-over-year growth. Cash generation remains strong, supporting ongoing deleveraging and dividend reinstatement. The group continues to expand its fleet with upcoming launches such as Star of the Seas (2025), Legend of the Seas (2026), and Celebrity Compass (2027).

Key risks and catalysts

Fuel price volatility, foreign exchange, and broader economic conditions could temper margin momentum. However, Royal Caribbean’s robust booking pipeline, pricing power, and fleet optimization provide strong visibility. Catalysts include upcoming ship debuts, expansion of the Perfect Day and Royal Beach Club destinations, and digital upgrades enhancing onboard spend per guest.

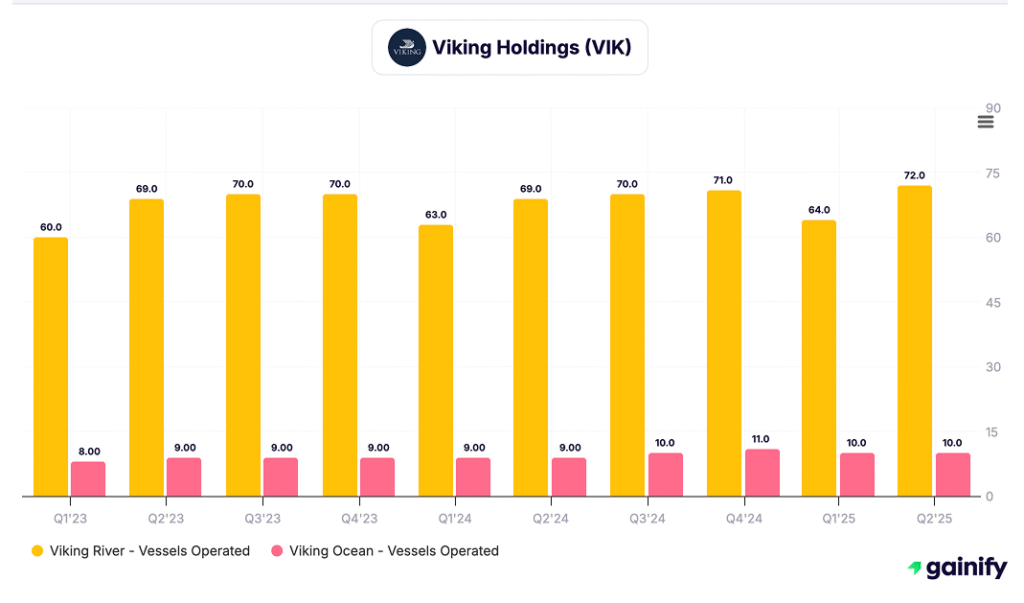

2. Viking Holdings (NYSE: VIK)

Overview

Market Cap: $25.35B

P/E 2025e: 23.1x

Dividend Yield: 0.0%

FCF Yield: 5.1%

Analyst View: Outperform

Viking Holdings (VIK) is a leader in river, ocean, and expedition cruising, catering to affluent travelers focused on cultural and destination-rich experiences. The company operates one of the youngest fleets in the industry, with 85 river vessels, 12 ocean ships, and 2 expedition ships, maintaining control or priority access to over 110 docking locations worldwide.

Investment thesis

Viking’s focused positioning in the upper-premium cruise segment provides durable pricing power, high occupancy rates, and efficient capital returns. Its asset-light design and relatively low cost of customer acquisition support above-average margins and free cash flow generation. Structural growth opportunities stem from expansion into Asia and India, alongside the scaling of its expedition fleet and investment in hybrid propulsion technologies, including the Viking Libra, which will become the first hydrogen-powered cruise ship in 2026.

Latest developments

In Q2 2025, Viking reported revenue of $1.88 billion, up 18% year over year, and adjusted EBITDA of $633 million, marking a 28% increase. Net income rose to $439 million, from $160 million in Q2 2024. Adjusted EBITDA margin expanded to 51.2%, supported by an 8% year-over-year increase in net yield and occupancy levels of 95.6%.

Key risks and catalysts

While Viking’s affluent customer base provides resilience, it remains exposed to geopolitical risks affecting European river routes and potential macro-driven softness in luxury discretionary spending. Key catalysts include continued expansion into new geographies, execution on hybrid energy initiatives, and further growth in expedition cruising. The company’s strong forward booking curve and disciplined capacity management position it well for sustained margin and free cash flow growth into 2026.

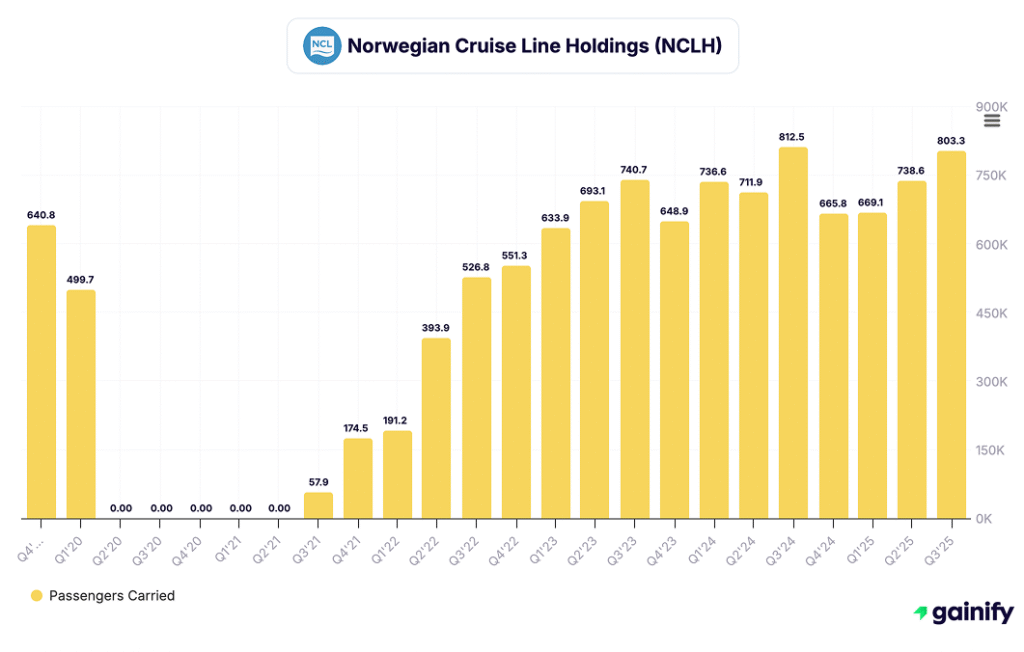

3. Norwegian Cruise Line Holdings (NYSE: NCLH)

Overview

Market Cap: $8.47B

P/E 2025e: 8.8×

Dividend Yield: 0.0%

FCF Yield: –12.7%

Analyst View: Outperform

Norwegian Cruise Line Holdings (NCLH) operates three distinct brands — Norwegian Cruise Line, Oceania Cruises, and Regent Seven Seas Cruises — spanning contemporary, premium, and luxury segments. The company manages 34 ships with more than 71,000 berths and has 13 additional vessels on order across its brands, supporting capacity growth through 2030.

Investment thesis

NCLH trades at one of the lowest valuation multiples among large-cap cruise operators despite ongoing improvements in load factors, yields, and cost control. The company’s diversified brand mix captures a wide range of customer demographics, from mass-market leisure to ultra-luxury travel. Strategic redeployment to the Caribbean market, where yields are stronger, and shorter-duration itineraries are more profitable, is driving operational leverage. Continued deleveraging, disciplined pricing, and fleet efficiency gains are key to restoring free cash flow generation from 2026 onward.

Latest developments

In Q3 2025, Norwegian delivered results ahead of guidance across all key metrics. Occupancy reached 106.4%, while net yield growth came in at 1.5% year over year.Adjusted EBITDA totaled $1.02 billion, and adjusted net income was $596 million, both slightly above expectations. Earnings per share reached $1.20, compared with guidance of $1.14. Management expects continued improvement in load factor and profitability into 2026, supported by a shift toward Caribbean deployment and ongoing fleet modernization.

Key risks and catalysts

Execution on debt reduction remains essential as leverage moderates from pandemic-era highs. Higher fuel costs and interest rates could weigh on near-term margins, but fleet renewal and stronger onboard revenue per guest provide offsets. The rollout of new vessels across all three brands, combined with enhanced onboard amenities at Great Stirrup Cay in 2026, could serve as catalysts for multiple expansion as cash flow normalizes.

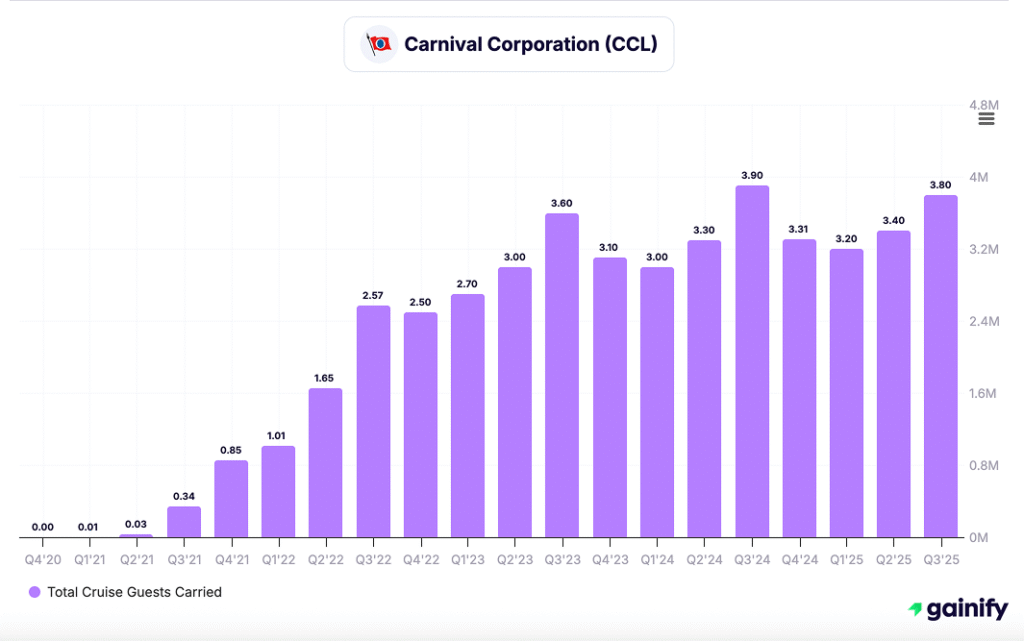

4. Carnival Corporation (NYSE: CCL)

Overview

Market Cap: $34.97B

P/E 2025e: 12.5x

Dividend Yield: 0.0%

FCF Yield: 9.6%

Analyst View: Outperform

Carnival Corporation (CCL) is the world’s largest cruise operator, with a global portfolio that includes Carnival Cruise Line, Princess Cruises, Holland America, Costa, and AIDA. After years of deleveraging and operational restructuring, the company is now in a period of renewed profitability and balance sheet strength.

Investment thesis

Carnival trades at a valuation discount to peers despite significant operating momentum. The company has regained full pricing power, with occupancy above pre-pandemic levels and onboard revenue per passenger at record highs. Its cost structure is improving through fuel efficiency gains and disciplined expense control. With net debt declining and return on invested capital reaching the low teens for the first time in nearly two decades, Carnival’s equity story is shifting from recovery to sustained cash generation.

Latest developments In Q3 2025, Carnival outperformed across all guidance metrics. Net yields rose 4.6% year over year, exceeding expectations, while adjusted cruise costs (excluding fuel) improved 5.5% versus 2024. Adjusted EBITDA reached $3.0 billion, and adjusted net income totaled $2.0 billion, beating guidance by roughly $120 million. Customer deposits hit a record $7.1 billion, reflecting stronger booking trends and pricing discipline. For full-year 2025, management raised guidance for the third time this year, now expecting $7.1 billion in adjusted EBITDA and $2.98 billion in net income.

Key risks and catalysts

Fuel cost volatility, higher interest expenses, and competitive capacity growth could weigh on margins. However, strong forward bookings, disciplined pricing, and refinancing at lower spreads support the near-term outlook. Sustained improvement in yields and leverage ratios could drive a re-rating toward historical valuation levels as Carnival transitions to a consistent free cash flow compounder.

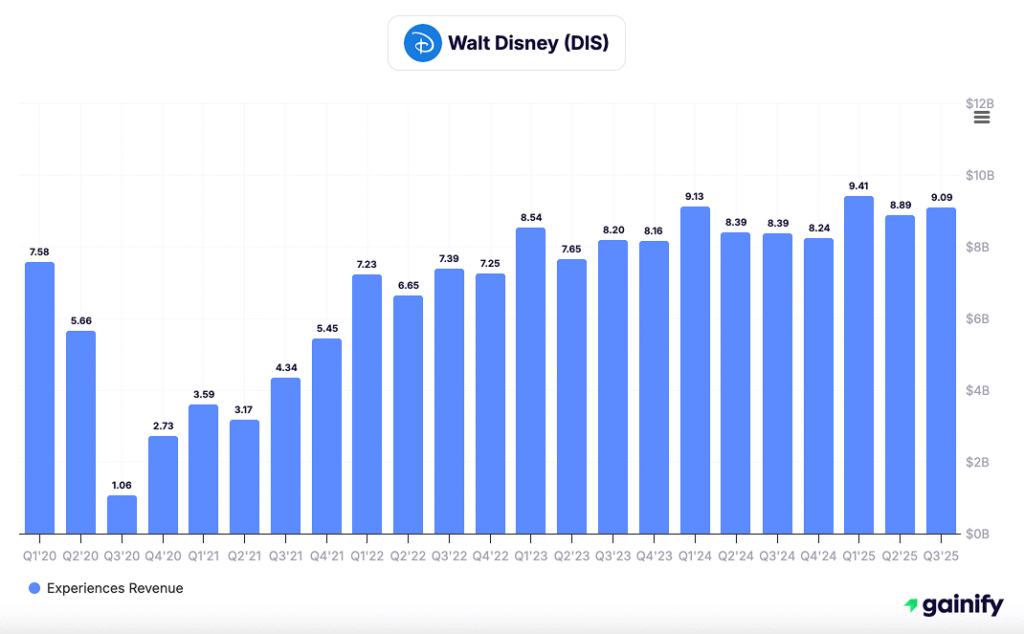

5. Walt Disney (NYSE: DIS)

Overview

Market Cap: $200.22B

P/E 2025e: 19.1x

Dividend Yield: 1.0%

FCF Yield: 5.7%

Analyst View: Outperform

Disney Cruise Line (DCL) operates within the Disney Experiences segment, alongside parks and resorts. The division has become an increasingly important profit driver, reflecting the strength of Disney’s experiential and brand-based ecosystem. The cruise business is positioned at the premium end of the family travel market, supported by strong brand equity and a high repeat-customer base.

Investment thesis

Disney leverages its entertainment IP, character franchises, and resort network to create a vertically integrated travel experience. The cruise line’s smaller, high-end fleet drives strong returns through premium pricing and differentiated offerings. DCL’s limited capacity model ensures high occupancy and brand exclusivity. The ongoing fleet expansion and geographic diversification, including the first Asia-based ship launching from Singapore — provide a clear growth runway through 2027.

Latest developments

In Q3 FY2025, the Disney Experiences segment recorded higher operating income year over year, supported by increased guest spending and higher volumes across domestic parks and Disney Cruise Line. Cruise performance improved on higher passenger cruise days and occupied room nights, largely due to the launch of the Disney Treasure, which began sailing in early 2025 and expanded global fleet capacity by roughly 20%. While operating costs increased with new guest offerings and the addition of ships, the cruise business contributed positively to segment growth. Early demand trends for 2026 sailings remain above historical averages, highlighting pricing resilience in premium family travel.

Key risks and catalysts

Results are linked to broader consumer discretionary trends and company-wide capital allocation. Rising fuel and staffing costs may limit near-term margin expansion. However, continued fleet growth, expansion into Asia, and increased cross-promotion between parks, films, and cruises reinforce long-term growth visibility. The upcoming Disney Adventure, launching from Singapore in 2026, is positioned to be a strategic catalyst for international brand and revenue diversification.

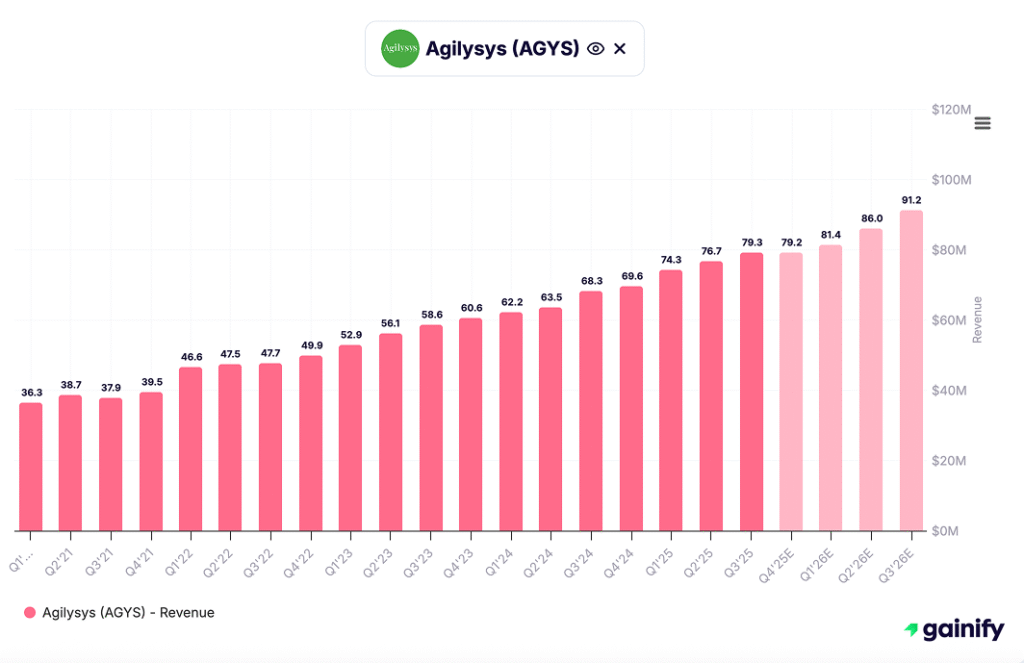

6. Agilysys (NASDAQ: AGYS)

Overview

Market Cap: $3.52B

P/E 2025e: 73.3x

Dividend Yield: N/A

FCF Yield: 1.4%

Analyst View: Buy

Agilysys (AGYS) develops hospitality management software serving hotels, resorts, casinos, and cruise lines. Its solutions span property management, point-of-sale, inventory control, and guest engagement systems, helping operators modernize core operations across global leisure and lodging markets.

Investment thesis

Agilysys is a pure-play digital enabler of the hospitality and travel recovery. Its cloud-based SaaS model delivers mission-critical functionality with high switching costs, driving durable recurring revenue that now exceeds 75% of total sales. With global travel technology adoption accelerating, Agilysys stands out as a scalable, asset-light compounder.

Latest developments

In fiscal Q2 2025, Agilysys reported revenue of $79.3 million, up 7% year over year, and adjusted EPS of $0.40, beating consensus estimates. Net income rose to $11.7 million, reflecting ongoing margin improvement. Management reaffirmed full-year revenue guidance of $315–318 million, implying mid-teens growth. Performance was supported by strong demand for cloud migrations and enterprise-level upgrades across hotels, resorts, and cruise clients.

Key risks and catalysts

Valuation remains elevated, requiring consistent execution and sustained SaaS expansion. Risks include slower hospitality capex cycles and rising implementation costs. Catalysts include wider adoption of integrated cloud platforms by global hotel and cruise operators, cross-selling of AI-enabled modules, and deeper integrations with payment and booking ecosystems.

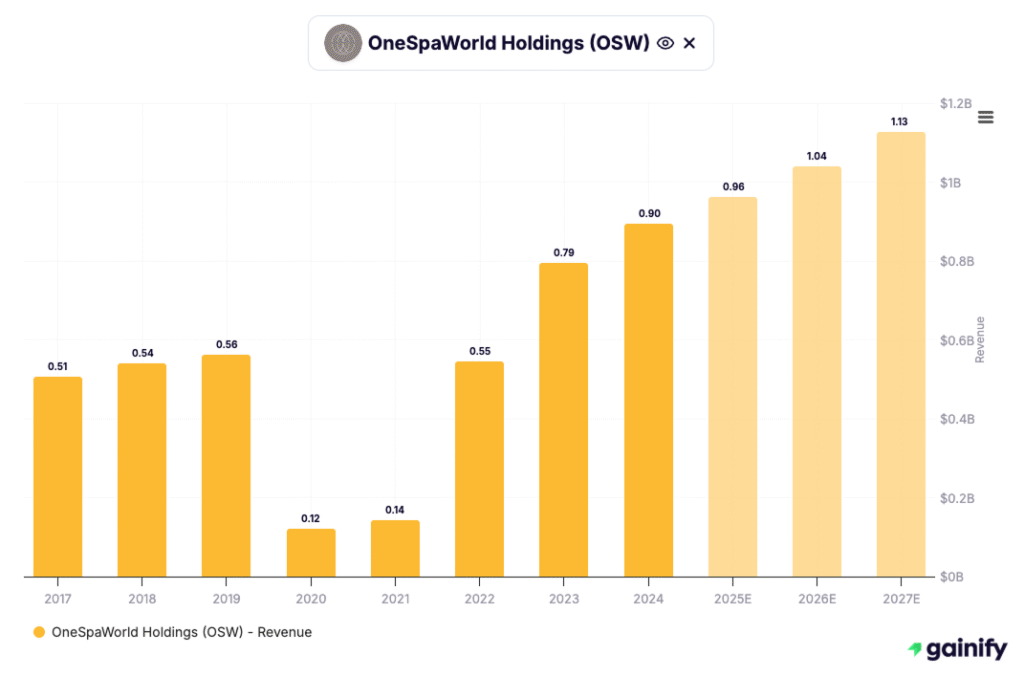

7. OneSpaWorld Holdings (NASDAQ: OSW)

Overview

Market Cap: $2.27B

P/E 2025e: 21.9x

Dividend Yield: 0.8%

Analyst View: Buy

OneSpaWorld (OSW) operates health, beauty, and wellness centers across the global cruise industry and at destination resorts. The company runs facilities on 204 ships and at 49 resorts, and holds 90%+ share of the outsourced spa market at sea.

Investment thesis

OSW benefits from exclusive, multi-year agreements with major cruise lines, which provide recurring revenue and strong cash conversion. The model is asset-light and scalable, with flexible staffing and variable costs that protect margins. Rising demand for wellness travel and the expansion of premium treatment menus support steady growth in spend per guest.

Latest developments

In Q3 2025, total revenue was $258.5 million, up 7% year over year. Adjusted EBITDA reached $35.0 million, up 6%, and net income rose 13% to $24.3 million. The network ended the quarter with centers on 204 ships and 49 resorts, and onboard staffing increased to 4,466 personnel. Management cited record operations and continued rollouts of enhanced spa concepts across leading fleets.

Key risks and catalysts

Results are sensitive to cruise passenger volumes, wage inflation, and itinerary changes. Growth catalysts include deeper integration with top cruise brands, upgraded premium services, digital booking and personalization initiatives, and expansion of resort partnerships in key tourism markets.

Final Takeaway

Cruise stocks have transitioned into a more mature investment phase defined by sustainable profitability, disciplined capital management, and selective capacity growth. The sector’s fundamentals now rest on stronger balance sheets and recurring cash flow rather than post-pandemic recovery momentum.

For investors looking to build exposure, Royal Caribbean (RCL) and Viking (VIK) offer structural growth through brand strength and pricing power, while Carnival (CCL) provides cyclical leverage to continued demand normalization. Agilysys (AGYS) and OneSpaWorld (OSW) add a technology and service layer that captures value beyond ticket sales, rounding out a diversified approach to the global cruise economy.

All figures reflect market data as of November 5, 2025. This material is for informational purposes only and does not constitute investment advice.

All figures reflect market data as of November 5, 2025. This content is for informational purposes only and does not constitute investment advice.