The best psychedelic stocks are approaching a point where promise starts to give way to proof. After years defined by early-stage research, regulatory uncertainty, and shifting investor sentiment, the psychedelic medicine space is now moving into a phase where clinical data, trial design, and capital discipline matter far more than narrative.

As mental health remains one of the most under-treated areas in medicine, companies developing psychedelic and psychedelic-inspired therapies are increasingly being evaluated on their ability to deliver durable, scalable outcomes rather than theoretical potential.

What makes 2026 particularly important is timing. Several leading developers are moving through Phase 2 and Phase 3 trials, regulatory frameworks are becoming clearer, and capital markets are beginning to differentiate between companies with credible data and those still driven by narrative. This transition favors businesses with strong science, focused pipelines, and enough financial runway to reach meaningful milestones.

In this article, we highlight eight psychedelic stocks to watch in 2026, ranging from pure-play clinical-stage developers to larger neuroscience companies with psychedelic-adjacent exposure. We break down what each company does, key financials, upcoming catalysts, investment thesis, and the risks investors need to understand.

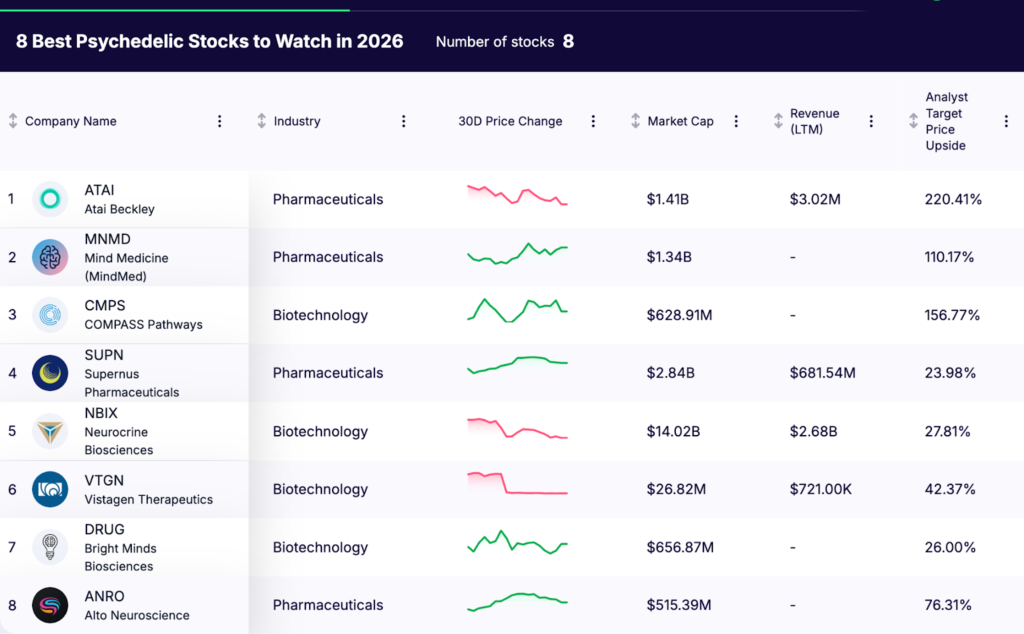

The companies covered include Atai Beckley, MindMed, Compass Pathways, Supernus Pharmaceuticals, Neurocrine Biosciences, Vistagen Therapeutics, Bright Minds Biosciences, and Alto Neuroscience.

Article Highlights

- Multiple companies approaching Phase 2b and Phase 3 readouts in depression, anxiety, and PTSD, with regulatory decisions likely to shape the sector in 2026

- Exposure across distinct therapeutic approaches, including synthetic psilocybin, optimized LSD analogs, intranasal and inhaled psychedelics, and non-hallucinogenic neuroplasticity compounds

- A spectrum of risk profiles, from sub-$100M clinical-stage developers to profitable, large-cap neuroscience companies with established commercial platforms

- Upside driven by discrete clinical and regulatory catalysts, balanced against trial execution risk, capital requirements, and evolving FDA frameworks

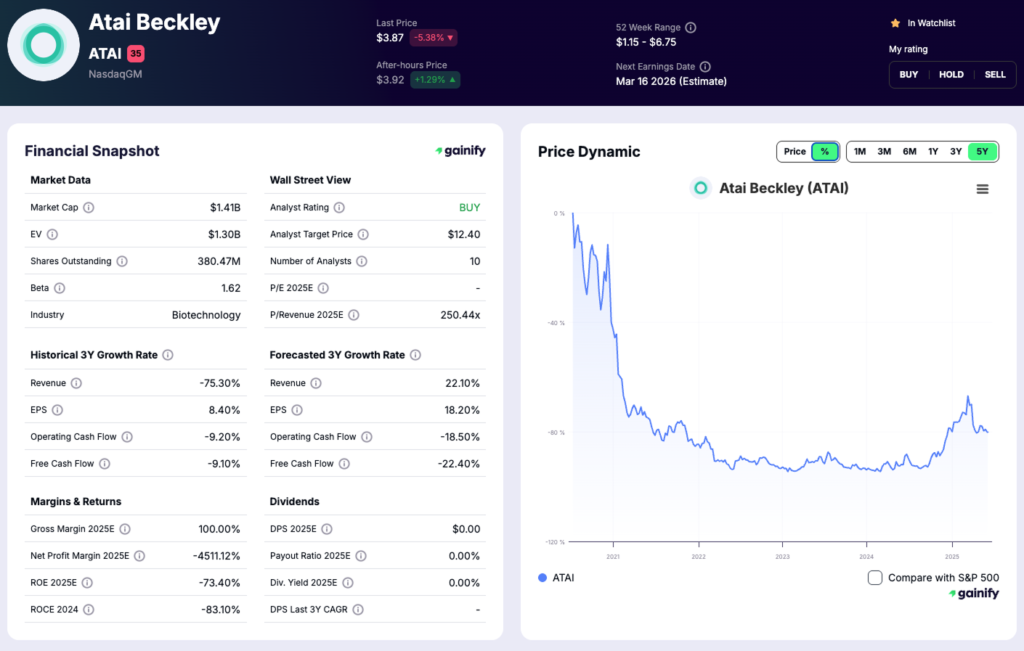

1. Atai Beckley (NASDAQ: ATAI)

What the company does

Atai Beckley is a clinical-stage biopharmaceutical company focused on developing rapid-acting and durable treatments for difficult-to-treat mental health disorders. Following the completion of its strategic combination with Beckley Psytech in November 2025, the company now operates a diversified pipeline of psychedelic and non-psychedelic programs, primarily targeting depression and other neuropsychiatric conditions.

The company’s strategy centers on interventional psychiatry, with an emphasis on compounds designed to deliver meaningful clinical effects with limited dosing rather than chronic daily use.

Key financials

- Market cap: 1.4 billion dollars

- Revenue (LTM): 3.0 million dollars, generated primarily from licensing and R&D services through its Nualtis subsidiary

- Cash and short-term securities: 114 million dollars as of September 30, 2025

- Operating profile: Pre-revenue for core programs with ongoing net losses

Investment thesis

Pipeline breadth and clinical optionality reduce reliance on any single asset, positioning the company to absorb individual trial setbacks while preserving long-term upside across multiple programs.

What to expect next

Advancement of priority programs through late-stage clinical development, alongside disciplined integration and capital allocation following the Beckley Psytech transaction.

Key risks

Sustained cash burn without near-term commercialization, combined with clinical and regulatory uncertainty inherent to central nervous system drug development.

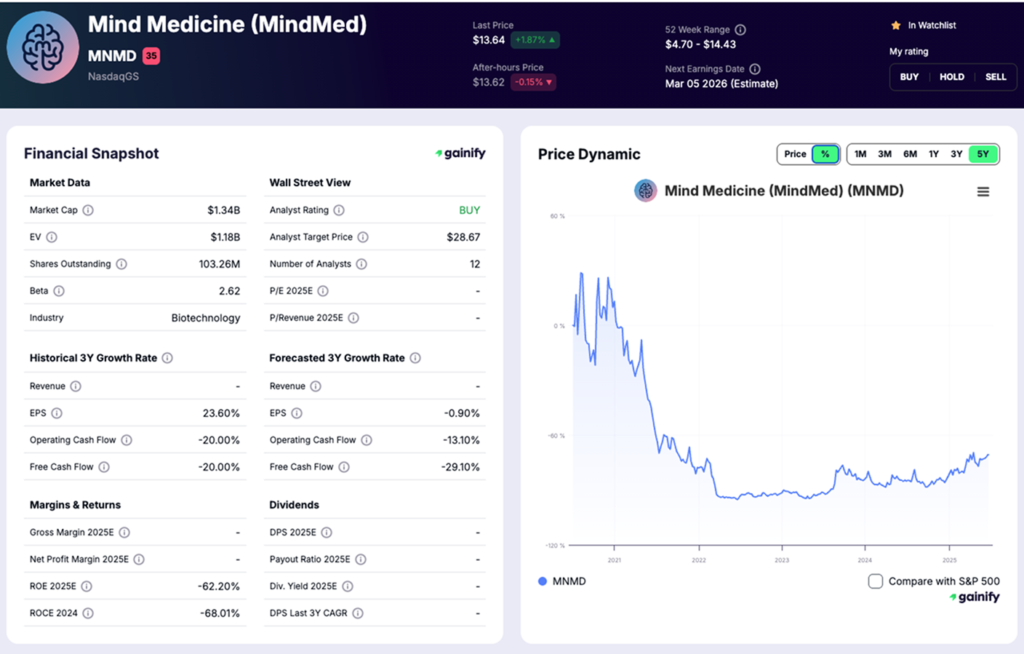

2. MindMed (NASDAQ: MNMD)

What the company does

MindMed is a late-stage neuro-pharmaceutical company developing psychedelic-inspired therapies for large, underserved psychiatric conditions. Its primary focus is generalized anxiety disorder and major depressive disorder, two of the highest-burden mental health categories globally. The company’s strategy centers on single-dose or intermittent treatments designed to deliver rapid and durable clinical benefit without requiring chronic daily administration.

MindMed’s lead program, MM120 ODT, is a pharmaceutically optimized form of lysergide delivered as an oral disintegrating tablet. The company is also advancing MM402, a proprietary R-enantiomer of MDMA, for autism spectrum disorder.

Key financials

- Market cap: 1.34 billion dollars

- Revenue (LTM): None reported

- Cash and short-term securities: 209.1 million dollars as of September 30, 2025

- Net proceeds from October 2025 financing: 242.8 million dollars

- Cash runway: Expected to fund operations into 2028 based on current plans

Investment thesis

MindMed offers one of the most advanced and de-risked clinical setups in the psychedelic space, with MM120 ODT already in multiple Phase 3 trials supported by strong Phase 2b efficacy, favorable tolerability, FDA Breakthrough Therapy Designation, and patent protection extending through 2041.

What to expect next

Three Phase 3 topline readouts in 2026, including two studies in generalized anxiety disorder and one in major depressive disorder, representing the most significant value inflection points in the company’s history.

Key risks

Binary clinical and regulatory outcomes tied primarily to MM120, meaning Phase 3 trial failures, safety concerns, or regulatory pushback could materially impair the investment case despitRegulatory and reimbursement uncertainty.

3. Compass Pathways (NASDAQ: CMPS)

What the company does

Compass Pathways is a late-stage biotechnology company developing psilocybin-based therapies for serious mental health conditions. Its lead program, COMP360, is a synthetic formulation of psilocybin administered in a controlled setting with psychological support. The company’s primary focus is treatment-resistant depression, with additional development activity in post-traumatic stress disorder.

Compass has built an end-to-end platform that includes drug manufacturing, therapist training, site certification, and clinical infrastructure, reflecting the complexity of delivering psychedelic-assisted therapies at scale.

Key financials

- Market cap: 628.91 million dollars

- Revenue (LTM): None reported

- Cash and cash equivalents: 185.9 million dollars as of September 30, 2025

- Operating profile: Late-stage clinical company with no commercial revenue

Investment thesis

Compass is positioned to become the first company to bring a psilocybin-based therapy through FDA approval, supported by statistically significant Phase 3 efficacy data, direct regulatory engagement, and a clearly defined path toward submission.

What to expect next

Multiple Phase 3 data readouts in 2026 across two ongoing trials in treatment-resistant depression, which will be critical in determining the timing and structure of a potential regulatory submission.

Key risks

Regulatory complexity and commercialization execution, including approval requirements for supervised administration, REMS design, reimbursement uncertainty, and the operational challenge of scaling therapist-supported treatment models.

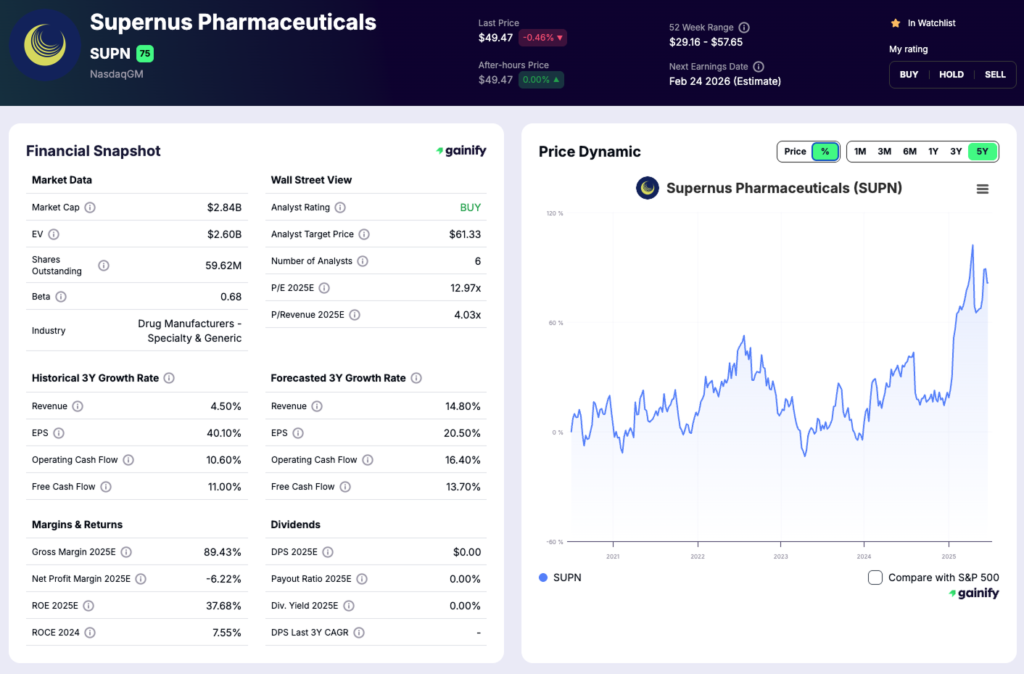

4. Supernus Pharmaceuticals (NASDAQ: SUPN)

What the company does

Supernus Pharmaceuticals is a commercial-stage neuroscience company with a diversified portfolio spanning attention-deficit hyperactivity disorder, Parkinson’s disease, epilepsy, and depression. Unlike pure-play psychedelic developers, Supernus combines established revenue-generating products with a growing pipeline of novel central nervous system therapies, including programs that target neuroplasticity and rapid-onset antidepressant effects.

Key marketed products include Qelbree for ADHD, GOCOVRI for Parkinson’s disease dyskinesia and “off” episodes, ZURZUVAE for postpartum depression through a collaboration, and ONAPGO, a subcutaneous apomorphine infusion device launched in 2025. The company also maintains a research pipeline that includes SPN-817 for epilepsy and SPN-820, a novel intracellular modulator of mTORC1 for major depressive disorder.

Key financials

- Market cap: 2.84 billion dollars

- Revenue (LTM): 681.54 million dollars

- Full-year 2025 revenue guidance: 685 to 705 million dollars

- Operating profile: Commercial-stage company with positive non-GAAP operating earnings

Investment thesis

Supernus offers a lower-risk way to gain exposure to innovation in mental health through a profitable, diversified CNS platform, supported by recurring product revenue and internally developed pipeline assets that can extend growth beyond current franchises.

What to expect next

Continued commercial execution across ADHD, Parkinson’s, and postpartum depression products, alongside advancement of SPN-817 in epilepsy and SPN-820 in depression, with additional clinical updates expected as development programs progress.

Key risks

Exposure to loss of exclusivity on legacy products over time, combined with execution risk in integrating acquisitions and translating early-stage pipeline assets into meaningful commercial contributors.

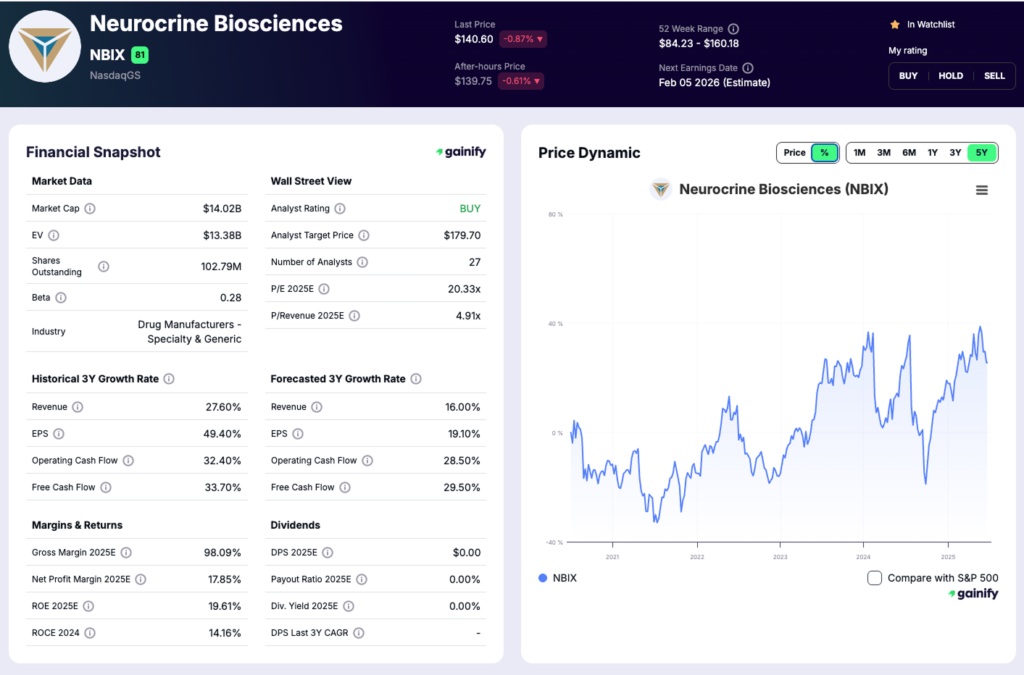

5. Neurocrine Biosciences (NASDAQ: NBIX)

What the company does

Neurocrine Biosciences is a large-cap neuroscience-focused biopharmaceutical company with approved commercial products and one of the deepest late-stage pipelines in psychiatry and neurology. While not a pure-play psychedelic company, Neurocrine is highly relevant to the psychedelic investment theme through its work on rapid-acting antidepressant mechanisms, glutamatergic modulation, and next-generation neuropsychiatric therapies designed to deliver psychedelic-like efficacy without hallucinogenic effects.

The company generates substantial revenue from INGREZZA for tardive dyskinesia and Huntington’s disease chorea, providing durable cash flow to self-fund an expansive research and development engine across psychiatry and neurology. Its psychiatry portfolio includes multiple late-stage programs targeting major depressive disorder and schizophrenia, areas directly adjacent to psychedelic-assisted innovation.

Key financials

- Market cap: 14.02 billion dollars

- Revenue (LTM): 2.68 billion dollars

- Operating profile: Commercial-stage company with positive operating cash flow

Investment thesis

Neurocrine offers a lower-risk way to gain exposure to next-generation mental health innovation, combining a profitable commercial base with a late-stage psychiatry pipeline built around validated biology rather than unproven mechanisms.

What to expect next

Progression of multiple Phase 3 programs in psychiatry, including osavampator for major depressive disorder and direclidine for schizophrenia, alongside continued lifecycle expansion of INGREZZA and advancement of earlier-stage CNS assets.

Key risks

Late-stage clinical trial risk and competitive pressure, particularly as novel depression therapies, including psychedelic-assisted approaches, move closer to commercialization and compete for similar patient populations.

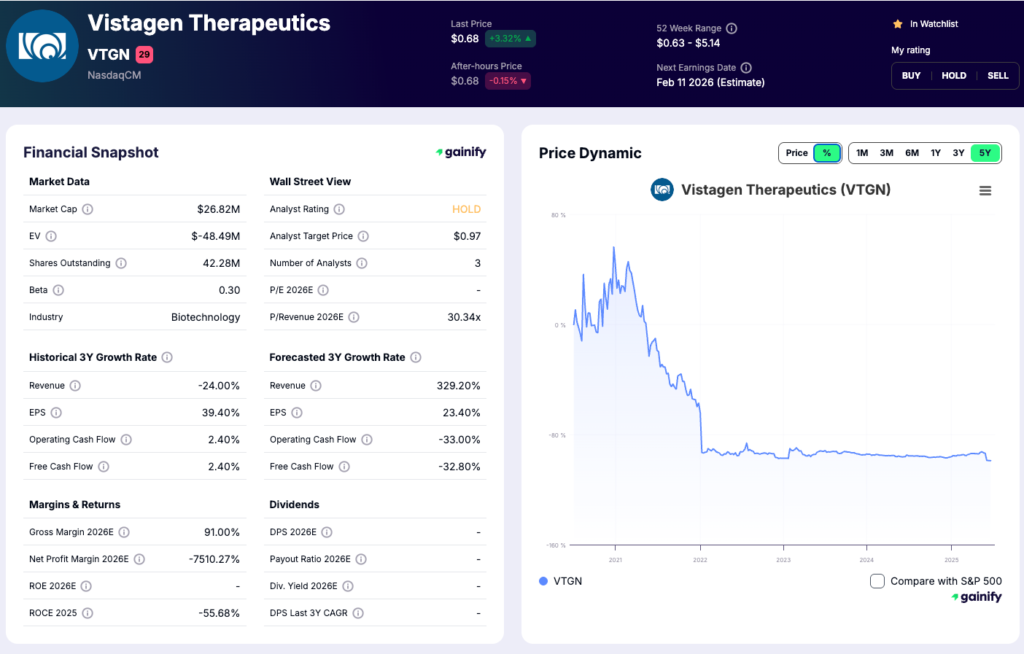

6. Vistagen Therapeutics (NASDAQ: VTGN)

What the company does

Vistagen Therapeutics is a late clinical-stage neuroscience company developing a novel class of intranasal treatments called pherines. Unlike classic psychedelics, pherines are non-systemic compounds designed to rapidly activate nose-to-brain neural circuits without entering the bloodstream or causing hallucinogenic effects. The company is focused on anxiety, depression, and other CNS disorders where rapid-onset relief is clinically valuable.

Its most advanced asset is fasedienol, an intranasal pherine being developed for the acute treatment of social anxiety disorder. Vistagen also has earlier-stage pherine programs targeting major depressive disorder, menopausal symptoms, mental fatigue, and cancer-related conditions.

Key financials

- Market cap: 26.82 million dollars

- Revenue (LTM): 0.72 million dollars

- Cash, cash equivalents, and marketable securities (Sept 30, 2025): 77.2 million dollars

Investment thesis

Vistagen’s differentiated thesis is centered on rapid, non-systemic CNS modulation, positioning pherines as potentially safer, faster-acting alternatives to traditional psychiatric drugs. Fasedienol has already demonstrated positive Phase 3 data in PALISADE-2, showing acute anxiety reduction without sedation or abuse potential. If ongoing Phase 3 trials confirm efficacy, Vistagen could occupy a unique niche in acute anxiety treatment where few effective options exist today.

What to expect next

Multiple near-term clinical readouts define the company’s trajectory. Topline data from the PALISADE-3 Phase 3 trial for fasedienol is expected in the fourth quarter of 2025, with PALISADE-4 and a repeat-dose Phase 2b study expected in the first half of 2026. These results will be critical for regulatory positioning and determining whether fasedienol can support an FDA submission.

Key risks

Clinical and financing risk remain elevated despite late-stage progress. Vistagen continues to generate operating losses and disclosed substantial doubt about its ability to continue as a going concern beyond twelve months without additional capital. Failure of upcoming Phase 3 trials, delays in regulatory alignment, or shareholder dilution from future financing could materially impact the investment case.

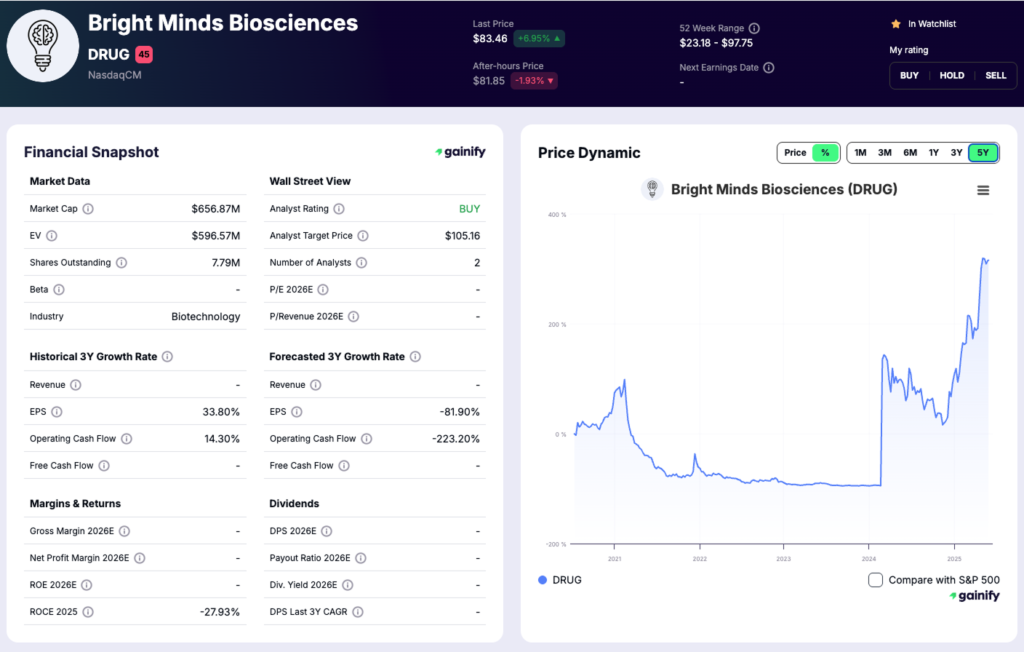

7. Bright Minds Biosciences (NASDAQ: DRUG)

What the company does

Bright Minds Biosciences is a clinical-stage neuroscience company developing highly selective serotonin receptor agonists designed to deliver the therapeutic benefits associated with psychedelics while avoiding hallucinogenic effects and safety liabilities. The company’s platform focuses on targeted modulation of 5-HT2 receptors, with programs spanning rare epilepsies, neurodevelopmental disorders, and neuropsychiatric conditions such as depression and anxiety.

Its lead asset, BMB-101, is a first-in-class, G-protein-biased 5-HT2C agonist being developed for absence epilepsy and developmental and epileptic encephalopathies. Bright Minds also has earlier-stage 5-HT2A agonist programs, BMB-201 and BMB-202, designed to induce neuroplasticity with short or minimal psychoactive effects, positioning them as next-generation alternatives to traditional psychedelic therapies.

Key financials

- Market cap: 656.87 million dollars

- Revenue (LTM): Not reported

- Cash runway: Management has guided to funding into 2027

Investment thesis

Bright Minds is targeting high-unmet-need CNS indications with a differentiated receptor-selective approach, aiming to capture psychedelic-like efficacy while improving safety, tolerability, and chronic usability. BMB-101 has demonstrated favorable Phase 1 safety, clear target engagement, and early signals supporting its mechanism in epilepsy, a space where treatment resistance remains common. If clinical efficacy is confirmed, the company could establish a best-in-class position in niche but commercially meaningful epilepsy markets, with optional upside from its broader neuropsychiatric pipeline.

What to expect next

Clinical execution in Phase 2 is the primary value driver. BMB-101 is currently being evaluated in an open-label Phase 2 BREAKTHROUGH study in adults with absence seizures and developmental and epileptic encephalopathies, with seizure frequency, EEG markers, and quality-of-life measures as key endpoints. Progression toward randomized controlled studies, alongside advancement of the Prader-Willi syndrome program and preclinical 5-HT2A assets, will shape investor perception through 2026.

Key risks

Clinical, regulatory, and concentration risk are central to the story. The company remains pre-revenue and heavily dependent on the success of BMB-101. Failure to demonstrate meaningful seizure reduction or durability in Phase 2 could materially impair the investment case. Additional risks include regulatory uncertainty around novel serotonin-based therapies, execution risk as programs expand into multiple indications, and potential dilution if capital needs increase ahead of pivotal trials.

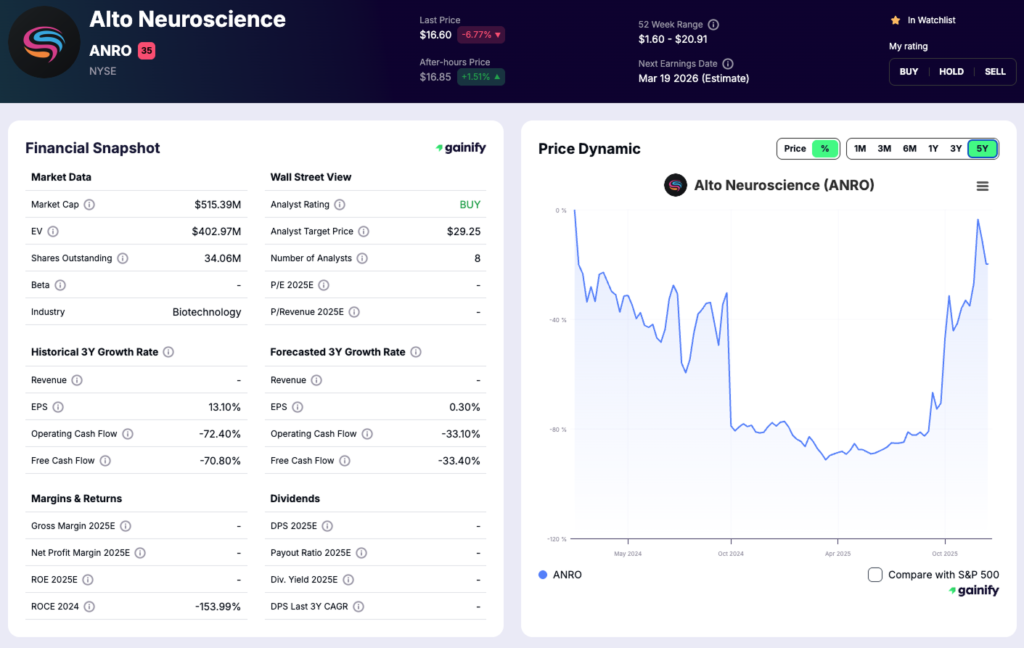

8. Alto Neuroscience (NYSE: ANRO)

What the company does

Alto Neuroscience is a clinical-stage precision psychiatry company developing biomarker-driven treatments for major depressive disorder, treatment-resistant depression, schizophrenia, bipolar depression, and related CNS conditions. Unlike traditional psychiatry approaches that treat heterogeneous patient populations, Alto’s strategy centers on identifying objective biomarkers to prospectively select patients most likely to respond to specific therapies.

The company is advancing a broad portfolio of six clinical programs, including ALTO-207, ALTO-300, ALTO-101, and ALTO-100, each paired with proprietary EEG, cognitive, or behavioral biomarkers. This precision approach is designed to improve efficacy signals, reduce placebo effects, and increase the probability of success in late-stage trials.

Key financials

- Market cap: 515.39 million dollars

- Revenue (LTM): Not reported

- Expected cash runway: Into 2028

Investment thesis

Alto’s core differentiation is its biomarker-first development model, which seeks to fundamentally change how CNS drugs are tested, approved, and prescribed. Lead program ALTO-207 targets treatment-resistant depression using a dopamine D3/D2 agonist combined with a 5-HT3 antagonist to enable faster titration and improved tolerability versus pramipexole alone. Phase 2a data demonstrated robust antidepressant effects with improved safety, supporting progression toward potentially pivotal studies. Across the pipeline, Alto’s ability to stratify patients based on biological signals creates multiple shots on goal with structurally higher signal-to-noise than traditional psychiatry trials.

What to expect next

2026 and 2027 are catalyst-heavy years for Alto. The company expects multiple mid- to late-stage data readouts across its portfolio, including topline Phase 2b data for ALTO-300 in major depressive disorder in mid-2026, topline Phase 2b data for ALTO-101 in cognitive impairment associated with schizophrenia in the first quarter of 2026, and initiation of a Phase 2b trial for ALTO-207 in treatment-resistant depression in the first half of 2026, with topline data expected in 2027. Regulatory feedback on biomarker enrichment strategies will be a key determinant of trial design and commercial positioning.

Key risks

Execution risk is elevated given the complexity of running multiple biomarker-driven trials in parallel. Failure to prospectively validate biomarkers or demonstrate clear efficacy in biomarker-positive populations could undermine the platform’s credibility. While Alto is well-capitalized, the company remains pre-revenue and dependent on clinical success to justify continued investment. Regulatory uncertainty around enrichment strategies, operational risk across decentralized trials, and the need to educate regulators and prescribers on precision psychiatry all represent meaningful hurdles.

Final Thoughts

The psychedelic and next-generation psychiatry sector remains inherently HIGH RISK, but the nature of that risk is changing. As the industry moves into 2026, uncertainty is shifting away from scientific viability and toward execution, regulation, and scale. Several companies are no longer being judged on potential alone, but on their ability to deliver reproducible clinical outcomes, navigate regulatory frameworks, and sustain development through late-stage trials.

For investors, the opportunity lies in selectivity. Pure-play psychedelic developers offer asymmetric upside tied to discrete clinical and regulatory inflection points, while larger neuroscience companies provide a more measured way to participate in innovation with lower binary risk. Understanding where each company sits on that spectrum is critical.

This is not a sector where broad exposure works well. Position sizing, diversification across development stages, and a clear view of upcoming catalysts matter more than thematic enthusiasm. If late-stage data and regulatory clarity materialize as expected, 2026 may be remembered as the year psychedelic medicine began to transition from experimental to investable.

Disclaimer:

This article is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Investing in biotechnology and clinical-stage companies involves substantial risk, including the risk of loss of principal. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.