Railroads remain one of the most dependable pillars of North American transportation. As 2026 approaches, the industry is entering a new phase of steady, technology-driven growth. Nearshoring, infrastructure upgrades, and automation are reshaping how freight moves across borders and creating new efficiencies for the companies that operate these networks.

For investors, railroad stocks stand out for their consistency and resilience. They generate reliable cash flow, benefit from strong pricing power, and play an essential role in trade and logistics. With industrial activity improving and supply chains becoming more regional, the outlook for the major rail operators is positive.

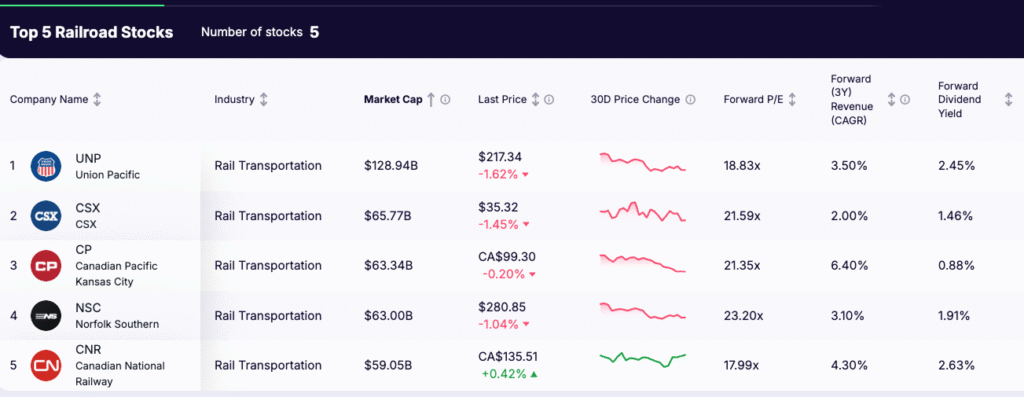

This analysis reviews five leading railroad stocks – Union Pacific, CSX, Canadian Pacific Kansas City, Norfolk Southern, and Canadian National Railway – and examines their businesses, performance drivers, and the trends likely to shape their results in 2026.

Key Highlights for 2026

- Steady but Slowing Growth: North American rail volumes rose about 2 percent in 2025, though quarterly gains eased as intermodal and industrial freight softened while bulk commodities stayed strong.

- Efficiency and Technology Drive Profitability: Railroads are focusing on automation, predictive maintenance, and digital scheduling to improve margins and offset slower traffic growth.

- Long-Term Fundamentals Stay Strong: Nearshoring, infrastructure modernization, and sustainability initiatives continue to underpin stable cash flow and support railroads as essential assets in North American trade.

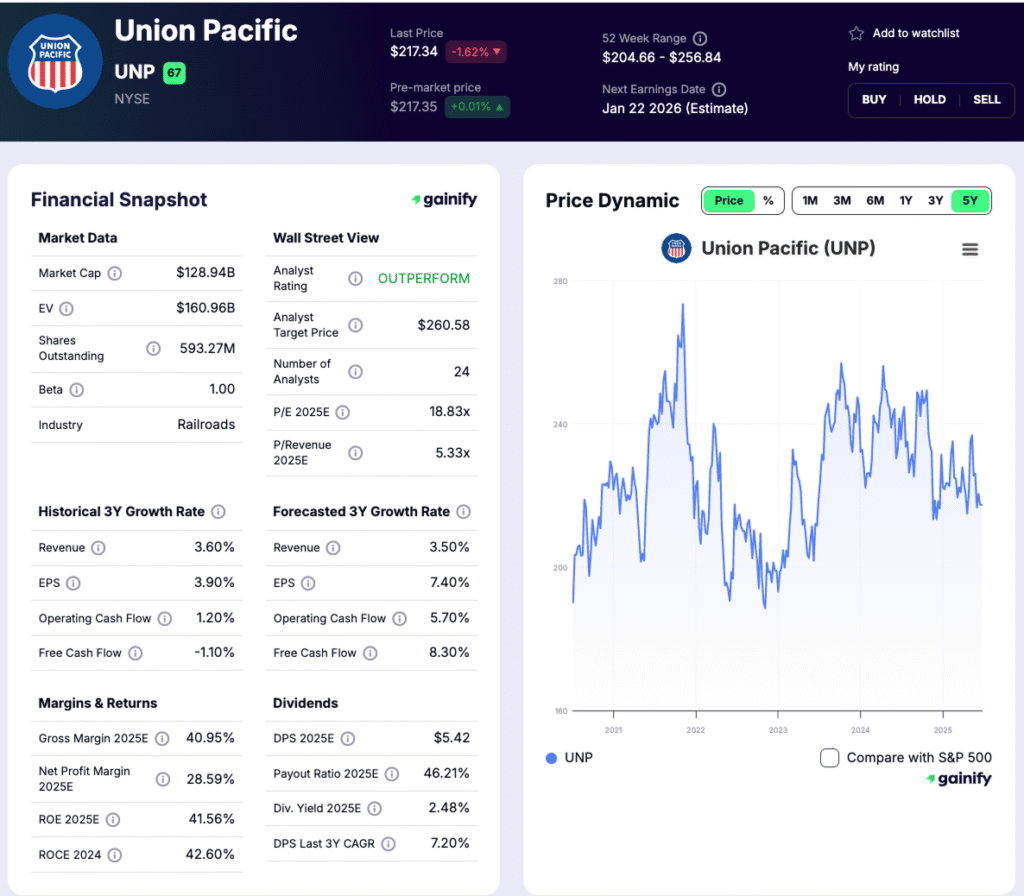

1. Union Pacific (NYSE: UNP)

- Market Cap: $128.9B

- Last Price: $217.34

- Forward P/E: 18.8x

- Forward Dividend Yield: 2.45%

- 3-Year Revenue CAGR: 3.5%

Overview:

Union Pacific is America’s largest publicly traded railroad, operating 32,000 route miles across 23 western states. Its network connects key ports, agricultural regions, and industrial hubs, forming the backbone of U.S. trade logistics. The company’s freight mix spans bulk commodities, industrial goods, intermodal containers, and automotive shipments.

Investment View:

Union Pacific’s scale, pricing power, and operational discipline support steady cash flow and shareholder returns. Efficiency initiatives such as automation and precision scheduling are improving margins, while a disciplined capital strategy underpins dividend stability.

Catalysts for 2026:

- Growth from U.S. manufacturing reshoring and intermodal demand.

- Margin improvement through automation and lower fuel intensity.

- Continued network efficiency and service reliability gains.

Risks:

Flat freight volumes, labor costs, fuel price volatility, and regulatory pressure remain key risks that could limit earnings growth.

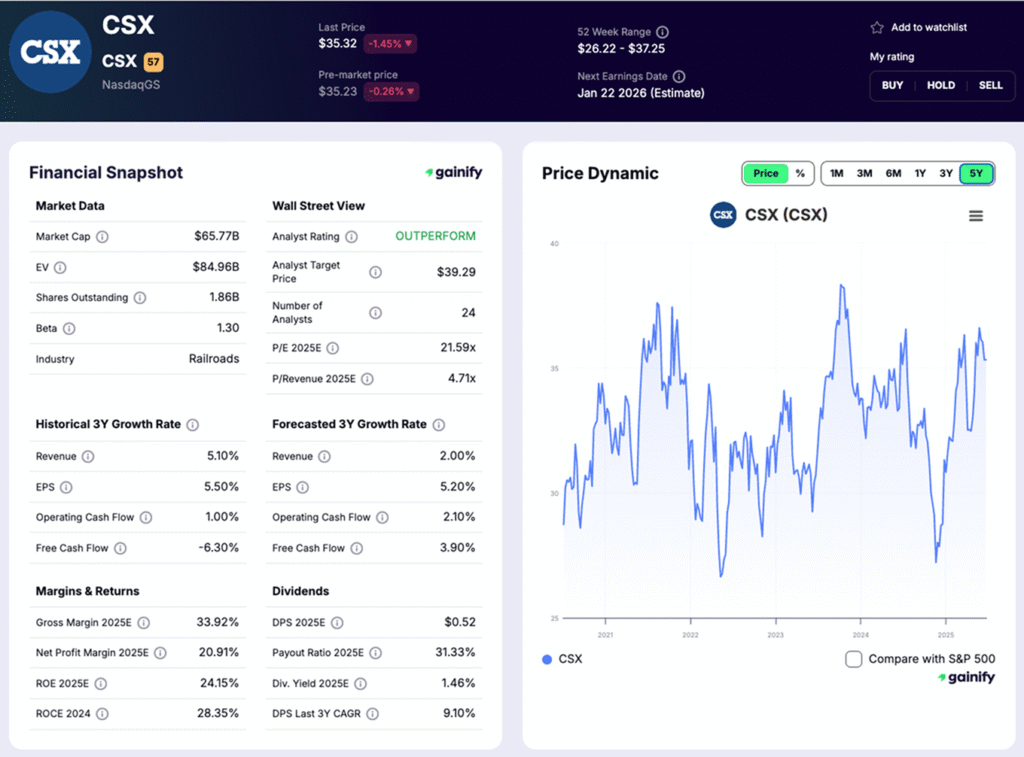

2. CSX Corporation (NASDAQ: CSX)

- Market Cap: $65.8B

- Last Price: $35.32

- Forward P/E: 21.6x

- Forward Dividend Yield: 1.46%

- 3-Year Revenue CAGR: 2.0%

Overview:

CSX operates a 21,000-mile rail network across the eastern United States, connecting the Midwest, Southeast, and Atlantic ports. The company plays a key role in moving intermodal freight, consumer goods, industrial products, and energy shipments across densely populated regions. Its strategic access to ports like Savannah, Charleston, and New York gives it an important position in U.S. logistics.

Investment View:

CSX is known for its efficient operations and disciplined cost management. Its precision scheduled railroading (PSR) model has improved network velocity and operating ratios, while ongoing investments in digital tools and terminal automation are strengthening service reliability. The company’s balance between operational efficiency and moderate revenue growth makes it appealing for investors seeking steady returns.

Catalysts for 2026:

- Growth in intermodal freight linked to e-commerce and port trade.

- Infrastructure expansion on the East Coast improving network capacity.

- Continued margin improvement through automation and disciplined capital spending.

Risks:

CSX remains exposed to shifts in consumer demand, weather-related disruptions, and competition from trucking. A prolonged slowdown in manufacturing or exports could weigh on volume growth.

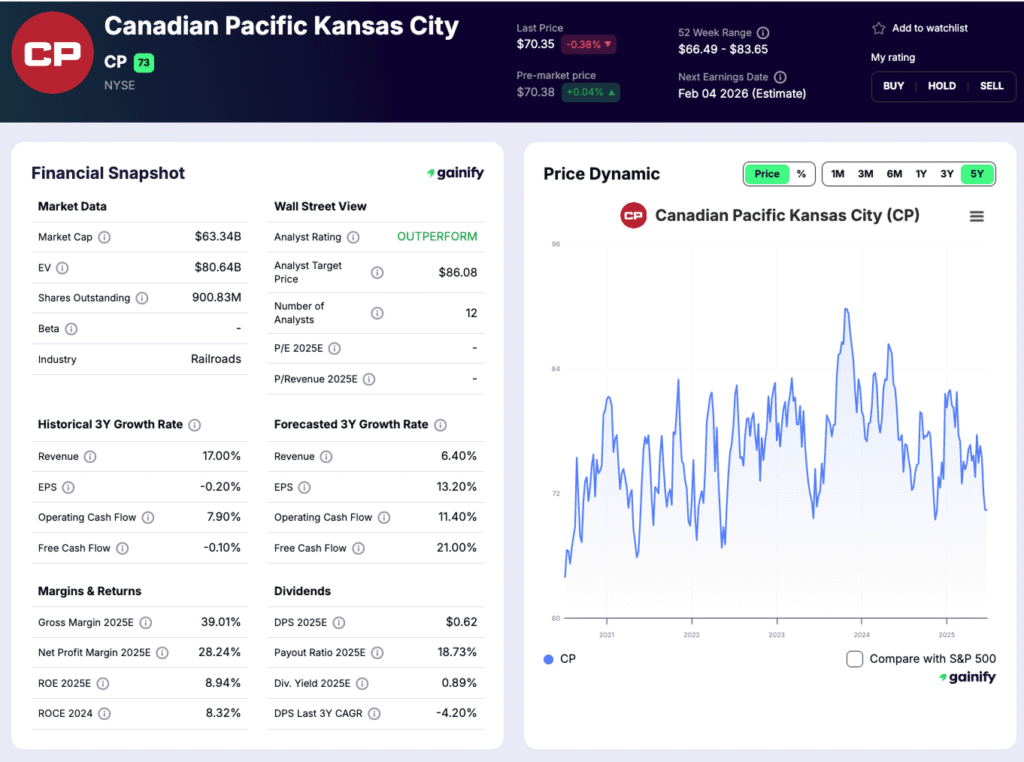

3. Canadian Pacific Kansas City (TSX/NYSE: CP)

- Market Cap: CA$63.3B

- Last Price: CA$99.30

- Forward P/E: 21.3x

- Forward Dividend Yield: 0.88%

- 3-Year Revenue CAGR: 6.4%

Overview:

Canadian Pacific Kansas City (CP) is the only single-line railway linking Canada, the United States, and Mexico. Formed through the 2023 merger of Canadian Pacific and Kansas City Southern, it operates roughly 20,000 route miles across North America’s three largest economies. The company transports automotive parts, grain, chemicals, intermodal freight, and energy products, making it a key player in continental trade and manufacturing supply chains.

Investment View:

CPKC’s unified network gives it a unique advantage as North American supply chains shift closer to home. Rising nearshoring and cross-border production are expected to drive long-term freight growth, particularly in automotive and industrial goods. Continued efficiency gains and network integration should help margins improve over the next few years.

Catalysts for 2026:

- Expansion of U.S.–Mexico manufacturing and export activity under the USMCA framework.

- Growth in automotive and energy freight volumes.

- Operational benefits from technology integration and improved cross-border fluidity.

Risks:

The company still faces integration challenges following the merger and remains sensitive to currency movements, weather-related disruptions, and regulatory oversight across its three jurisdictions.

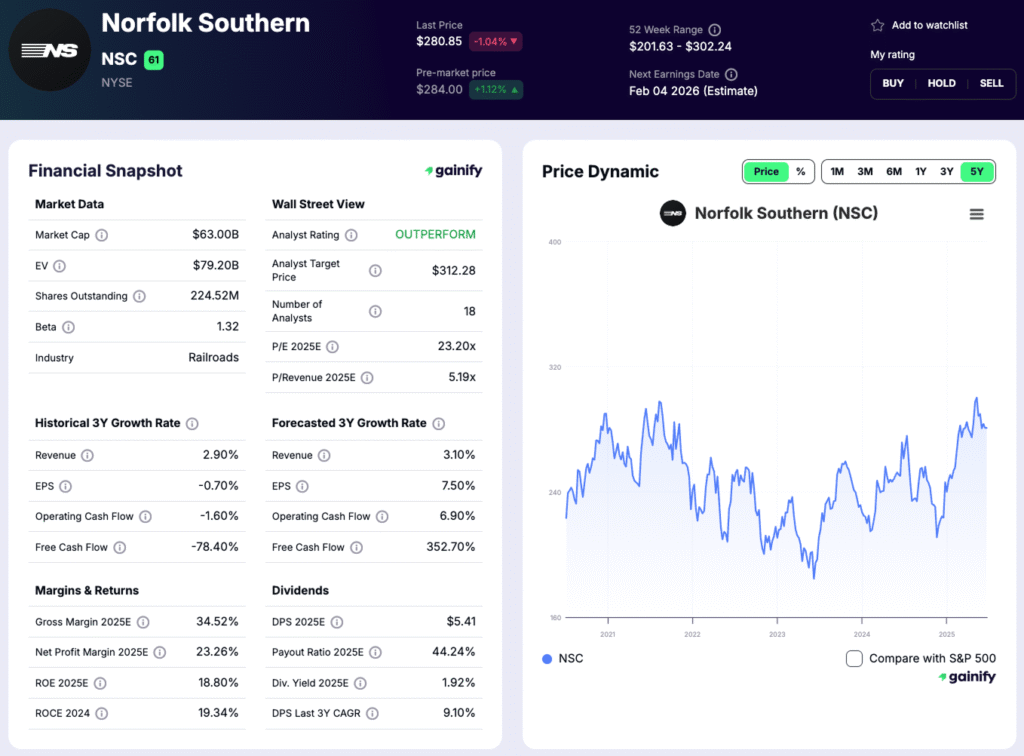

4. Norfolk Southern (NYSE: NSC)

- Market Cap: $63.0B

- Last Price: $280.85

- Forward P/E: 23.2x

- Forward Dividend Yield: 1.91%

- 3-Year Revenue CAGR: 3.1%

Overview:

Norfolk Southern operates about 19,000 route miles across the eastern and southeastern United States. Its network connects the Midwest to key Atlantic ports, with major terminals in Atlanta, Charlotte, and Norfolk. Core freight categories include intermodal shipments, automotive products, and coal. The company continues to invest heavily in infrastructure and service reliability following recent safety and operational challenges.

Investment View:

Norfolk Southern is working through a multi-year modernization program aimed at restoring network efficiency and strengthening its cost base. While near-term results remain constrained by higher safety and compliance expenses, the company’s long-term fundamentals are supported by strong geographic positioning and exposure to high-value freight sectors.

Catalysts for 2026:

- Ongoing infrastructure upgrades across the Southeast and East Coast.

- Growth in intermodal and automotive volumes tied to regional manufacturing.

- Efficiency gains through digital systems and improved asset utilization.

Risks:

Heightened regulatory oversight and insurance costs remain key concerns. Volume growth may be limited by economic headwinds, while ongoing safety-related expenses could weigh on margins.

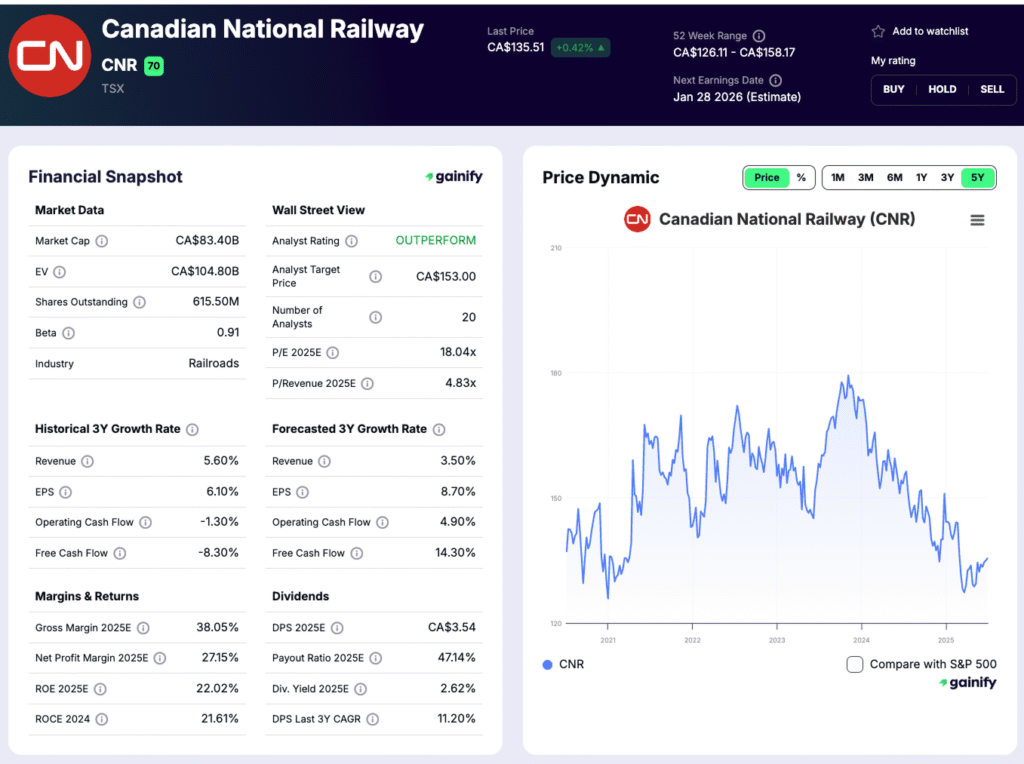

5. Canadian National Railway (TSX/NYSE: CNR)

- Market Cap: CA$59.0B

- Last Price: CA$135.51

- Forward P/E: 17.99x

- Forward Dividend Yield: 2.63%

- 3-Year Revenue CAGR: 4.3%

Overview:

Canadian National Railway (CNR) is Canada’s largest rail operator, managing a 20,000-mile network that links the Atlantic and Pacific coasts with the U.S. Midwest and Gulf of Mexico. This extensive system makes CNR a critical connector for trade and exports across North America. The company’s freight portfolio includes petroleum, chemicals, grain, forest products, coal, and intermodal containers.

Investment View:

CNR offers investors a balance of stability and steady growth. It maintains one of the strongest balance sheets in the industry, supported by disciplined cost control and efficient network utilization. The company’s focus on technology, including AI-driven scheduling and fuel-efficient locomotives, supports long-term margin expansion and sustainability goals.

Catalysts for 2026:

- Expansion of Canadian exports, particularly grain and energy products.

- Growth in intermodal freight as global trade patterns evolve.

- Ongoing investment in automation, infrastructure, and decarbonization initiatives.

Risks:

CNR faces exposure to commodity cycles, harsh weather conditions, and currency fluctuations between the Canadian and U.S. dollars. A slowdown in industrial output or exports could moderate volume growth.

What Drives the North American Railroad Industry in 2026

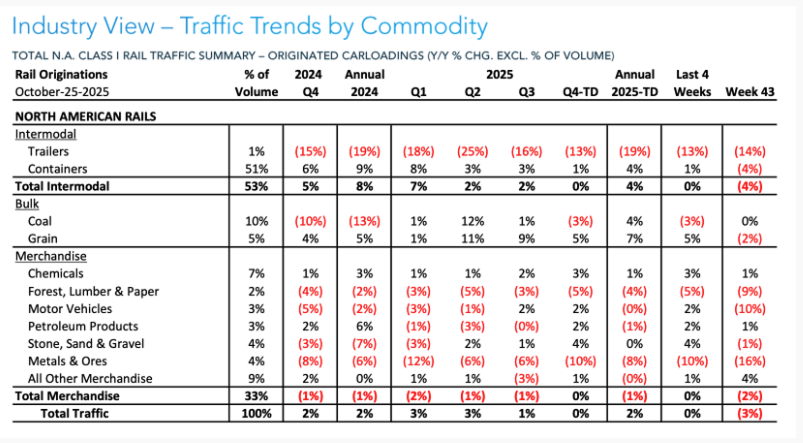

The North American rail industry enters 2026 with modest growth and a more measured outlook. Total rail traffic for 2025 rose about 2 percent year to date, marking a steady recovery from recent lows. However, the pace of growth slowed as the year progressed, easing from roughly 3 percent in the first quarter to around 1 percent by the third. The result is a landscape of selective strength, where certain freight categories continue to expand while others remain under pressure.

1. Trade and Freight Demand

Freight performance in 2025 was uneven across segments. Bulk commodities, particularly coal and grain, delivered the strongest results with year-to-date gains near 4 percent. Intermodal volumes were mixed, as container traffic edged slightly lower and trailer shipments declined sharply. Merchandise freight categories, including chemicals and petroleum products, were largely stable, though forest products and metals weakened.

Key Insight: Total traffic remains positive but momentum is slowing. Bulk commodities and select merchandise shipments are offsetting softness in intermodal and industrial freight.

2. Nearshoring and Supply Chain Shifts

The continued relocation of manufacturing closer to U.S. markets is reshaping freight flows. Mexico and the southern United States remain focal points for investment, gradually increasing cross-border rail activity. Carriers such as Canadian Pacific Kansas City and Union Pacific are beginning to capture incremental gains from stronger north–south trade under the USMCA.

Key Insight: Nearshoring is a slow but steady structural trend, providing a foundation for longer-term freight growth rather than a near-term surge.

3. Technology and Automation

Railroads are relying on technology to sustain profitability amid moderating volume growth. The deployment of predictive maintenance systems, automation, and AI-based network management has improved fuel efficiency and service reliability. Digital investments are also helping operators control costs and meet sustainability goals across increasingly complex supply chains.

Key Insight: Technology remains central to cost control and service quality, enabling railroads to improve margins even in a slower traffic environment.

4. Infrastructure and Modernization

Investment in infrastructure continues to underpin the sector’s long-term competitiveness. In 2025, more than three billion dollars was allocated to track upgrades, terminal expansion, and safety programs across North America. These initiatives are improving operational resilience and preparing networks for future demand growth tied to nearshoring and export activity.

Key Insight: Ongoing infrastructure modernization supports efficiency and reliability, ensuring that railroads remain integral to continental trade.

Outlook for 2026

The rail industry enters 2026 with modest traffic growth and slowing momentum. Bulk commodities and cross-border trade remain the main stabilizers, while intermodal and industrial freight continue to lag. With volumes plateauing, profitability will increasingly depend on technology, operational discipline, and targeted investment. Despite near-term softness, railroads remain essential to North American commerce and are positioned for gradual, efficiency-driven progress in the year ahead.

Bottom Line

Conclusion

The 2026 outlook for North American railroads is defined by steady fundamentals and measured expectations. Volume growth has moderated, but the sector continues to demonstrate resilience through disciplined operations and strategic investment.

Union Pacific maintains a leadership position through scale and efficiency, Canadian Pacific Kansas City stands out for its cross-border growth potential, and Canadian National Railway delivers reliable returns through superior cost management. CSX and Norfolk Southern remain vital in the eastern market, leveraging strong regional networks and port connectivity.

Railroads may not be a high-growth story in 2026, but they remain essential infrastructure businesses capable of consistent performance. As nearshoring deepens and technology transforms operations, the industry’s focus on reliability, sustainability, and efficiency will continue to generate long-term value for investors.

Bottom line: Growth is slowing, but the track ahead remains solid. For investors seeking stable returns from critical assets, railroad stocks continue to represent a dependable route forward.