Transportation stocks are entering 2026 with a setup that is materially easier to underwrite than it has been in recent years. Many companies in the sector have already adjusted to higher labor costs, normalized demand patterns, and a more disciplined regulatory environment. What is increasingly visible now is tighter cost control, improved asset utilization, and a clearer focus on free cash flow generation rather than volume growth alone.

Wall Street analysts have responded by concentrating on transportation businesses that demonstrate consistent execution and margin durability. Conviction is strongest around companies that can translate operational improvements and pricing discipline into sustainable earnings growth, even in a more mature demand environment. Management commentary and investor materials are increasingly centered on efficiency, return on capital, and capital allocation rather than expansion narratives.

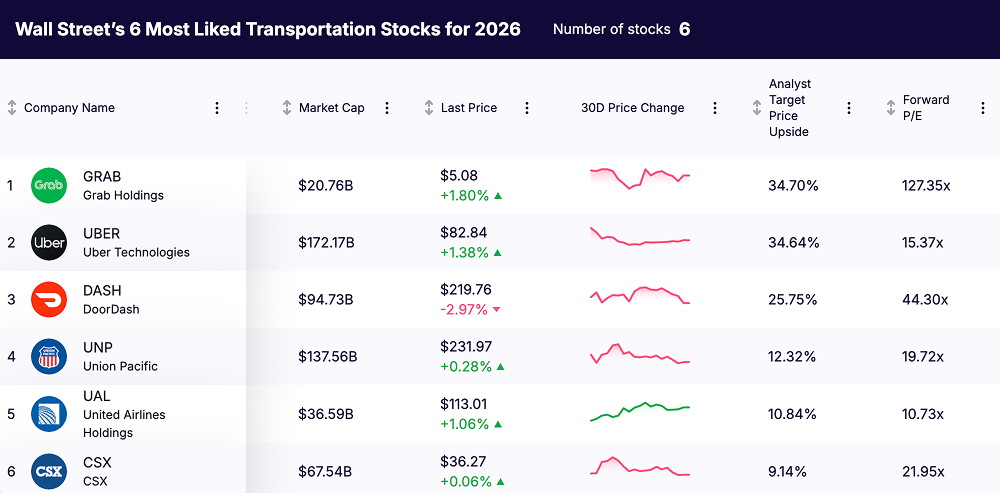

In this article, we highlight six transportation stocks with the highest upside potential based on Wall Street analyst targets and sentiment. These names are among the most liked by analysts heading into 2026, reflecting confidence in their business models and ability to compound value through execution and cash generation. This is less about cyclical recovery and more about identifying transportation leaders with durable upside driven by fundamentals.

Article Highlights

- Six transportation stocks with the highest upside potential for 2026, based on Wall Street analyst targets and sentiment: Uber, Grab, DoorDash, Union Pacific, United Airlines, and CSX

- Analyst conviction centered on earnings growth driven by execution, pricing discipline, and operating leverage, not macro tailwinds

- A deliberate mix of platform-based transportation leaders and asset-heavy operators, offering distinct risk-return profiles

- Clear visibility into margin expansion and free cash flow generation into 2026, supported by management guidance

1. Grab Holdings (NASDAQ: GRAB)

What the company does

Grab is the dominant on-demand platform across Southeast Asia, operating at scale in mobility, food delivery, logistics, and digital financial services. Its advantage comes from dense, multi-product ecosystems in markets where urbanization, smartphone penetration, and cashless payments continue to grow. Rather than relying on a single vertical, Grab monetizes users across multiple services, strengthening engagement and improving unit economics over time.

Key financials

- Market cap: 20.76 billion

- Analyst target price upside: 34.70%

- Forward P/E: 127.35

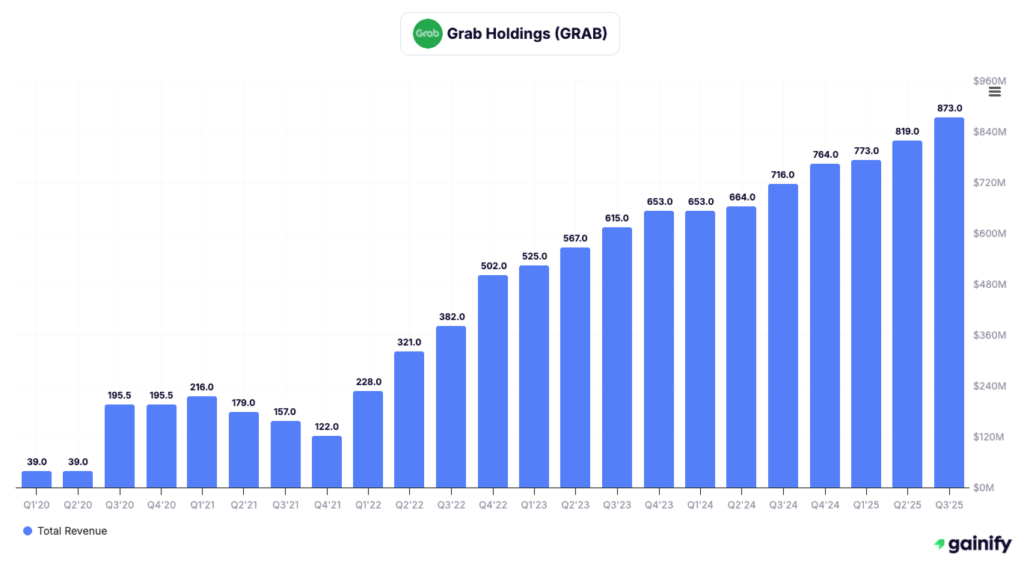

Operationally, Grab delivered revenue growth of 22% year over year in Q3 2025, with on-demand GMV up 24%. Adjusted EBITDA reached 136 million, up 51% year over year, while trailing twelve-month adjusted free cash flow increased to 283 million, improving by 185 million year over year. These metrics reinforce that the company is transitioning from growth-first to profitability-driven execution.

Investment thesis

Grab’s story has shifted from building scale to monetizing scale. Analysts increasingly focus on operating leverage as incentive intensity continues to normalize and higher-margin segments expand. Deliveries GMV growth accelerated for the third consecutive quarter, while financial services loan disbursements grew 56% year over year, reaching an annualized run rate of 3.5 billion. This combination supports margin expansion as revenue grows faster than platform costs.

What to expect next

Margin expansion remains the key driver into 2026. Management has guided to full-year adjusted EBITDA of 490 to 500 million for 2025, representing close to 60% growth year over year. Continued improvement in free cash flow, lower incentives as a share of GMV, and deeper penetration of financial services are central to the bull case.

Key risks

Execution risk across multiple regulatory regimes remains the primary concern. Grab operates in jurisdictions with differing rules around ride-hailing, food delivery, and digital lending. Competitive pressure could reintroduce incentive spending, while credit risk must be carefully managed as the financial services portfolio scales.

2. Uber Technologies (NYSE: UBER)

What the company does

Uber operates the world’s largest on-demand mobility and delivery platform, connecting riders, drivers, couriers, and merchants across more than 70 countries. Its business spans Mobility (ride-hailing), Delivery (food, grocery, and retail), and Freight. What differentiates Uber at this stage is scale-driven efficiency: a global network where increased usage directly improves unit economics, pricing power, and platform monetization across multiple verticals.

Key financials

- Market cap: 172.17 billion

- Analyst target price upside: 34.64%

- Forward P/E: 15.37

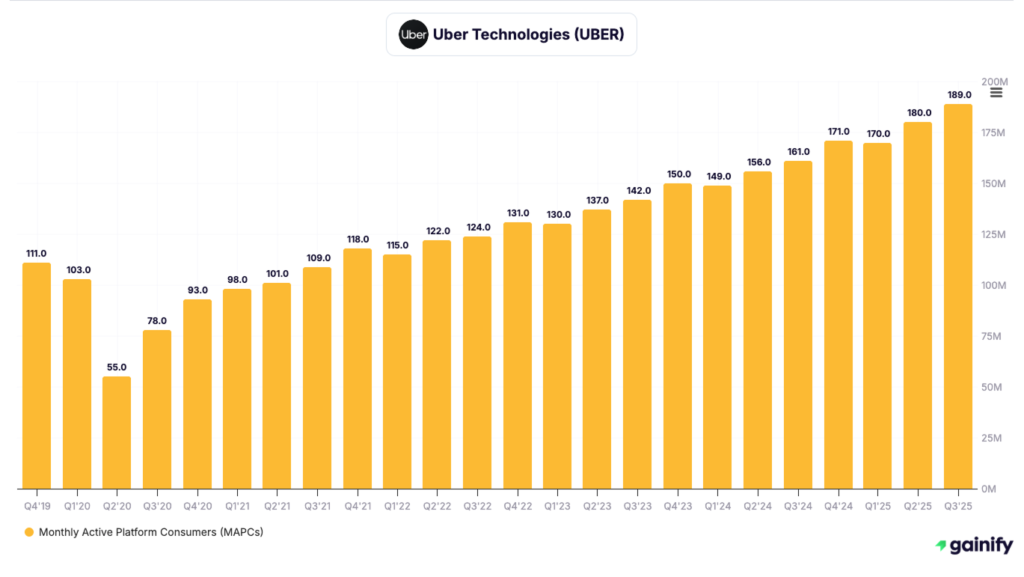

Operationally, Uber continues to deliver consistent, broad-based growth with improving profitability. In Q3 2025, gross bookings increased 21% year over year on a constant-currency basis, while revenue grew 19%. Adjusted EBITDA reached 2.26 billion for the quarter, up 33% year over year, with margins expanding across both Mobility and Delivery. Trailing twelve-month free cash flow rose to 8.66 billion, with free cash flow conversion exceeding 100% of adjusted EBITDA, underscoring strong cash generation across the platform.

Investment thesis

Uber has transitioned from a growth-at-all-costs platform into a durable cash-generating business with multiple embedded growth engines. Analysts increasingly focus on operating leverage as trip volumes rise, frequency improves, and newer verticals such as grocery, retail, and advertising scale within the ecosystem. Mobility margins remain structurally strong, while Delivery continues to show improving profitability as scale and efficiency gains compound.

What to expect next

Into 2026, Wall Street expects continued margin expansion driven by higher trip frequency, disciplined cost control, and deeper monetization of the Delivery platform beyond restaurants. Grocery and retail are expanding Uber’s addressable market meaningfully, while management remains focused on sustaining free cash flow growth and returning capital through share repurchases. Any incremental upside from advertising or autonomy partnerships is viewed as optional rather than core to the base case.

Key risks

The primary risks center on regulatory developments around driver classification, competitive intensity in both Mobility and Delivery, and macro sensitivity tied to consumer demand. While Uber’s scale provides insulation, renewed price competition or unfavorable regulatory changes could pressure margins and slow the pace of earnings expansion.

3. DoorDash (NASDAQ: DASH)

What the company does

DoorDash is the leading local commerce platform in North America, connecting consumers, merchants, and drivers across food delivery, grocery, convenience, and an expanding suite of merchant services. While best known for restaurant delivery, the company has steadily evolved into a broader commerce infrastructure provider, supporting order fulfillment, advertising, payments, and logistics for local businesses both on and off its marketplace.

Key financials

- Market cap: 94.73 billion

- Analyst target price upside: 25.75%

- Forward P/E: 44.30

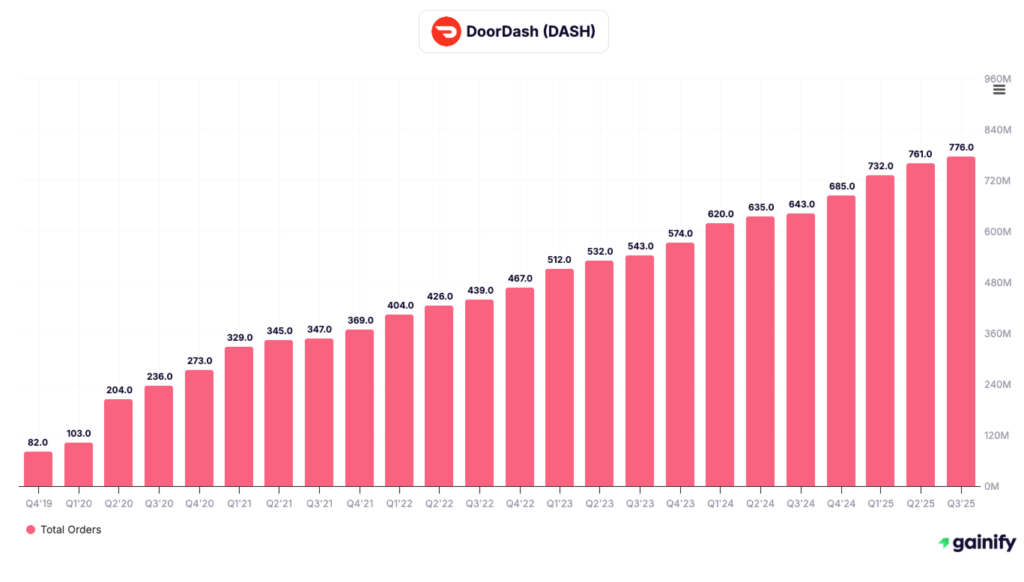

Operationally, DoorDash continues to demonstrate strong scale advantages. Revenue reached 3.45 billion in Q3 2025, up meaningfully year over year, while operating income improved to 258 million for the quarter. The business generated 2.01 billion in operating cash flow over the first nine months of 2025, underscoring improving cash generation as unit economics mature. International operations, including Wolt, are contributing an increasing share of growth, while advertising and merchant services continue to expand margins.

Investment thesis

DoorDash is transitioning from a pure delivery growth story into a profitable local commerce platform. Analysts focus on the company’s ability to monetize its merchant base through higher-margin services such as advertising, white-label logistics, and software tools. With leading market share in the U.S., improving international execution, and rising contribution margins, DoorDash offers earnings leverage as order growth, take rates, and ancillary services scale together.

What to expect next

Into 2026, investors will be watching continued margin expansion, particularly through advertising growth and Commerce Platform services. Management’s focus remains on disciplined cost control, steady international expansion, and increasing free cash flow generation. Additional upside could come from deeper penetration in grocery and non-restaurant verticals, where order frequency and basket sizes are structurally higher.

Key risks

Competitive intensity remains a core risk, particularly if pricing pressure or incentives reaccelerate. Regulatory scrutiny around gig worker classification and merchant fees could impact margins in certain jurisdictions. Additionally, international expansion introduces execution risk, as profitability profiles vary by market and require localized operational discipline.

4. Union Pacific (NYSE: UNP)

What the company does

Union Pacific is one of the largest freight transportation companies in North America, operating an extensive rail network that serves industrial, agricultural, energy, and consumer markets. The company plays a critical role in U.S. supply chains, moving bulk commodities, finished goods, and intermodal freight with high asset intensity and long-lived infrastructure. Its network scale and geographic reach create durable competitive advantages that are difficult to replicate.

Key financials

- Market cap: 137.56 billion

- Analyst target price upside: 12.32%

- Forward P/E: 19.72

Operationally, Union Pacific has made measurable progress on efficiency and service reliability. Freight car velocity and terminal dwell times improved through 2025, while service performance reached near-record levels. These gains have supported pricing discipline and volume recovery across key segments, including industrial and bulk categories. The company continues to generate strong operating cash flow, enabling consistent dividends and share repurchases.

Investment thesis

Union Pacific’s appeal lies in its ability to compound earnings through operational excellence rather than volume growth alone. Analysts favor the company’s focus on safety, service reliability, asset utilization, and cost control, which together support margin stability across cycles. Improved service levels also position Union Pacific to capture incremental freight demand as customers prioritize reliability and efficiency.

What to expect next

Wall Street expects continued improvement in operating efficiency and disciplined capital allocation in 2026. Management has outlined targets for high single- to low double-digit earnings growth, supported by pricing initiatives, productivity gains, and ongoing share repurchases. Incremental upside may come from improved network fluidity and selective volume growth in industrial and bulk markets.

Key risks

Union Pacific remains exposed to economic cyclicality, particularly in industrial demand. Labor availability, regulatory oversight, and weather-related disruptions can affect network performance. While pricing power is strong, sustained volume weakness or cost inflation could pressure margins if not offset by productivity gains.

5. United Airlines Holdings (NASDAQ: UAL)

What the company does

United Airlines is one of the largest global airline platforms, operating an extensive domestic and international network with leading positions across transatlantic, transpacific, and Latin American routes. The company combines a scale-driven hub system with a high-margin loyalty ecosystem anchored by MileagePlus, positioning United as both a transportation operator and a durable consumer platform.

Key financials

- Market cap: 36.59 billion

- Analyst target price upside: 10.84%

- Forward P/E: 10.73

Operationally, United generated total operating revenue of 43.7 billion in the first nine months of 2025, up from 42.4 billion year over year. Net income reached 2.3 billion over the same period, while operating cash flow totaled 7.1 billion. The balance sheet shows 6.7 billion in cash and equivalents, alongside continued progress in debt reduction and disciplined capital allocation.

Investment thesis

United’s investment case centers on earnings durability rather than cyclical recovery. Analysts favor the company’s premium-heavy route mix, strong international exposure, and the structural profitability of its loyalty program. MileagePlus continues to generate stable, high-margin revenue streams through co-branded credit card partnerships and deferred revenue growth, supporting valuation through the cycle.

What to expect next

Into 2026, the focus remains on margin stability, fleet modernization, and shareholder returns. United has resumed share repurchases, reduced secured debt tied to loyalty assets, and continues to invest in next-generation aircraft to improve fuel efficiency and unit costs. Earnings visibility is supported by advance ticket sales growth and disciplined capacity deployment.

Key risks

Airline equities remain sensitive to fuel price volatility, labor negotiations, and macroeconomic demand shifts. United also faces execution risk tied to aircraft delivery timing and regulatory oversight. While leverage has improved, the capital-intensive nature of the business limits flexibility during demand shocks.

6. CSX (NASDAQ: CSX)

What the company does

CSX is a leading freight transportation company operating a dense rail network across the eastern United States. Its network connects major population centers, ports, and industrial hubs, making it a critical link in domestic supply chains. CSX transports a diversified mix of intermodal freight, merchandise, and energy-related commodities, with a business model built around high asset utilization, long-lived infrastructure, and disciplined pricing.

Key financials

- Market cap: 67.54 billion

- Analyst target price upside: 9.14%

- Forward P/E: 21.95

In Q3 2025, CSX reported revenue of 3.59 billion and adjusted operating income of 1.25 billion, translating to an adjusted operating margin of 34.9%. Year-to-date operating cash flow totaled 3.23 billion, while free cash flow before dividends reached 1.07 billion despite over 850 million of temporary cash outflows related to network rebuild spending and deferred tax payments. Safety and efficiency metrics continued to improve, with fuel efficiency declining to 0.94 gallons per thousand gross ton-miles and car miles per day rising to 136.6, the highest level in the period shown.

Investment thesis

CSX’s investment case is centered on operational discipline and incremental margin improvement rather than volume-driven growth. Analysts highlight sustained gains in network efficiency, service reliability, and asset productivity as key drivers of earnings durability. As temporary network investment spending rolls off, free cash flow conversion is expected to improve, supporting shareholder returns through dividends and share repurchases.

What to expect next

Heading into 2026, expectations are focused on continued efficiency gains, normalization of capital spending following major network projects, and steady pricing execution. Management has guided to full-year volume growth in 2025 and a balanced approach to capital allocation, with capex of 2.5 billion excluding hurricane rebuild spending. Improved service metrics position CSX to capture incremental intermodal demand as supply chains stabilize.

Key risks

CSX remains exposed to economic cyclicality across industrial, agricultural, and energy markets. Volume softness in certain merchandise categories, weather-related disruptions, and regulatory oversight can affect near-term performance. While pricing power is strong, sustained cost inflation or weaker demand could pressure margins if not offset by productivity improvements.

Final Thoughts

Wall Street’s top transportation picks for 2026 are not defined by cyclical optimism or recovery narratives. They are defined by execution. Across Grab, Uber, DoorDash, Union Pacific, United Airlines, and CSX, analysts are consistently favoring companies that have already proven their ability to operate efficiently, protect margins, and convert scale into durable cash flow.

Despite operating in different segments, these businesses share common traits that matter in today’s market: pricing discipline, improving unit economics, and a clear framework for capital allocation. Analyst upside expectations are rooted in tangible drivers such as margin expansion, productivity gains, and free cash flow growth, rather than assumptions about macro acceleration or multiple expansion.

For investors, the opportunity heading into 2026 is increasingly about selectivity. Transportation is no longer a broad beta trade. The stocks highlighted in this article represent where Wall Street sees the most attractive upside relative to fundamentals, with risk profiles that are transparent and actively managed. In a market that rewards consistency and execution, these names stand out as long-term compounders rather than short-term trades.

Disclaimer

This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investing in equities involves risk, including the potential loss of principal. Readers should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.