If you stream a film, ask an AI, unlock a phone, or start a car, you are using semiconductors.

In 2026, chips sit inside nearly every device and data center on the planet. That universal demand is why semiconductor stocks have been among the market’s most powerful drivers of wealth creation in recent years.

Investors are not just buying a gadget cycle. They are buying the infrastructure behind artificial intelligence, cloud computing, connected cars, factory automation, and secure communications. Each of those trends needs more compute, more memory, and more specialized silicon.

Over the last decade, semiconductor stocks have outperformed the S&P 500 by NEARLY FOUR times, reflecting their pivotal role in global innovation and economic transformation. The combination of structural demand, technological leadership, and expanding use cases has made the sector one of the most important engines of modern market growth.

In this article, we look at the 12 largest semiconductor stocks shaping the industry today.

What Are Semiconductors?

Semiconductors are the core components that make modern electronics possible. They are used to build chips that process, store, and transfer information across billions of devices worldwide. While the term originally referred to materials like silicon that can conduct electricity in controlled ways, today it represents a vast global industry of companies that design, manufacture, and supply the technology behind digital life.

Most chips are still made from silicon, but advanced materials such as gallium nitride (GaN) and silicon carbide (SiC) are becoming increasingly important for high-performance computing, electric vehicles, and renewable energy systems.

Simply put, semiconductors are the foundation of modern technology. They enable everything from smartphones and computers to electric vehicles and satellites, making devices intelligent, efficient, and connected.

Main Types of Semiconductors

Logic and Processors

The brains of computing systems, including CPUs, GPUs, and AI accelerators that power data centers, cloud computing, and advanced analytics.

Memory

DRAM provides fast temporary storage, while NAND flash stores data long-term. Memory demand continues to grow with AI, cloud services, and autonomous systems.

Analog and Mixed-Signal

Power management and interface chips that connect digital processors to the real world, ensuring stable performance and energy efficiency.

RF and Connectivity

Chips that enable 5G, Wi-Fi, Bluetooth, and satellite communication across devices and networks.

Power and Automotive

Used in electric vehicles, chargers, and renewable energy systems. Materials like SiC and GaN improve efficiency and reduce heat loss.

Sensors and Microcontrollers

Provide perception and control in devices such as cars, industrial machines, and consumer electronics.

The Semiconductor Value Chain

- Designers (e.g., NVIDIA, AMD, Qualcomm, Broadcom, Arm Holding) create architectures and intellectual property.

- Foundries (e.g., TSM) manufacture chips for designers.

- Integrated Device Makers (e.g., Intel, Micron Technology) design and produce chips in-house.

- Equipment Suppliers (e.g., ASML, Applied Materials, Lam Research, KLA Corporation) provide the tools and materials needed for fabrication.

Semiconductors are the backbone of the global digital economy, powering innovation in AI, communications, healthcare, and energy. Their influence will only expand as the world becomes more data-driven and interconnected.

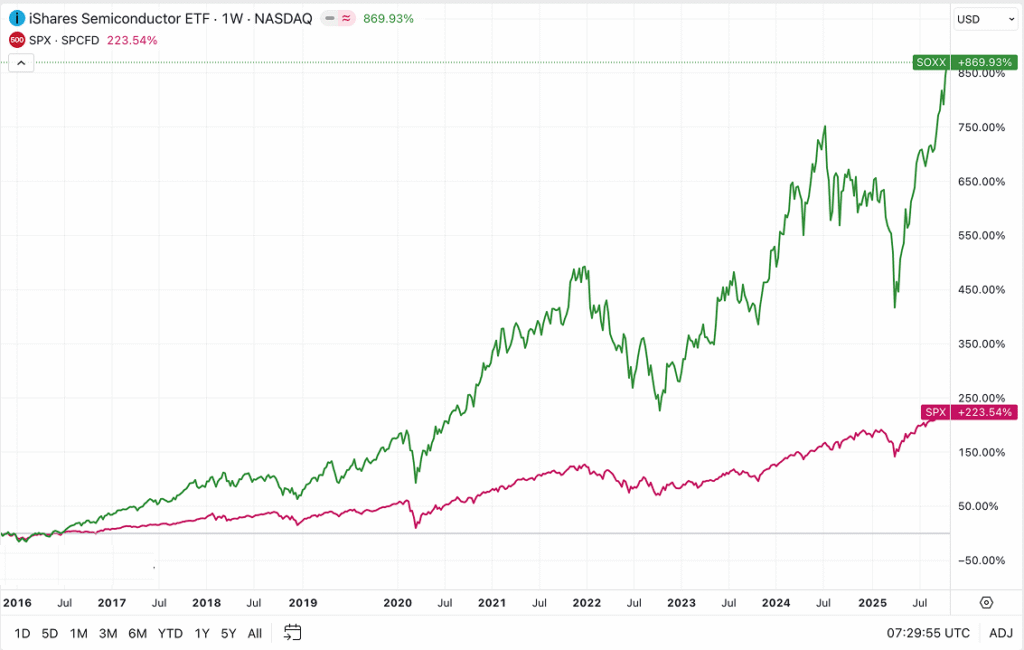

Semiconductor Outperformance Over the Last 10 Years

Over the past decade, semiconductor stocks have been the backbone of equity market gains. The chart compares the iShares Semiconductor ETF (SOXX) with the S&P 500 (SPX). Since 2015, SOXX has surged nearly 870%, compared with a 220% gain for the S&P 500. That is almost four times the total return of the broader market.

Why Semiconductors Outperformed

- AI and Cloud Boom: Explosive demand for compute power across data centers and AI applications.

- Memory and Storage Growth: Stronger pricing and adoption of high-bandwidth memory in servers and edge devices.

- Automotive and Industrial Expansion: Rising semiconductor content in electric vehicles, driver assistance, and factory automation.

- Post-2022 Recovery: Inventory normalization led to a powerful rebound and new investment in advanced manufacturing nodes.

- Equipment and Tools Upside: Persistent strength in lithography and wafer fabrication equipment suppliers.

Why It Can Still Be Volatile

- Cyclicality: Demand fluctuations as customers adjust inventory levels.

- Capital Intensity: High investment cycles for fabrication and tools during each new node transition.

- Geopolitical Risk: Export restrictions, supply chain realignments, and regional subsidies affecting production and trade.

How to Read the Chart

- The sharp rise in 2024–2025 reflects AI server growth and a rebound in memory pricing.

- The dip in 2022 shows the semiconductor inventory correction and tighter monetary conditions.

- The long-term trend remains up because nearly every industry continues to add more silicon content.

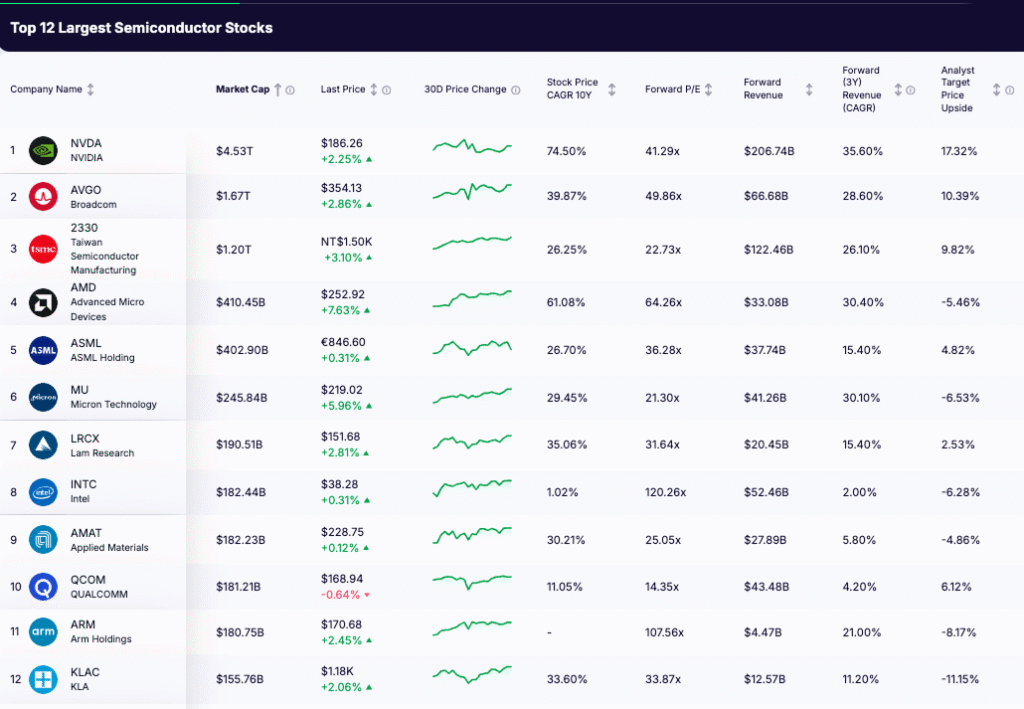

The 12 Largest Semiconductor Companies by Market Cap

Below is a look at the 12 largest publicly traded semiconductor companies in the world as of October 2025, ranked by market capitalization. Each plays a distinct role in the chip value chain and is driving or enabling the next wave of technological innovation in AI, computing, and connectivity.

12) KLA (KLAC)

Market Cap: $155.76 billion

2025E Revenue: $12.57 billion

Analyst Target Price Upside: –11.15%

2025E P/E: 33.87x

What it does:

KLA develops process-control and metrology tools that enhance chip yields and manufacturing precision by identifying defects and ensuring consistency across production steps. Its systems help chipmakers maintain high quality and efficiency at increasingly advanced nodes.

Key investment theses:

- Process complexity at advanced nodes drives more inspection steps per wafer.

- Recurring high-margin service revenue from a large installed base.

- Broad exposure across logic, memory, and foundry markets.

Key risks:

- Wafer-fab equipment spending remains cyclical and could slow.

- High dependency on major foundry customers introduces concentration risk.

- Export restrictions and geopolitical tensions pose upside and downside risks.

11) Arm Holdings (ARM)

Market Cap: $180.57 billion

2025E Revenue: $4.23 billion

Analyst Target Price Upside: +8.9%

2025E P/E: 87.2x

What it does:

Arm designs and licenses energy-efficient processor architectures used in smartphones, data centers, automotive systems, and emerging AI devices. Its IP forms the foundation for over 95% of mobile chips and a rapidly growing share of AI and edge computing processors.

Key investment theses:

- Licensing model scalability: Arm’s royalty and license-based revenue model allows high margins with limited capital intensity.

- AI and edge growth: Expanding use of Arm CPUs and NPUs in AI PCs, servers, and automotive applications boosts long-term demand.

- Ecosystem dominance: Deep partnerships with major chipmakers (Apple, Nvidia, Qualcomm, and Amazon) secure Arm’s architectural leadership.

- New pricing structure: Armv9 architecture rollout and per-core royalty uplift improve monetization across devices.

Key risks:

- Valuation risk: Premium multiple (80–100× forward P/E) leaves little room for growth disappointments.

- Customer concentration: Heavy reliance on a handful of large licensees for revenue.

- Geopolitical exposure: Licensing to Chinese subsidiaries subject to export and regulatory uncertainties.

- Execution risk: Success in servers and AI depends on sustained adoption by hyperscalers and chip partners.

10) Qualcomm (QCOM)

Market Cap: $181.21 billion

2025E Revenue: $43.6 billion

Analyst Target Price Upside: +12.4%

2025E P/E: 14.4x

What it does:

Qualcomm is a global leader in wireless chipsets and connectivity solutions. It designs and supplies mobile processors (Snapdragon), modems, RF systems, and increasingly AI-enabled SoCs for smartphones, automotive platforms, and connected devices. Its technology underpins 5G networks and next-generation on-device AI capabilities.

Key investment theses:

- Diversification beyond smartphones: Expanding growth engines in automotive, IoT, and PC processors reduce reliance on cyclical handset demand.

- AI integration: On-device AI processing in Snapdragon chips (for phones and PCs) positions Qualcomm as a key beneficiary of edge AI growth.

- 5G leadership: Maintains dominant share in premium 5G modems and RF front-end solutions.

- Attractive valuation: Among the lowest P/E multiples in the large-cap semiconductor space despite high free cash flow generation.

Key risks:

- Customer concentration: Heavy dependence on a few large OEMs (especially Apple and Samsung).

- Competitive pressure: Rising competition from MediaTek, Apple’s in-house silicon, and custom AI chip vendors.

- Cyclical handset demand: Global smartphone weakness could offset growth in newer segments.

- Regulatory and export risk: Ongoing scrutiny in China and antitrust actions could impact licensing revenue.

9) Applied Materials (AMAT)

Market Cap: $182.23 billion

2025E Revenue: $26.15 billion

Analyst Target Price Upside: +7.8%

2025E P/E: 25.1x

What it does:

Applied Materials is the world’s largest supplier of semiconductor manufacturing equipment. Its tools and software are used in nearly every step of chip fabrication from deposition and etching to inspection and packaging. The company also provides materials engineering solutions for displays and advanced packaging technologies.

Key investment theses:

- Breadth across wafer-fab steps: Exposure to logic, memory, and foundry markets diversifies risk and captures growth across semiconductor cycles.

- AI-driven demand: Advanced node transitions (3nm and below) and AI chip complexity increase capital intensity, boosting tool demand.

- Recurring service revenue: A large installed base generates high-margin, recurring services and parts sales.

- Technology leadership: Continued innovation in materials deposition and patterning strengthens its competitive position.

Key risks:

- Cyclical WFE spending: Capital spending fluctuations among foundries and memory makers can create revenue volatility.

- Geopolitical exposure: Roughly 30% of revenue tied to China; export restrictions could constrain shipments.

- Intense competition: Rivalry with Lam Research, Tokyo Electron, and ASML in key process equipment categories.

- Customer concentration: Heavy reliance on a handful of large semiconductor manufacturers for new orders.

8) Intel (INTC)

Market Cap: $182.44 billion

2025E Revenue: $52.46 billion

Analyst Target Price Upside: –6.28 %

2025E P/E: 120.26x

What it does:

Intel designs and manufactures CPUs, chipsets, and networking silicon for PCs, servers, and data centers. The company is also transforming into a global foundry service provider through its Intel Foundry Services (IFS) business, building advanced manufacturing capacity in the U.S. and Europe.

Key investment theses:

- Foundry transformation: Intel is investing over $100 billion to regain process leadership and establish a U.S.-based foundry alternative to TSM and Samsung.

- Strategic national asset: Its manufacturing footprint has made Intel a centerpiece of the U.S. semiconductor-resilience strategy, benefiting from CHIPS Act subsidies and political support.

- Technology roadmap: Aims to deliver five nodes in four years (Intel 3 through 14A) and position IFS as a key supplier for domestic and allied-nation chip production.

- AI exposure: Expanding Xeon 6 processors and Gaudi AI accelerators broaden Intel’s relevance in AI compute, even as it lags Nvidia and AMD in performance.

Major recent developments / government involvement:

- August 2025 – U.S. Government stake: Washington finalized an $11.1 billion investment for a 9.9 % equity position in Intel, converting part of CHIPS Act grants into shares to secure U.S. semiconductor capacity.

- CHIPS Act funding: Earlier grants totaling $7.86 billion plus $5.7 billion accelerated funding support ongoing fab projects in Arizona, Ohio, New Mexico, and Oregon.

- Foundry expansion: Intel Foundry signed new customer design wins, including partnerships with U.S. defense contractors and AI chip startups, strengthening domestic supply-chain resilience.

Key risks:

- Execution risk: Failure to meet process-node milestones (Intel 3, 20A, 18A) could derail foundry credibility.

- Capital intensity: Massive capex (> $25 billion per year) pressures cash flow and raises dilution risk.

- Cyclicality: Weak PC and data-center demand can limit near-term recovery.

- Policy risk: Government ownership and funding come with constraints on buybacks, overseas expansion, and governance oversight.

- Competition: Persistent leadership from TSM, Samsung, and AMD continues to challenge Intel’s turnaround.

7) Lam Research (LRCX)

Market Cap: $190.51 billion

2025E Revenue: $20.45 billion

Analyst Target Price Upside: +2.53 %

2025E P/E: 31.64x

What it does:

Lam Research designs and manufactures wafer-fabrication equipment used for etch and deposition processes, which are critical steps in producing advanced logic and memory chips. Its tools enable the creation of smaller, denser, and more power-efficient semiconductors across DRAM, NAND, and logic nodes.

Key investment theses:

- AI-driven demand: The boom in AI data-center chips is fueling new wafer-fab equipment (WFE) spending, benefiting Lam’s core etch and deposition markets.

- Technology leadership: Lam’s deep expertise in atomic-level etch and deposition supports next-generation 3D NAND, gate-all-around, and advanced logic production.

- Installed-base leverage: A large global footprint provides recurring, high-margin services and spares revenue.

- Capital discipline: Strong free-cash-flow generation supports consistent buybacks and dividend growth.

Recent developments:

- HBM and advanced logic exposure: Demand for high-bandwidth-memory and AI-optimized devices has increased orders from Samsung, SK Hynix, and TSM.

- China impact: Approximately 30 % of sales come from China; export-control adjustments in 2025 added some near-term uncertainty but overall backlog remains solid.

- Product innovation: Lam continues expanding its Sense.i platform, which is an AI-driven equipment architecture improving throughput and process control.

- AI manufacturing push: The company is integrating more automation and analytics into fabs to address rising chip complexity and shortage of skilled labor.

Key risks:

- Cyclical exposure: Semiconductor capital-spending cycles can lead to sharp revenue swings.

- Geopolitical dependence: High China exposure subjects Lam to U.S. export-license constraints.

- Customer concentration: A few large foundry and memory clients account for most orders.

- Technology transition risk: Delays in new node adoption or memory-capex pullbacks could pressure growth.

6) Micron Technology (MU)

Market Cap: $245.84 billion

2025E Revenue: $41.26 billion

Analyst Target Price Upside: –6.53 %

2025E P/E: 21.30x

What it does:

Micron Technology produces DRAM and NAND memory chips used in data centers, AI infrastructure, mobile devices, and automotive systems. Its products are critical to enabling faster data processing, higher storage density, and energy-efficient computing.

Key investment theses:

- AI demand tailwind: High-bandwidth memory (HBM) adoption in AI servers and GPUs is driving a strong pricing recovery and multi-year growth opportunity.

- Rising memory content: Increasing DRAM and NAND requirements per device across all end markets provide long-term structural growth.

- Supply discipline: Industry consolidation among major players supports healthier pricing and margin expansion.

- Financial strength: Strong cash flow and a solid balance sheet allow Micron to invest through cycles while maintaining shareholder returns.

Recent developments:

- HBM3E ramp: Micron achieved early volume production for HBM3E, winning key AI platform design-ins with Nvidia and AMD.

- Pricing recovery: Memory prices stabilized in 2025 after a prolonged downturn, lifting gross margins across segments.

- Domestic manufacturing: U.S. CHIPS Act funding supports new fabs in Idaho and New York, enhancing supply security.

- AI ecosystem expansion: Deeper partnerships with hyperscalers and AI chipmakers are strengthening Micron’s market positioning.

Key risks:

- Cyclical volatility: Memory prices remain sensitive to supply-demand shifts and can compress profitability quickly.

- Capital intensity: Sustaining technological leadership requires heavy investment in new fabs and process nodes.

- Geopolitical exposure: China accounts for a meaningful portion of demand and remains subject to export restrictions.

- End-market dependence: A slowdown in data-center or AI infrastructure spending could delay expected earnings growth.

5) ASML Holding (ASML) — $402.90B

Market Cap: $402.90 billion

2025E Revenue: $35.89 billion

Analyst Target Price Upside: +8.24 %

2025E P/E: 36.27x

What it does:

ASML designs and manufactures advanced lithography systems used in semiconductor production. It is the only company in the world capable of producing extreme ultraviolet (EUV) and next-generation high-NA EUV lithography machines, which are essential for manufacturing cutting-edge chips at 3 nm and below.

Key investment theses:

- Monopoly position: Exclusive control of EUV technology provides unmatched pricing power and long-term visibility.

- AI and advanced-node growth: Rising demand for high-performance logic and memory chips drives sustained orders for EUV and DUV systems.

- High-NA EUV rollout: The next generation of lithography tools extends ASML’s technology lead and deepens its customer relationships.

- Service and install base: A growing installed base supports recurring high-margin service revenue.

Recent developments:

- High-NA shipments: ASML began delivering its first High-NA EUV systems in 2025, marking a key technological milestone.

- Capacity expansion: The company continues to scale production to meet AI-driven demand from TSM, Samsung, and Intel.

- Order momentum: Backlog remains robust as foundries accelerate investments in advanced nodes.

- Government oversight: EU and Dutch authorities are coordinating with ASML on export-license compliance amid tightening U.S. export controls.

Key risks:

- Geopolitical and regulatory exposure: Export restrictions to China could limit unit growth and revenue diversification.

- Customer concentration: A small number of large chipmakers represent most system sales.

- Cyclical capital spending: Semiconductor-equipment demand can fluctuate with industry investment cycles.

- Execution risk: Delays or cost overruns in High-NA EUV production could slow revenue recognition.

4) Advanced Micro Devices (AMD)

Market Cap: $410.45 billion

2025E Revenue: $33.46 billion

Analyst Target Price Upside: +6.59 %

2025E P/E: 64.29x

What it does:

Advanced Micro Devices designs high-performance computing and graphics chips used in data centers, PCs, and gaming systems. Its product portfolio includes EPYC server processors, Ryzen CPUs, and Instinct AI accelerators, which compete directly with Intel and Nvidia across several high-growth segments.

Key investment theses:

- AI leadership expansion: The MI300 and upcoming MI400 series accelerators position AMD as a viable alternative to Nvidia in AI training and inference markets.

- Data center strength: EPYC processors continue gaining share against Intel in server compute, supported by hyperscaler and cloud adoption.

- Diversified growth: Balanced exposure across data center, client, gaming, and embedded markets provides resilience through cycles.

- Scalable business model: Strong gross margins and asset-light manufacturing via TSM enable consistent cash generation and reinvestment capacity.

Recent developments:

- OpenAI partnership: In mid-2025, AMD and OpenAI entered a multi-year collaboration to optimize MI300X and MI400 accelerators for ChatGPT and related inference workloads, expanding AMD’s footprint in AI data centers.

- AI momentum: Growing demand for AMD’s Instinct accelerators and ROCm software stack is boosting server GPU shipments.

- Product roadmap: MI400 and Zen 6 architecture are expected to launch in 2026, extending AMD’s performance leadership trajectory.

- Customer diversification: Partnerships with Microsoft, Meta, and Oracle are supporting AI infrastructure growth across cloud ecosystems.

Key risks:

- Competitive pressure: Nvidia maintains dominant market share and faster software ecosystem development.

- Supply dependence: Heavy reliance on TSM for leading-edge manufacturing nodes.

- Valuation risk: High P/E multiple leaves little margin for execution setbacks.

- Market cyclicality: Soft PC and gaming demand can offset strength in data center and AI segments.

3) Taiwan Semiconductor Manufacturing Co. (TSM)

Market Cap: $1.20 trillion

2025E Revenue: $88.68 billion

Analyst Target Price Upside: +4.64 %

2025E P/E: 22.69x

What it does:

TSM is the world’s largest dedicated semiconductor foundry. The company manufactures advanced chips for major technology firms including Apple, Nvidia, AMD, and Qualcomm. Its leadership in process technology at 3 nanometers and its ramp toward 2 nanometers make it the backbone of global semiconductor production.

Key investment theses:

- Process-node leadership: TSM’s consistent yield and performance advantage at advanced nodes sustain pricing power and customer loyalty.

- AI and high-performance computing growth: Surging demand for AI GPUs and data center chips continues to drive record utilization and revenue growth.

- Diversified customer portfolio: The company manufactures chips for nearly every leading fabless semiconductor firm, spreading risk across markets.

- Capital efficiency: Strong cash generation supports continuous capacity expansion while maintaining solid margins.

Recent developments:

- 2 nanometer production ramp: Volume production of N2 began in 2025 with Apple and Nvidia as anchor customers, while the 1.4 nanometer A14 process is in early development for 2027.

- Global capacity expansion: U.S. Arizona fab expected to reach mass production in 2026 with partial CHIPS Act funding, and the new Japan facility began volume output in early 2025.

- AI-driven demand: Orders for advanced packaging, particularly CoWoS capacity, have expanded to support GPU and accelerator customers.

- Geographic diversification: TSM continues building out fabs in Japan, the United States, and Europe to reduce concentration risk in Taiwan.

Key risks:

- Geopolitical exposure: Escalating tensions between China and Taiwan present ongoing operational and systemic risk.

- Customer concentration: A large portion of revenue depends on Apple, Nvidia, and AMD.

- Execution risk: Delays in new-node deployment or expansion projects could impact competitiveness.

- Industry competition: Samsung Foundry and Intel Foundry Services are heavily investing to narrow the technology gap.

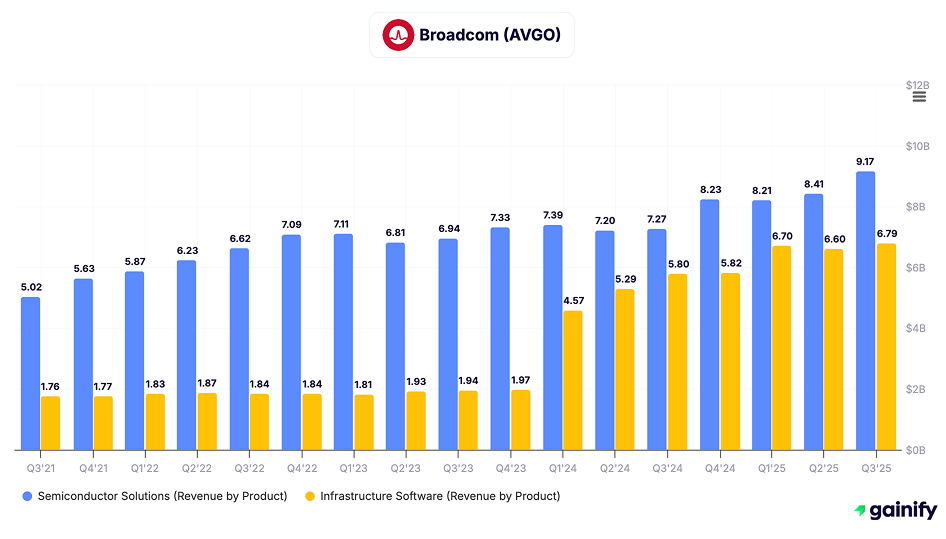

2) Broadcom (AVGO) — $1.67T

Market Cap: $1.67 trillion

2025E Revenue: $60.65 billion

Analyst Target Price Upside: +7.82 %

2025E P/E: 49.91x

What it does:

Broadcom designs and supplies a wide range of semiconductor and infrastructure software products. Its semiconductor portfolio includes networking, broadband, wireless, and custom silicon solutions that are essential for data centers, AI infrastructure, and enterprise connectivity. Following its acquisition of VMware, Broadcom has also become a major player in virtualization and cloud software.

Key investment theses:

- AI networking leadership: Strong position in high-speed networking chips and custom silicon for AI data centers supports multi-year growth.

- Diversified business mix: Balanced exposure across semiconductors and enterprise software provides earnings stability.

- Recurring revenue base: VMware integration expands Broadcom’s recurring software revenue, enhancing predictability and margins.

- Cash generation: Exceptional free cash flow allows for consistent dividend growth and share repurchases.

Recent developments:

- VMware integration: Broadcom completed the integration of VMware in 2025, restructuring its licensing model toward subscriptions and recurring revenue.

- AI-driven demand: Networking and custom ASIC solutions are benefiting from hyperscaler AI infrastructure spending.

- Operational efficiency: Cost synergies from VMware are exceeding initial expectations, driving stronger profitability.

- Expansion into software: Continued investment in security, automation, and infrastructure management platforms strengthens Broadcom’s enterprise footprint.

Key risks:

- Integration challenges: Large-scale integration of VMware may face customer churn and execution risks.

- Regulatory oversight: Broadcom’s size and acquisitions attract antitrust scrutiny in key markets.

- Cyclicality in semiconductors: Demand for networking and broadband chips remains tied to global capital spending cycles.

- Valuation sensitivity: A high forward P/E and rapid multiple expansion leave limited margin for error if growth slows.

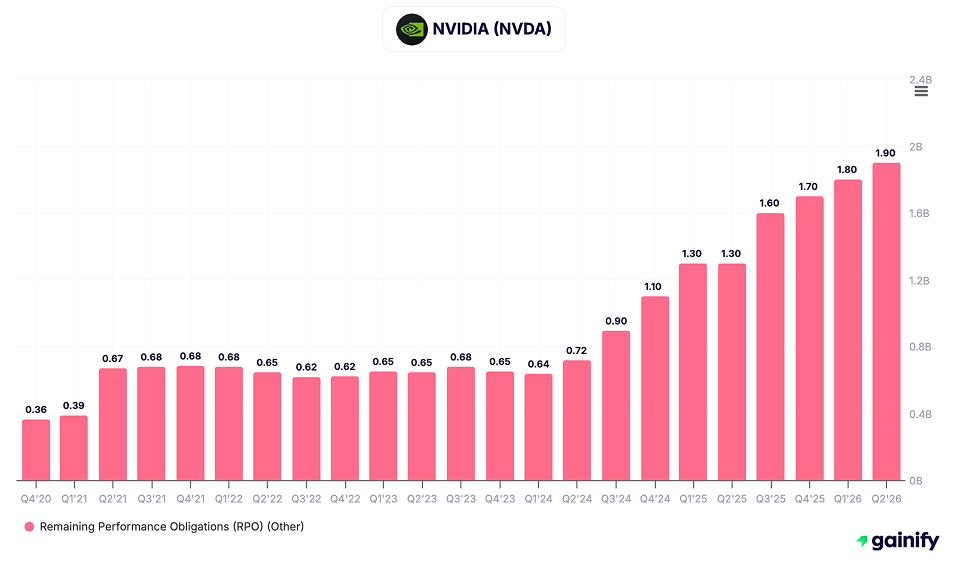

1) NVIDIA (NVDA) — $4.53T

Market Cap: ~$4.53 trillion

2025E Revenue: ~$55.44 billion

Analyst Target Price Upside: +12.5%

2025E P/E: ~41.30x

What it does:

NVIDIA designs and manufactures high-performance GPUs and AI systems that power data centers, gaming, autonomous vehicles and edge-computing infrastructure. Its hardware and software ecosystem (including CUDA, DGX systems, networking) play a central role in the AI computing pipeline.

Key investment theses:

- Massive structural tailwinds from generative AI, inference/workload growth and the increasing value of compute intensity.

- Strong ecosystem lock-in: hardware + software + developer community create high switching costs for customers.

- Innovation leadership: constant refresh of architecture (e.g., Blackwell, next-generation platforms) keeps NVIDIA ahead of many competitors.

- Monetisation expansion: from GPUs into systems, networking, software, and licensing which increases margin leverage.

Recent developments (October 2025):

- NVIDIA announced a landmark partnership with OpenAI to deploy at least 10 gigawatts of NVIDIA systems, under a deal valued around $100 billion.

- NVIDIA joined a consortium including BlackRock and Microsoft Corporation to acquire Aligned Data Centers in a $40 billion deal to secure AI-infrastructure capacity.

- The U.S. approved some NVIDIA chip exports to the United Arab Emirates (UAE) under an agreement for up to 500,000 advanced chips per year starting 2025, improving access to a key region.

Key risks:

- Export controls and geopolitical tensions (especially China) could severely limit NVIDIA’s addressable market.

- Supply constraints: demand for GPUs is extremely high, and any manufacturing or sourcing bottleneck could hamper growth.

- Valuation risk: at a high P/E multiple, even small execution missteps or slower growth could lead to a sharp correction.

- Competition: Other firms (custom silicon, in-house solutions) may erode parts of NVIDIA’s dominance over time.

Conclusion: The Chips Powering Tomorrow’s Economy

Semiconductors are no longer a cyclical curiosity tied to gadget demand. They are the foundation of the modern economy. Every wave of innovation, from artificial intelligence and cloud computing to electric vehicles and 5G connectivity, depends on faster, smaller, and more efficient chips.

The world’s largest semiconductor companies have become indispensable to global growth. They combine technological leadership with scale, capital intensity, and strategic importance that few other industries can match. Whether it is NVIDIA defining the AI infrastructure stack, TSM enabling global chip manufacturing, or ASML pushing the limits of physics, each company in this top 12 list plays a distinct and critical role in how technology evolves.

For investors, the sector’s long-term appeal lies in its combination of secular demand growth, moat-driven profitability, and strategic relevance. However, semiconductors remain a capital-heavy and geopolitically sensitive business, which means volatility will continue to accompany innovation.

Looking ahead, the next decade of semiconductor leadership will be shaped by three forces:

- AI and accelerated computing transforming data centers and devices.

- Manufacturing realignment across the United States, Europe, and Asia for supply chain resilience.

- Energy efficiency and advanced materials driving breakthroughs in performance and sustainability.

Investors who can look beyond short-term cycles and focus on durable business models, cash flow strength, and innovation leadership are likely to find that semiconductors remain one of the world’s most powerful engines of long-term wealth creation.