Digital entertainment stocks across the entertainment ecosystem are entering a structurally different phase than the one that defined the past decade. What was once driven primarily by user acquisition and platform expansion is now increasingly shaped by monetization efficiency, capital discipline, and durable free cash flow generation. After years of rapid growth, elevated content spending, and experimentation across formats, the sector is undergoing a reset that is rewarding scale, pricing power, and operational leverage.

The normalization of advertising markets, maturation of subscription models, and rising costs of content production have forced digital entertainment companies to prioritize returns on invested capital over pure top-line growth. Engagement remains resilient, but monetization has become more competitive and more cyclical, favoring platforms with global reach, diversified revenue streams, and defensible intellectual property.

Looking longer term, digital entertainment remains a structural growth market, supported by continued shifts in consumer time spent online, expanding global connectivity, and the increasing digitization of media, gaming, and interactive content. As emerging technologies enhance personalization, distribution, and monetization, the strongest platforms are positioned to compound earnings over multi-year horizons despite near-term cyclicality.

Against this backdrop, opportunity within digital entertainment stocks has become increasingly selective. Rather than broad exposure, investors are focusing on a concentrated group of platforms with the scale, monetization depth, and financial flexibility to navigate both cyclical volatility and long-term structural change. The six digital entertainment stocks highlighted below represent leading franchises across social media, streaming, gaming, audio, and interactive entertainment, each positioned differently but collectively shaping the next phase of the digital content economy heading into 2026.

Key Highlights

- Sector transition: Digital entertainment stocks are shifting toward monetization efficiency and cash flow discipline, benefiting scaled platforms such as Meta Platforms and Netflix, where pricing power and operating leverage are increasingly visible

- Engagement-driven growth: Interactive and creator-led platforms like Roblox and Spotify Technology continue to deliver strong engagement, with upside tied to improving monetization efficiency rather than user growth alone

- Content and IP leverage: Established franchises at Take-Two Interactive Software provide long-lived monetization through premium content and recurring in-game spending, albeit with cyclical release risk

- Emerging market optionality: Sea adds higher-growth exposure through digital gaming and entertainment in emerging markets, supported by improving capital discipline and cash flow generation

1. Meta Platforms (NASDAQ: META)

- Market capitalization: $1.67 trillion

- Forward P/E: 26.46x

- Analyst target upside: 26.21%

- Forward 3-year revenue CAGR: 18.30%

- Forward free cash flow yield: 2.52%

Business overview

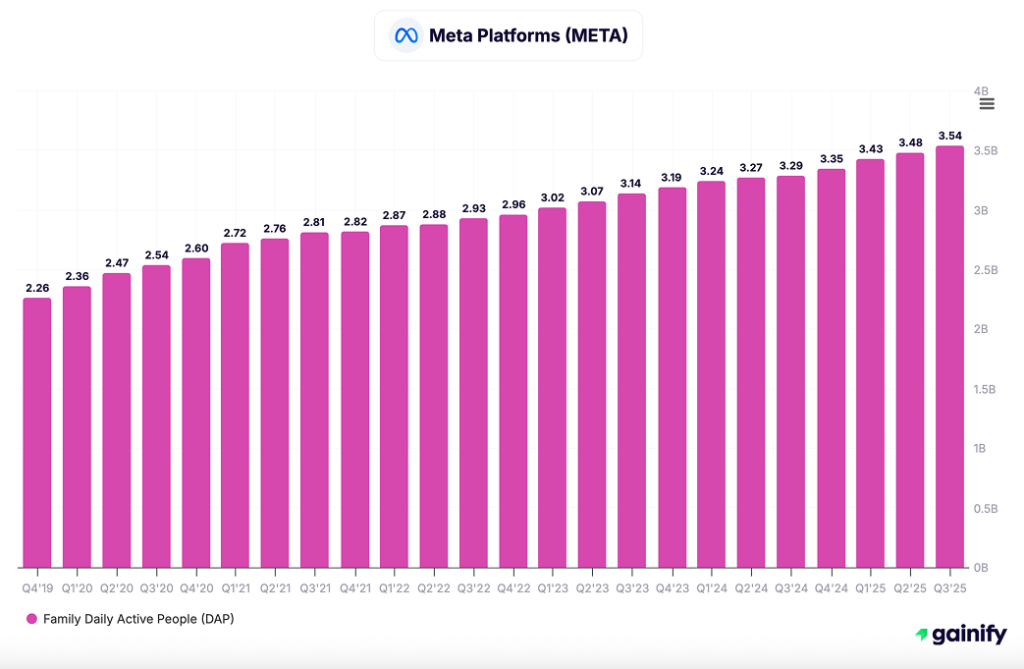

Meta Platforms operates one of the most dominant digital engagement ecosystems globally, spanning social networking, messaging, and short-form video across multiple platforms. Its scale gives it unparalleled access to user attention, behavioral data, and advertiser demand. Advertising remains the core revenue engine, increasingly driven by AI-based ad targeting, improved conversion tools, and better monetization of video and messaging surfaces.

Recent results underscore the durability of this model. Meta generated over $51 billion in quarterly revenue, while operating margins expanded meaningfully as expense growth moderated. Advertising impressions and pricing both contributed, reflecting improved ad performance rather than simple volume expansion.

AI investment and capital intensity

Artificial intelligence is becoming central to Meta’s long-term strategy. The company is investing heavily in AI infrastructure, large language models, and recommendation systems to improve ad targeting, content discovery, and user engagement across its platforms. These investments are driving elevated capital expenditures, particularly in data centers and compute capacity.

While higher capex weighs on near-term free cash flow yield, it strengthens Meta’s competitive positioning by reinforcing its data and infrastructure advantage. For investors, the key trade-off is between short-term capital intensity and long-term monetization leverage, with AI expected to enhance both user experience and advertising efficiency over time.

Investment thesis

Meta’s investment case is anchored in operating leverage at global scale. After several years of elevated investment, management has pivoted decisively toward cost discipline and efficiency, resulting in a sharp rebound in profitability. Operating income has grown faster than revenue, validating the company’s ability to convert engagement into earnings as monetization tools mature.

Importantly, Meta continues to generate tens of billions of dollars in annual operating cash flow, providing flexibility to invest in long-term initiatives while still returning capital through share repurchases. The market’s valuation reflects confidence that Meta can sustain high returns on capital by monetizing its existing user base more effectively, rather than relying on incremental user growth.

For investors, Meta increasingly resembles a cash-generative digital infrastructure platform with embedded growth optionality, rather than a pure growth company dependent on aggressive expansion.

Key risks

- Advertising cyclicality, which can pressure revenue during macro slowdowns

- Regulatory and policy scrutiny, particularly around data use and platform governance

- Ongoing investment needs in emerging technologies that may weigh on margins over shorter periods

2. Netflix (NASDAQ: NFLX)

- Market capitalization: $431.68 billion

- Forward P/E: 37.25x

- Analyst target upside: 33.58%

- Forward 3-year revenue CAGR: 13.30%

- Forward free cash flow yield: 2.13%

Business overview

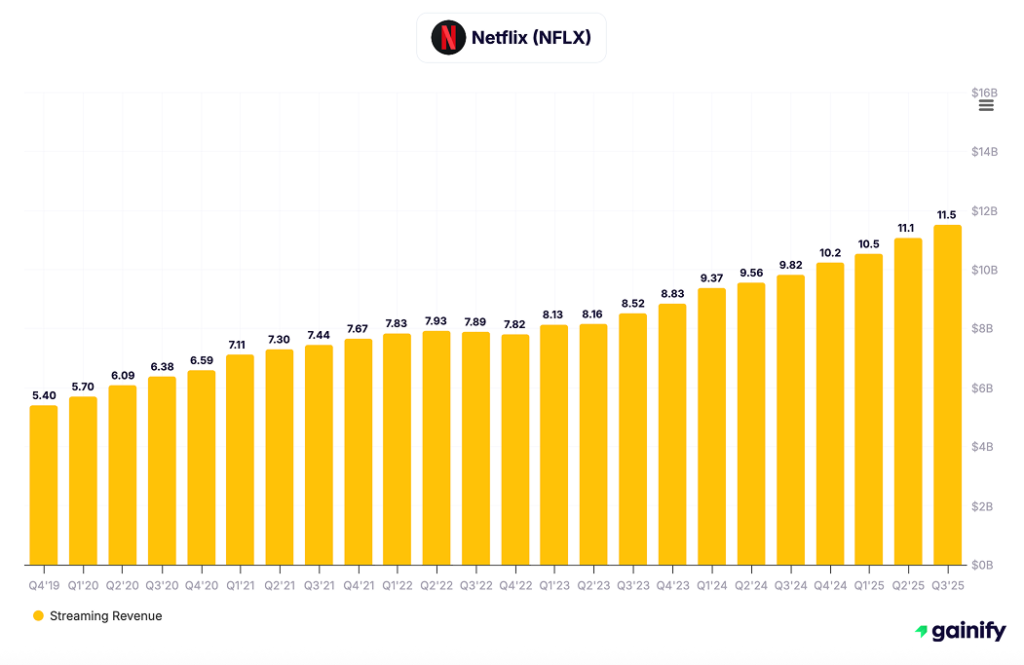

Netflix is the world’s leading global streaming platform, operating in more than 190 countries with a subscription-based model increasingly supported by advertising. The company has shifted from a growth-first strategy toward a framework focused on pricing power, content efficiency, and margin durability.

In Q3 2025, Netflix generated $11.51 billion in revenue and delivered operating income of $3.25 billion, underscoring its ability to convert global scale into meaningful profitability as streaming matures.

Investment thesis

Netflix’s investment case centers on monetizing a fully scaled global platform. With distribution infrastructure largely built, incremental revenue increasingly converts into operating income. Pricing actions, paid-sharing enforcement, and the continued expansion of the ad-supported tier have lifted revenue per membership while preserving engagement.

The company has also demonstrated strategic flexibility around consolidation, having submitted an offer for Paramount. While not core to the base-case thesis, this highlights Netflix’s balance-sheet strength and willingness to selectively expand content depth, intellectual property ownership, and advertising reach.

Overall, the valuation increasingly reflects Netflix as a durable global media franchise, where earnings visibility and free cash flow generation now matter more than subscriber growth alone.

Content strategy, AI, and capital intensity

Netflix continues to invest in data science and machine learning to enhance content discovery, personalization, and commissioning decisions. These tools improve engagement while enabling more disciplined capital allocation across genres and regions.

Content investment remains significant but more controlled. Rather than escalating budgets, management is prioritizing returns on content investment, supporting free cash flow growth alongside revenue.

Key risks

- Content cost inflation, particularly for premium franchises

- Integration and execution risk related to large-scale acquisitions

- Pricing sensitivity in international markets

- Competitive pressure from global and regional streaming platforms

3. Roblox (NYSE: RBLX)

- Market capitalization: $57.71 billion

- Forward P/E: not meaningful

- Analyst target upside: 71.05%

- Forward 3-year revenue CAGR: 39.30%

- Forward free cash flow yield: 2.02%

Business overview

Roblox operates a large-scale digital entertainment platform built around user-generated games and social experiences. The platform monetizes engagement through virtual goods and creator-driven content, creating a model where content supply continuously refreshes without reliance on traditional release cycles.

Investment thesis

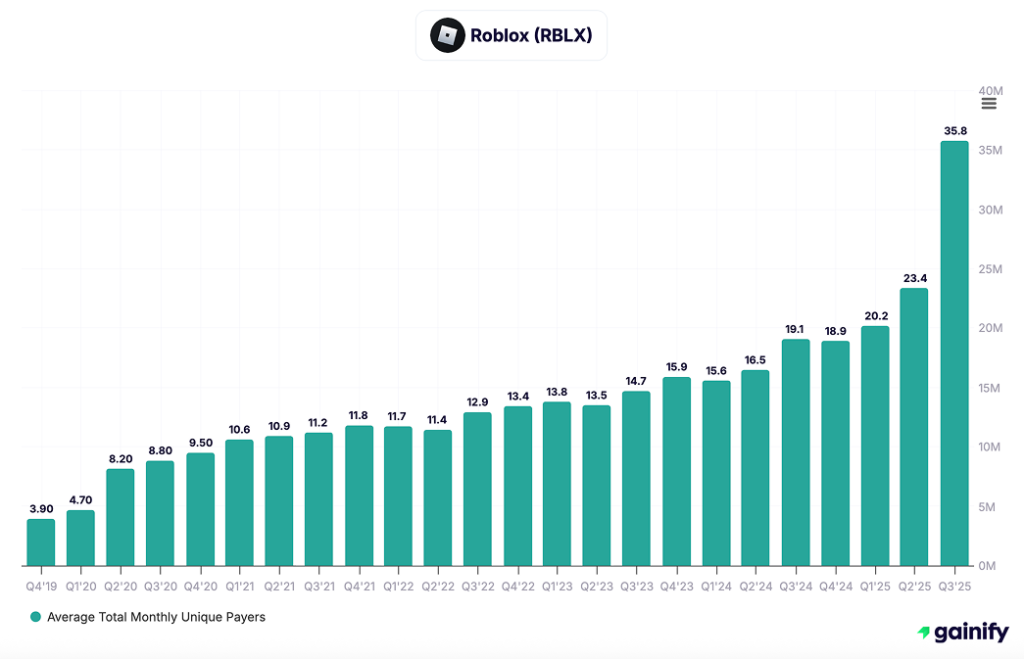

Roblox’s investment case is driven by engagement scale and long-term monetization optionality. In Q3 2025, the platform reached 151.5 million daily active users and generated $1.92 billion in bookings, highlighting both its global reach and the growing economic activity occurring within the ecosystem.

The core question for investors is not engagement leadership, but whether Roblox can translate sustained user growth into durable profitability. With a negative forward P/E and high implied revenue growth, valuation remains highly sensitive to evidence of operating leverage as infrastructure and platform costs mature.

Key risks

- Delayed path to sustained profitability, which can amplify valuation volatility

- Monetization execution risk, particularly beyond core gaming cohorts

- Platform safety and regulatory scrutiny, given a large youth user base

- Dependence on creator ecosystem quality, incentives, and content relevance

4. Spotify Technology (NYSE: SPOT)

- Market capitalization: $120.43 billion

- Forward P/E: 68.02x

- Analyst target upside: 29.24%

- Forward 3-year revenue CAGR: 17.80%

- Forward free cash flow yield: 2.83%

Business overview

Spotify is the leading global audio streaming platform, spanning music, podcasts, and audiobooks across subscription and advertising-supported tiers. Unlike video streaming, audio benefits from daily habitual usage, lower production intensity, and strong global portability, making it structurally resilient across economic cycles.

From a top-down perspective, audio continues to capture a growing share of consumer time, particularly in mobile-first and emerging markets. This provides Spotify with a large, expanding engagement base that can be monetized progressively rather than all at once.

Investment thesis

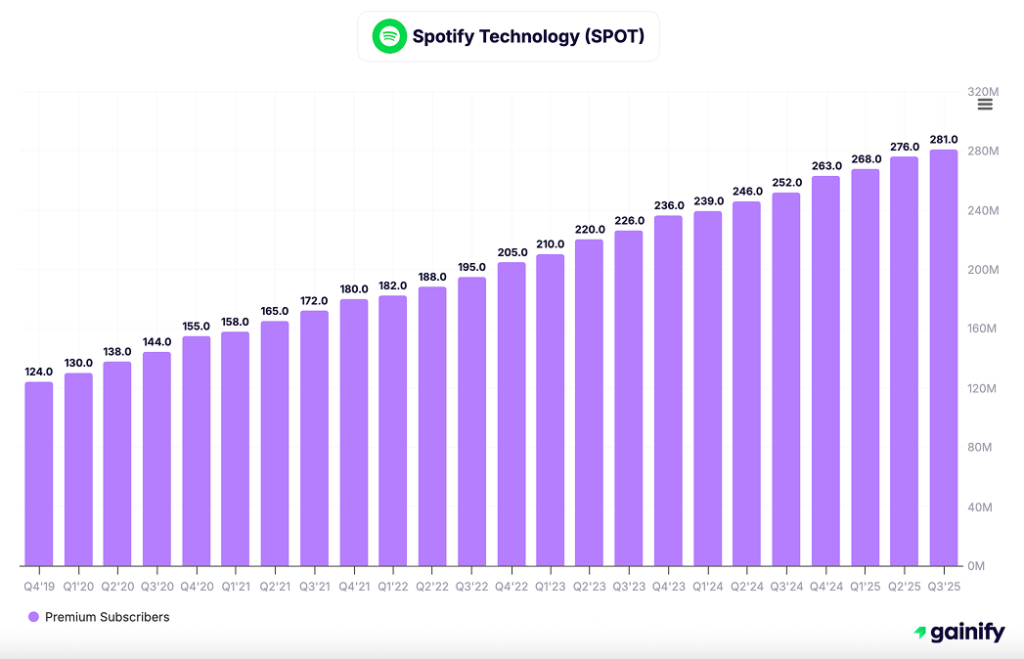

Spotify’s investment case entering 2026 is increasingly defined by operating leverage and cash generation, rather than pure user growth. In Q3 2025, Spotify reported 713 million monthly active users, reinforcing its global scale advantage. More importantly, the company generated €806 million in free cash flow during the quarter, demonstrating that scale is now translating into meaningful financial output. Operating income reached €582 million, reflecting expanding margins as cost discipline improves across content, marketing, and overhead.

At a sector level, Spotify is positioned at the intersection of three favorable trends: growth in global audio consumption, gradual recovery in digital advertising, and improved monetization efficiency from scale. As licensing economics stabilize and non-music formats mature, incremental revenue increasingly flows through to cash flow.

The valuation embeds high expectations, but unlike earlier phases of the business, those expectations are now supported by demonstrated profitability and balance-sheet flexibility, rather than distant assumptions.

Key risks

- Content licensing cost inflation, particularly with major music labels

- Advertising cyclicality, which can pressure near-term margins

- Execution risk in scaling podcasts and audiobooks into durable profit pools

5. Sea (NYSE: SE)

- Market capitalization: $75.69 billion

- Forward P/E: 36.57x

- Analyst target upside: 49.37%

- Forward 3-year revenue CAGR: 24.80%

- Forward free cash flow yield: 4.33%

Business overview

Sea operates a diversified digital ecosystem across Southeast Asia and other emerging markets, spanning e-commerce, digital financial services, and digital entertainment. Within digital entertainment, the company is anchored by Garena, which publishes and operates live-service games with deep regional penetration and long user lifecycles.

From a top-down perspective, Sea benefits from structural tailwinds in emerging markets, including rising smartphone penetration, improving digital payments infrastructure, and a growing middle class spending more time and money on digital content. Digital entertainment plays a critical role in this ecosystem by generating engagement and cash flow that supports broader platform expansion.

Investment thesis

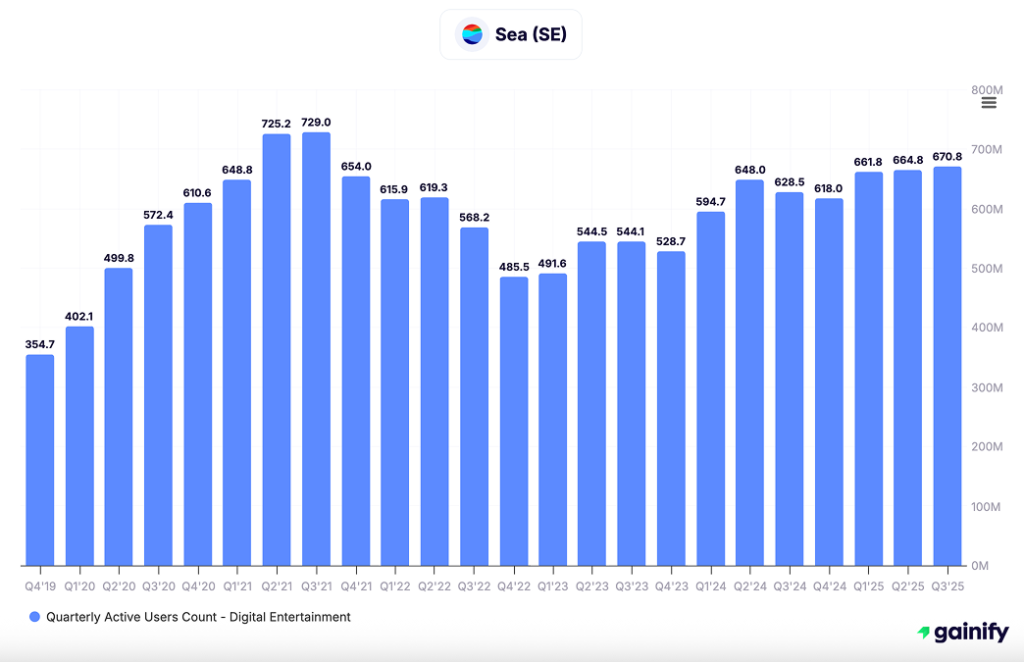

Sea’s digital entertainment segment continues to demonstrate strong operating momentum. In Q3 2025, digital entertainment bookings reached $841 million, while quarterly active users stood at 670.8 million, reflecting both scale and sustained engagement across key markets. The segment also generated $466 million in adjusted EBITDA, underscoring its role as a meaningful profitability driver within the group.

At a sector level, Sea offers leveraged exposure to gaming demand in faster-growing economies, where competitive intensity remains lower than in mature Western markets. The combination of high engagement, improving monetization, and strong profitability in digital entertainment provides internal funding for growth initiatives while reducing reliance on external capital.

Valuation reflects both growth potential and execution risk, but Sea’s ability to generate cash from digital entertainment meaningfully differentiates it from many emerging-market peers.

Key risks

- Revenue concentration risk within a limited number of flagship game franchises

- Regulatory and policy uncertainty across multiple emerging markets

- Volatility in user engagement, which can impact bookings and earnings

- Capital allocation risk as management balances growth across multiple business lines

6. Take-Two Interactive Software (NASDAQ: TTWO)

- Market capitalization: $47.32 billion

- Forward P/E: 57.45x

- Analyst target upside: 8.32%

- Forward 3-year revenue CAGR: 18.20%

- Forward free cash flow yield: 0.80%

Business overview

Take-Two is a leading global video game publisher with a portfolio of premium franchises spanning console, PC, and mobile platforms. The company’s model is anchored by a small number of high-value intellectual properties, supported by recurrent consumer spending through live services, digital add-ons, and in-game purchases.

From a top-down perspective, the premium gaming market remains cyclical and hit-driven, but Take-Two occupies a differentiated position due to the longevity and monetization depth of its core franchises. This structure results in periods of uneven earnings punctuated by major content-driven inflection points.

Investment thesis

The central driver of Take-Two’s investment case is its upcoming content pipeline, most notably Grand Theft Auto VI, which is scheduled for release in fiscal 2027. Historically, major GTA releases have reset Take-Two’s revenue and earnings base for multiple years, making the current period one of elevated anticipation rather than normalized profitability.

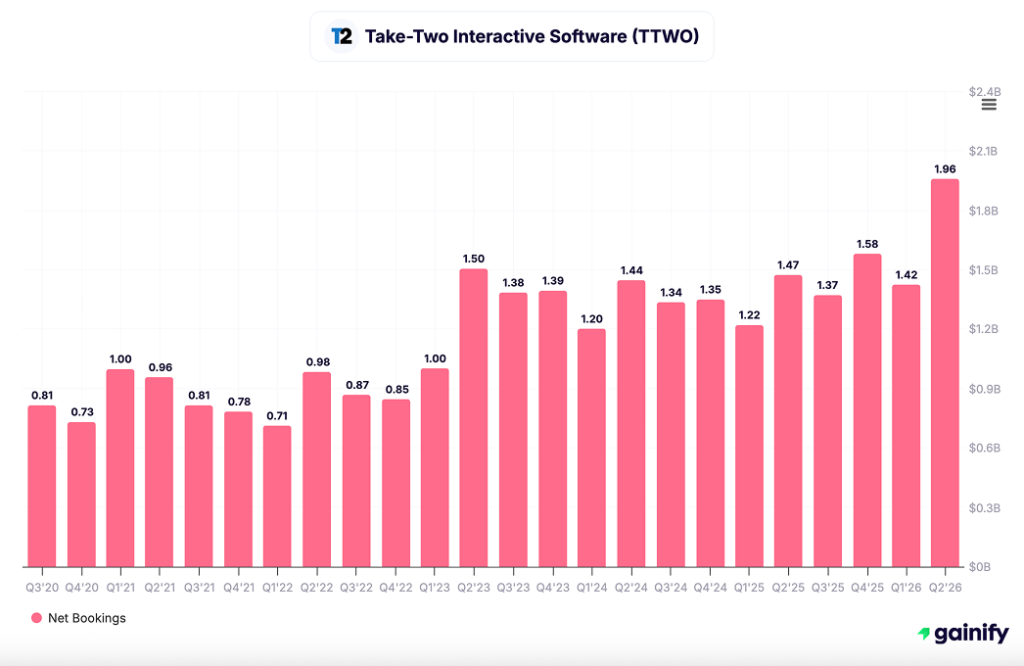

In Q2 FY26, Take-Two generated $1.96 billion in net bookings, significantly exceeding guidance, while recurrent consumer spending grew 20% year over year, highlighting the durability of its live-service revenue even ahead of its largest launch. Management also raised full-year guidance, projecting FY26 net bookings of $6.4 to $6.5 billion, reflecting confidence in the strength of its franchise portfolio and near-term release slate.

While valuation appears elevated on near-term earnings, the stock is best viewed through a cycle-adjusted lens, where earnings power expands materially following major franchise launches. GTA VI represents a potential step-change event rather than incremental growth.

Key risks

- Execution and timing risk surrounding Grand Theft Auto VI’s release

- Revenue concentration risk, given dependence on a small number of franchises

- Earnings volatility inherent in a hit-driven release model

- Rising development costs, which can pressure margins between launch cycles

Conclusion

As digital entertainment stocks move into 2026, the sector is no longer defined by unchecked expansion, but by execution, monetization efficiency, and cash flow durability. The reset that followed years of aggressive investment has sharpened differentiation across platforms, separating those that can convert scale and engagement into consistent financial returns from those still dependent on extended monetization assumptions.

The six companies discussed in this article illustrate that divergence clearly. Large-scale platforms such as Meta and Netflix are demonstrating operating leverage and improved capital discipline, while engagement-driven ecosystems like Roblox and Spotify are approaching inflection points where scale begins to translate into cash generation. Sea offers exposure to digital entertainment growth in emerging markets with stronger profitability than many peers, while Take-Two represents a cycle-driven opportunity tied to premium intellectual property and major content releases.

For investors, the opportunity lies in selective exposure rather than broad sector allocation. Blending cash-generative incumbents with a limited number of high-growth platforms can provide balanced participation in the next phase of digital entertainment, where returns are increasingly driven by monetization depth, capital efficiency, and the durability of underlying franchises rather than headline user growth alone.