Singapore remains one of Asia’s most stable and globally connected financial hubs. Its equity market, led by a mix of high-quality banks, infrastructure providers, and emerging technology platforms, offers a balance between income stability and moderate growth potential.

While the U.S. market, driven by the S&P 500, continues to outperform in aggregate, Singapore equities present selective opportunities for disciplined investors focused on valuation, cash flow resilience, or dividend yield.

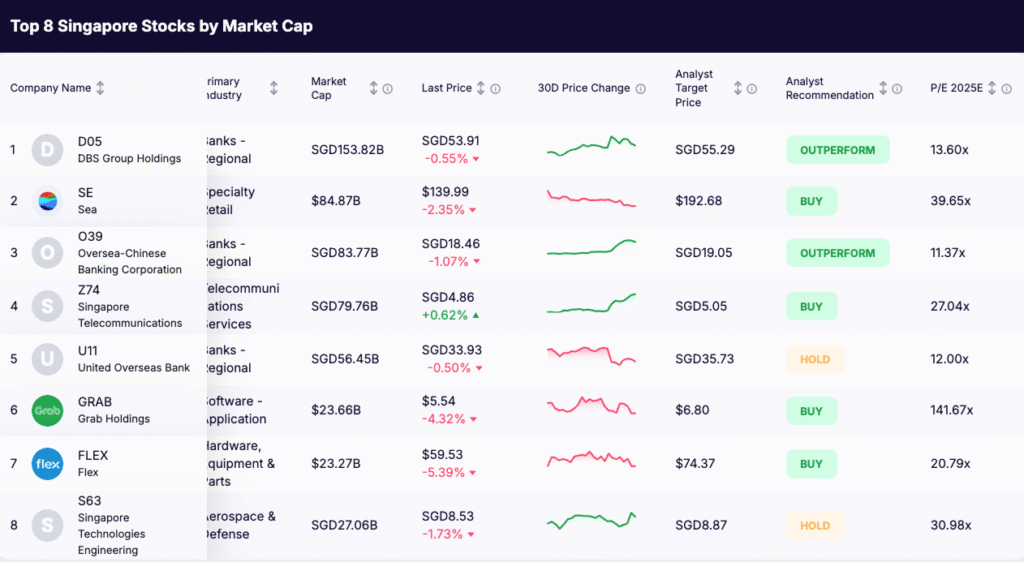

This analysis examines eight of the most prominent Singapore stocks by market capitalization, evaluating their strategic positioning, financial resilience, and risk-reward profiles as investors look ahead to 2026.

Market Overview: Singapore vs the S&P 500

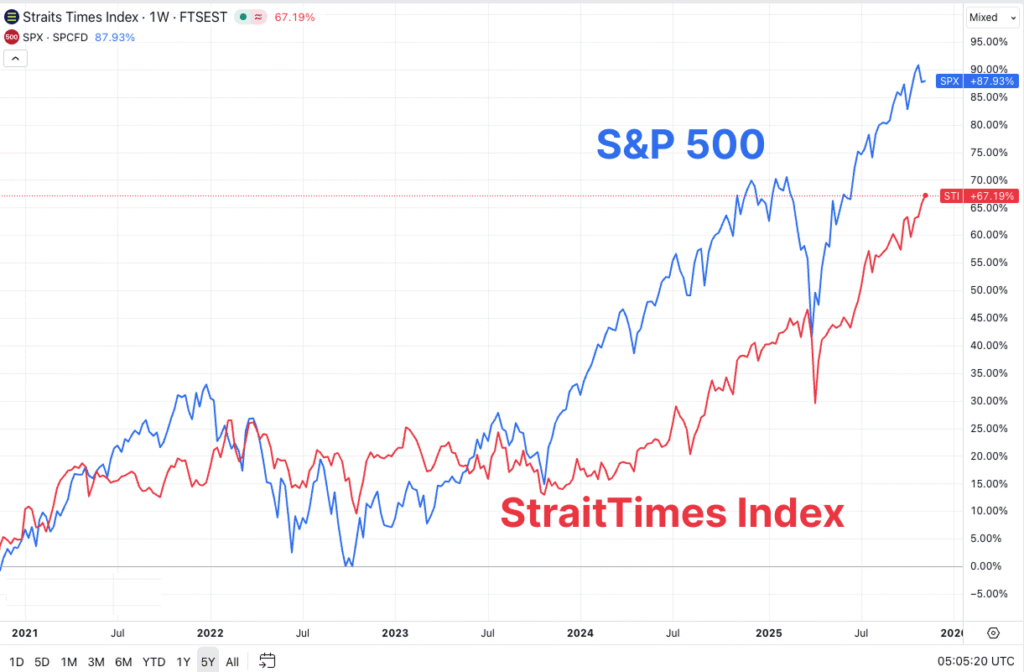

Over the past five years, Singapore stocks have returned 67 percent, compared with an 88 percent gain in the S&P 500. The Straits Times Index remains concentrated in financials, telecommunications, and industrials. These sectors provide resilience but offer limited participation in the high-growth areas that have powered U.S. market performance such as artificial intelligence, semiconductors, and software.

Singapore’s equity market continues to emphasize capital discipline, strong balance sheets, and dependable dividends. It serves as a stable proxy for Southeast Asian growth rather than a high-beta innovation trade.

Heading into 2026, investor focus will center on regional interest rates, credit and property-cycle conditions, and cross-border capital flows from China and the Middle East. These factors will drive liquidity, valuation trends, and sector leadership across Singapore stocks in the coming year.

To search stocks like that, just use the Gainify stock screener and filter by “Singapore” under Region.

1. DBS Group Holdings (D05)

Sector: Banking

Market Cap: SGD 153.8 billion

Last Price: SGD 53.91

Target Price: SGD 55.29

Analyst Consensus: Outperform

Implied Upside: 3%

DBS remains the dominant franchise in Singapore’s financial sector with diversified exposure across retail, corporate, and wealth management. Its digital transformation has enhanced operating efficiency and client retention, positioning it ahead of regional peers.

Investment Thesis:

The bank continues to generate superior return on equity above 16% while maintaining one of the strongest capital positions in Asia. Fee income momentum and disciplined cost management provide earnings stability even as loan growth moderates. Dividend yield near 5.5% offers defensive appeal.

Key Risks:

Earnings sensitivity to rate cuts in 2026, credit deterioration in Greater China, and slower trade activity across ASEAN.

Analyst View:

Research coverage within the Singapore banking sector maintains an Outperform stance, with analysts forecasting roughly 3% upside from current levels. DBS remains the preferred core holding among Singapore stocks for investors seeking liquidity, balance sheet quality, and consistent dividend returns.

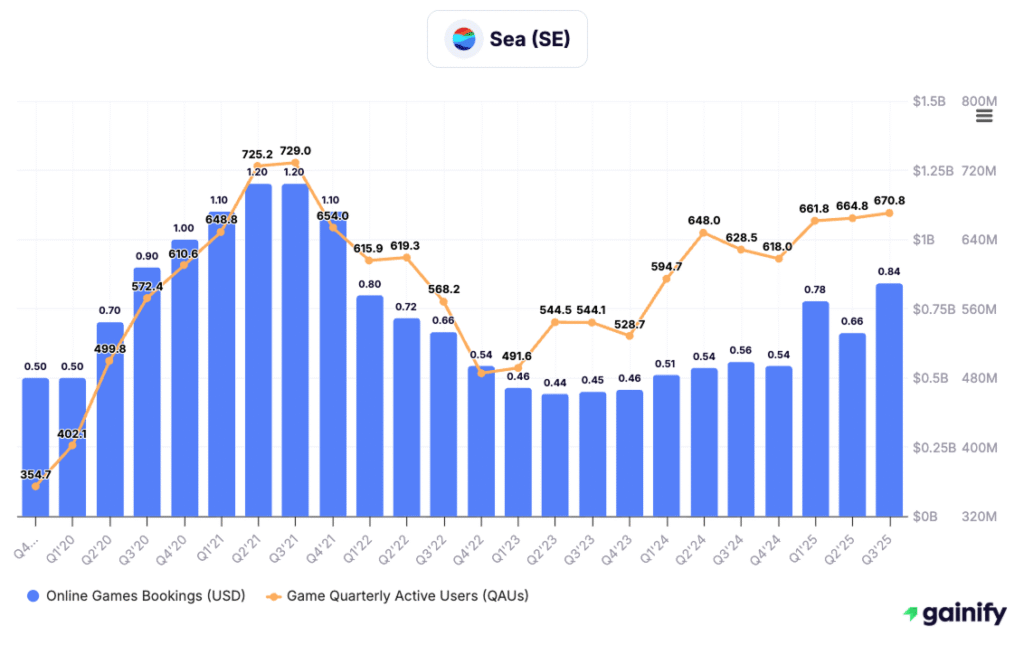

2. Sea Limited (SE)

Sector: Specialty Retail / Digital Services

Market Cap: USD 84.9 billion

Last Price: USD 139.99

Target Price: USD 192.68

Analyst Consensus: Buy

Implied Upside: 38%

Sea Limited is Singapore’s leading digital-economy platform with operations spanning e-commerce (Shopee), digital entertainment (Garena), and financial services (SeaMoney). The company has achieved scale leadership across multiple Southeast Asian markets and continues to expand its fintech footprint regionally.

Investment Thesis:

Shopee remains the dominant e-commerce player in Southeast Asia, while SeaMoney’s payments and lending businesses are gaining traction. Margin recovery has been supported by improved cost discipline and higher monetization rates. Continued growth in digital payments and credit adoption provides a medium-term re-rating catalyst.

Key Risks:

Execution risk in scaling financial services, heightened competition in regional e-commerce, and regulatory scrutiny in key markets such as Indonesia and Vietnam.

Analyst View:

Analysts maintain a Buy recommendation with an estimated 38 percent upside potential. Sea remains one of the most dynamic Singapore-linked growth stocks, combining exposure to e-commerce, gaming, and fintech in a single platform with improving profitability visibility.

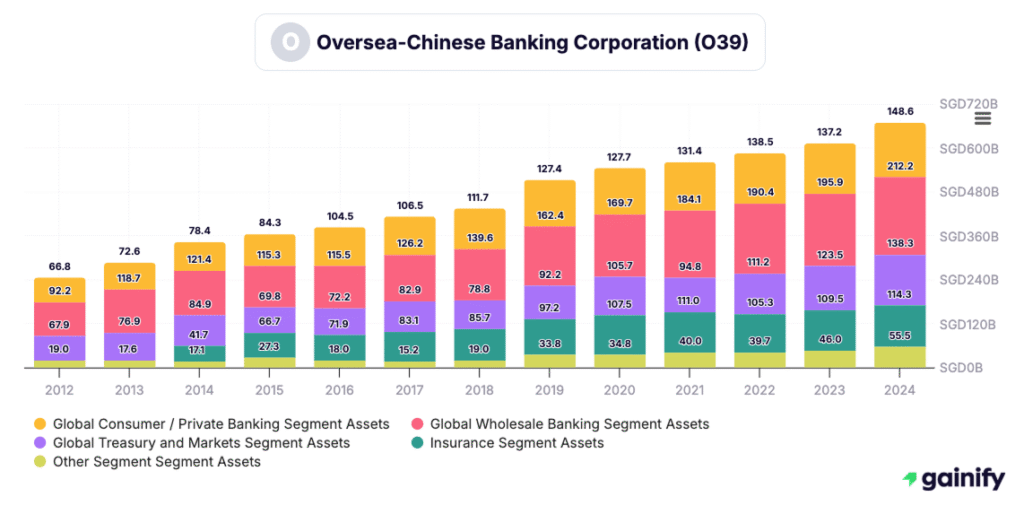

3. Oversea-Chinese Banking Corporation (O39)

Sector: Banking

Market Cap: SGD 83.8 billion

Last Price: SGD 18.46

Target Price: SGD 19.05

Analyst Consensus: Outperform

Implied Upside: 4%

OCBC is Singapore’s second-largest bank and one of the oldest financial institutions in Southeast Asia. The group operates an integrated model across banking, insurance, and wealth management, anchored by its ownership of Great Eastern Holdings and its strong presence in Malaysia, Indonesia, and China.

Investment Thesis:

OCBC offers a balanced mix of growth and income. Its diversified earnings base provides stability across market cycles, and capital levels remain robust with a Common Equity Tier 1 ratio above 14 percent. The bank’s wealth and insurance segments have become key profit contributors, helping offset margin compression from slower loan growth.

Key Risks:

Weakness in China’s property sector, lower investment income in its insurance arm, and limited near-term catalysts for earnings re-rating.

Analyst View:

Coverage across major institutions retains an Outperform stance with approximately 4% upside from current levels. Among Singapore stocks, OCBC remains a conservative, income-generating choice for investors seeking high dividend stability and measured exposure to regional banking growth.

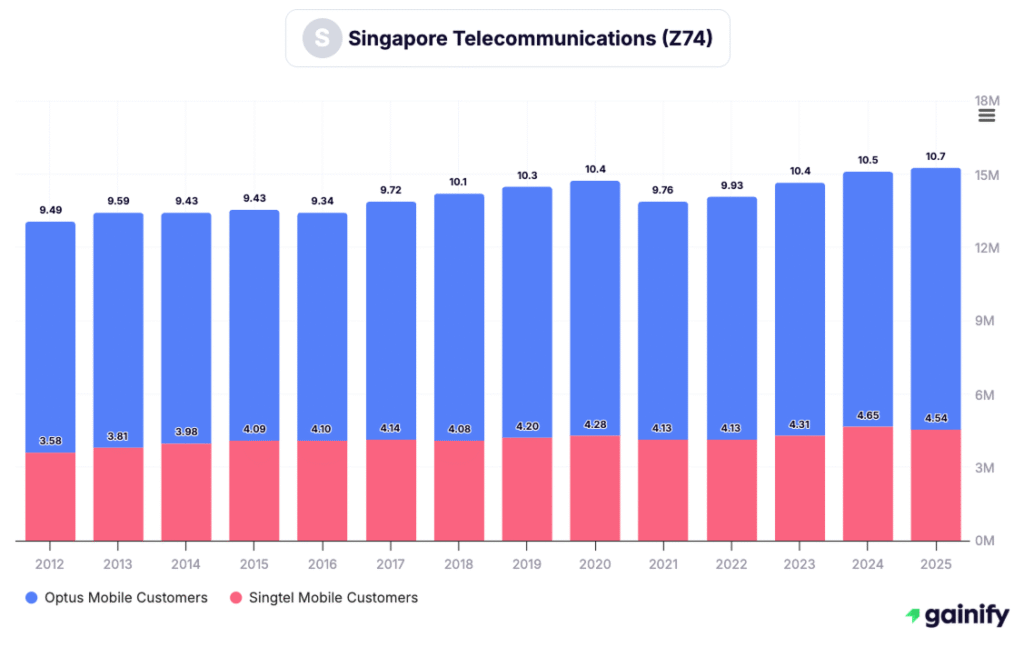

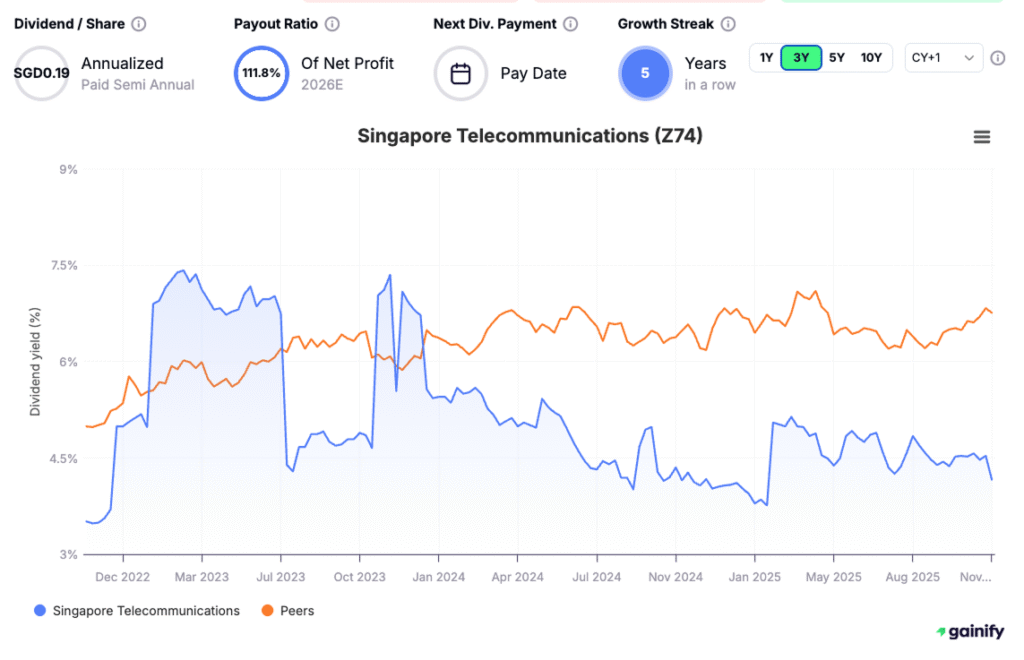

4. Singapore Telecommunications (Z74)

Sector: Telecommunications and Digital Infrastructure

Market Cap: SGD 79.8 billion

Last Price: SGD 4.86

Target Price: SGD 5.05

Analyst Consensus: Buy

Implied Upside: 4%

Singapore Telecommunications, or Singtel, is the largest telecom and digital-services provider in Southeast Asia. The group operates core connectivity and enterprise services in Singapore and Australia and holds strategic investments in regional associates such as Bharti Airtel in India and Telkomsel in Indonesia.

Investment Thesis:

Singtel is transitioning from a legacy telecom operator into a digital infrastructure and data-services leader. Its regional associates continue to deliver strong performance, while the domestic business benefits from stable cash flows and disciplined cost control. The expansion into data centers and cloud services supports a medium-term growth trajectory and valuation re-rating potential.

Key Risks:

Intensifying competition in regional telecom markets, execution challenges in digital ventures, and high capital expenditure requirements tied to 5G and data infrastructure.

Analyst View:

Analysts maintain a Buy recommendation with an expected 4 percent upside. Singtel remains a core component among Singapore stocks for investors seeking a blend of income stability, infrastructure exposure, and participation in Asia’s digital transformation.

5. United Overseas Bank (SGX: U11)

Sector: Banking

Market Cap: SGD 56.5 billion

Last Price: SGD 33.93

Target Price: SGD 35.73

Analyst Consensus: Hold

Implied Upside: 5%

United Overseas Bank is Singapore’s third-largest lender and one of the most conservatively managed banks in the region. Its operations span consumer banking, SME lending, and corporate finance across Singapore, Malaysia, Thailand, Indonesia, and China.

Investment Thesis:

UOB remains a high-quality defensive franchise within the ASEAN banking system. Its credit discipline and prudent risk management have produced one of the lowest non-performing loan ratios among regional peers. The bank’s investments in digital platforms, particularly UOB TMRW, have enhanced customer acquisition and operating efficiency. Dividend yield of around 4.0% continues to attract income-focused investors.

Key Risks:

Slower ASEAN loan growth, margin compression under a lower-rate environment, and limited near-term earnings catalysts relative to larger peers DBS and OCBC.

Analyst View:

Consensus maintains a Hold rating with an estimated 5 percent upside. UOB remains a dependable component within Singapore stocks, offering predictable income and balance sheet strength, but may underperform peers without a clear catalyst for growth re-rating.

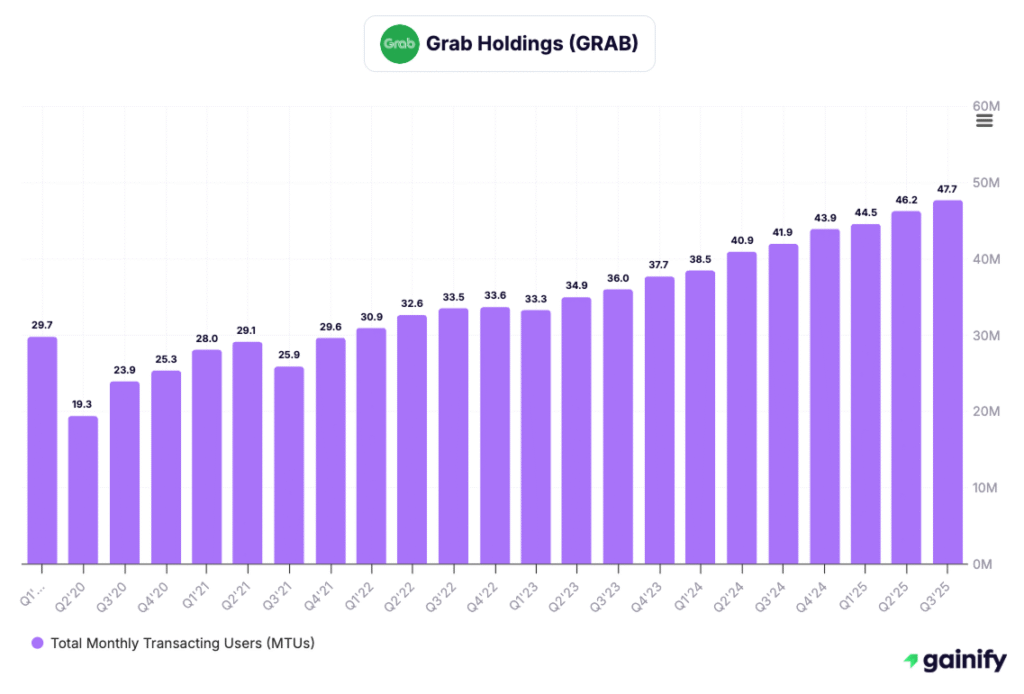

6. Grab Holdings (GRAB)

Sector: Mobility, Delivery, and Fintech

Market Cap: USD 24.2 billion

Last Price: USD 3.17

Target Price: USD 4.25

Analyst Consensus: Buy

Implied Upside: 34%

Grab is Southeast Asia’s leading super-app, providing mobility, food delivery, logistics, and financial services across eight countries. Its ecosystem integrates on-demand transport, merchant solutions, and digital payments through a unified consumer platform.

Investment Thesis:

Grab’s path to profitability continues to accelerate. Management has executed on cost discipline and improved unit economics in both mobility and delivery segments. Gross merchandise value and adjusted EBITDA have shown double-digit growth, reflecting better demand recovery post-reopening. The expansion of GrabFin into lending and insurance offers new monetization opportunities.

Key Risks:

Sustained competition in food delivery and ride-hailing, regulatory pressures on gig labor, and the pace of fintech adoption in emerging Southeast Asian markets.

Analyst View:

Analysts maintain a Buy rating with an estimated 34% upside. Among Singapore stocks with regional reach, Grab stands out as a scalable digital platform transitioning from growth-at-all-costs to sustainable profitability. Its diversified ecosystem positions it as a long-term beneficiary of Southeast Asia’s digital consumption trend.

7. Flex Ltd (FLEX)

Sector: Electronics Manufacturing Services (EMS)

Market Cap: USD 23.4 billion

Last Price: USD 34.33

Target Price: USD 35.09

Analyst Consensus: Hold

Implied Upside: 2%

Flex Ltd is a global leader in electronics manufacturing and supply-chain solutions. The company designs and builds products across technology, automotive, healthcare, and industrial markets. Headquartered in Singapore with major operations in the United States, Flex plays a pivotal role in global production networks and near-shoring initiatives.

Investment Thesis:

Flex continues to benefit from structural shifts in global manufacturing, including diversification away from China and increasing demand for design-led, high-value manufacturing solutions. The company’s focus on automation and supply-chain optimization supports steady margin expansion and free-cash-flow generation. Its balance sheet remains conservative, providing flexibility for strategic acquisitions or shareholder returns.

Key Risks:

Exposure to global macro cycles, volatility in electronics demand, and pricing pressure from large OEM customers.

Analyst View:

Analysts maintain a Hold rating with an implied 2% upside. Among Singapore-linked industrials, Flex offers investors stable exposure to global manufacturing trends with limited short-term catalysts. Its execution discipline and operational leverage support a neutral but resilient outlook within Singapore stocks.

8. ST Engineering (S63)

Sector: Aerospace, Defence, and Smart Infrastructure

Market Cap: SGD 27.8 billion

Last Price: SGD 8.93

Target Price: SGD 9.79

Analyst Consensus: Buy

Implied Upside: 10%

ST Engineering is Singapore’s flagship engineering and defence conglomerate with global operations across aerospace, electronics, land systems, and marine divisions. Its diversified revenue base spans government, commercial, and smart-city infrastructure clients in more than 100 countries.

Investment Thesis:

The company enters 2026 with record order backlog exceeding SGD 27 billion, providing earnings visibility through 2027. Growth in the aerospace and defence segments, combined with expanding smart mobility and infrastructure solutions, supports consistent revenue momentum. Margin recovery is expected as supply-chain pressures ease and operational efficiency improves. Dividend yield of approximately 4% adds income stability to the investment case.

Key Risks:

Execution challenges in large-scale defence projects, potential budget constraints in government spending, and currency exposure from global contracts.

Analyst View:

Consensus maintains a Buy rating with an implied 10% upside. ST Engineering remains a core industrial holding within Singapore stocks, offering predictable earnings, strong cash generation, and moderate growth supported by long-term government and commercial contracts.

Strategic Insights

- Sector Concentration: Banking accounts for over 40 percent of Singapore’s market capitalization. Investors should balance exposure with telecoms, industrials, and emerging tech for diversification.

- Dividend Advantage: The average dividend yield among Singapore blue chips exceeds 4 percent, significantly higher than the S&P 500’s forward yield near 2.0 percent.

- Regional Opportunity: With ASEAN GDP growth projected above 4 percent for 2026, Singapore companies positioned in banking, logistics, and digital services may benefit from rising consumption and trade integration.

- Valuation Landscape: Singapore equities trade at approximately 12–13 times forward earnings compared with the S&P 500’s 25 times, providing potential for re-rating if earnings momentum continues.

Key Risks

- Macroeconomic Sensitivity: Slower global trade or a China downturn could reduce regional loan demand and consumer spending.

- Interest-Rate Reversal: Lower rates could pressure bank profitability and dividend sustainability.

- Sector Disruption: Telecoms and manufacturing sectors face ongoing disruption from technology shifts.

- Currency Volatility: A weaker regional currency environment could affect USD-translated earnings for multinational investors.

Conclusion

Singapore’s equity market offers investors a differentiated opportunity set built on resilient financial institutions, established industrials, and selectively emerging technology leaders. For 2026, positioning across the banking sector for income stability and selective exposure to digital-economy names such as Sea and Grab provides a balanced framework.

While total returns may continue to lag U.S. benchmarks, Singapore’s combination of strong governance, attractive valuations, and growing regional integration ensures it remains a core allocation for investors seeking diversification and dependable cash flow in Asia.