Water is no longer just a basic necessity. It is becoming one of the most investable themes of the decade. From drought resilience to industrial efficiency and smart infrastructure, the global race to secure clean water is creating a powerful long-term investment story.

In 2025, capital has been steadily flowing toward companies that combine regulated stability with technology-driven growth, including utilities, equipment manufacturers, and innovators that keep the world’s water systems running. Investors now view water as both a defensive anchor and a sustainability growth opportunity.

As of November 5, 2025, the iShares Global Water UCITS ETF is up 10.8% year to date, compared with a 15.4% gain for the S&P 500. Water stocks have lagged broad equities but continue to outperform traditional utilities, offering lower volatility and stronger earnings visibility.

With the sector’s momentum building and governments increasing infrastructure investment, here are the top eight water stocks to consider for 2026, representing the companies best positioned to turn the world’s most vital resource into sustainable long-term growth.

Key highlights for investors

- Demand drivers remain strong, supported by global infrastructure renewal, tighter environmental regulation, drought mitigation efforts, and industrial efficiency initiatives.

- Regulated water utilities continue to deliver stable earnings and steady dividend growth. Although higher interest rates have constrained free cash flow, upcoming tariff adjustments are expected to provide partial relief.

- Water technology and quality-testing companies are driving the sector’s expansion, benefiting from recurring service revenue, strong pricing power, and multi-year adoption of digital monitoring and water-reuse systems.

- Valuations across the sector are diverse, giving investors an opportunity to build a balanced mix of income-generating utilities and high-growth technology leaders within the broader water theme.

Top 8 Water Stocks to Consider in 2026

The global water industry is entering a new investment cycle. Years of underinvestment are giving way to large-scale infrastructure upgrades, digital modernization, and private-sector partnerships. The result is a market that now combines the dependable income of regulated utilities with the higher-margin potential of advanced water technology.

Across every segment, from purification systems and treatment facilities to smart sensors and analytics, companies are working to improve efficiency, reduce waste, and meet increasingly strict environmental standards. Investors are beginning to separate steady, dividend-focused names from innovators that are positioned for faster structural growth, creating opportunity across the entire sector.

With this backdrop, the following are the top eight water stocks to consider in 2026, each representing a different part of the global water investment landscape, from essential utilities to technology leaders shaping the future of clean water.

To screen stocks like that, you can use the Gainify stock screener. In the Industry filter, select Water Utilities or any other option from the 1000+ available filters.

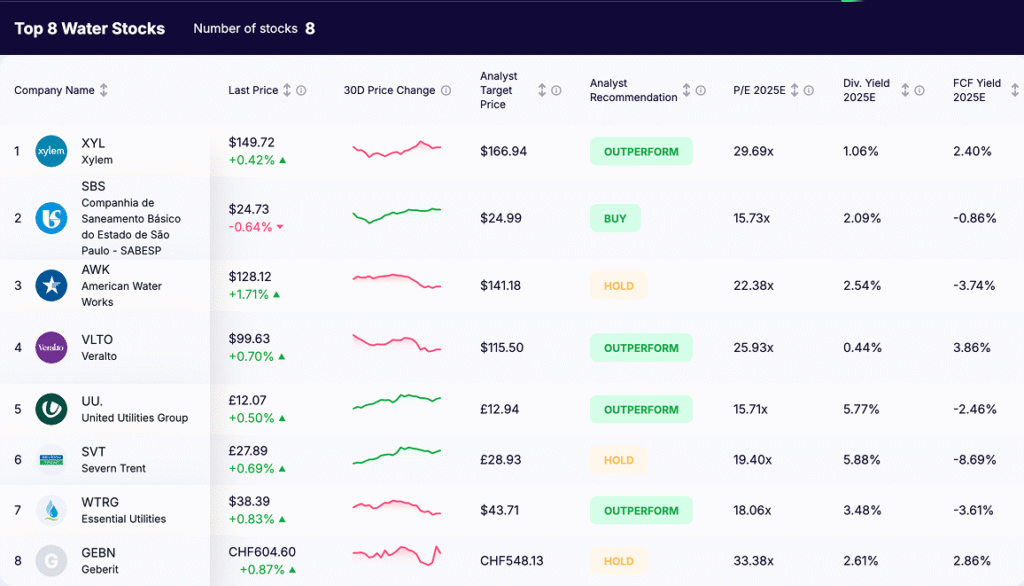

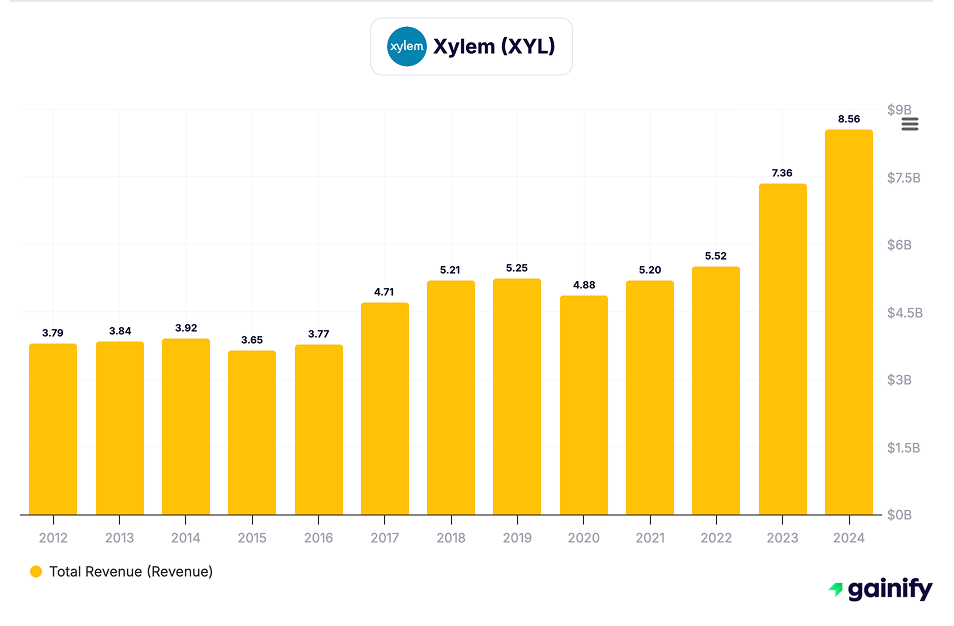

1) Xylem (NYSE: XYL)

Price: $149.72

P/E: 29.69x

Dividend yield: 1.06%

FCF yield: 2.40%

Target price: $166.94

Analyst view: Outperform

What it does:

Xylem is the leading global provider of water infrastructure and digital monitoring systems. The company designs and manufactures advanced pumps, sensors, treatment solutions, and software for municipalities and industrial customers worldwide. Its acquisition of Evoqua Water Technologies in 2023 expanded its capabilities in wastewater and reuse, creating the most comprehensive portfolio in the sector.

Investment thesis:

Xylem combines scale with a technology edge. Its integrated hardware and analytics platform positions it to benefit from the global shift toward smart water networks and industrial recycling. Rising demand for digital monitoring, leak detection, and predictive maintenance supports recurring revenue growth. The Evoqua integration is driving cost savings, while a growing share of high-margin software and services is supporting mid-teens annual EPS growth.

Latest developments:

In Q3 2025, organic revenue increased 7.0% year over year, and EBITDA margin improved 200 basis points to 23.2%, supported by pricing gains and procurement efficiencies. Industrial order intake declined by 2%, partially do slower municipal project timing. Management raised its full-year outlook for EPS to $5.03 – $5.08.

Catalyst watch:

Monitor upcoming U.S. and EU infrastructure funding rounds focused on leakage reduction, digital twins, and water reuse initiatives, which could accelerate project pipelines.

Key risks:

Potential delays in public infrastructure spending or slower Evoqua integration could weigh on earnings. The current valuation already prices in above-trend growth, leaving limited room for missteps.

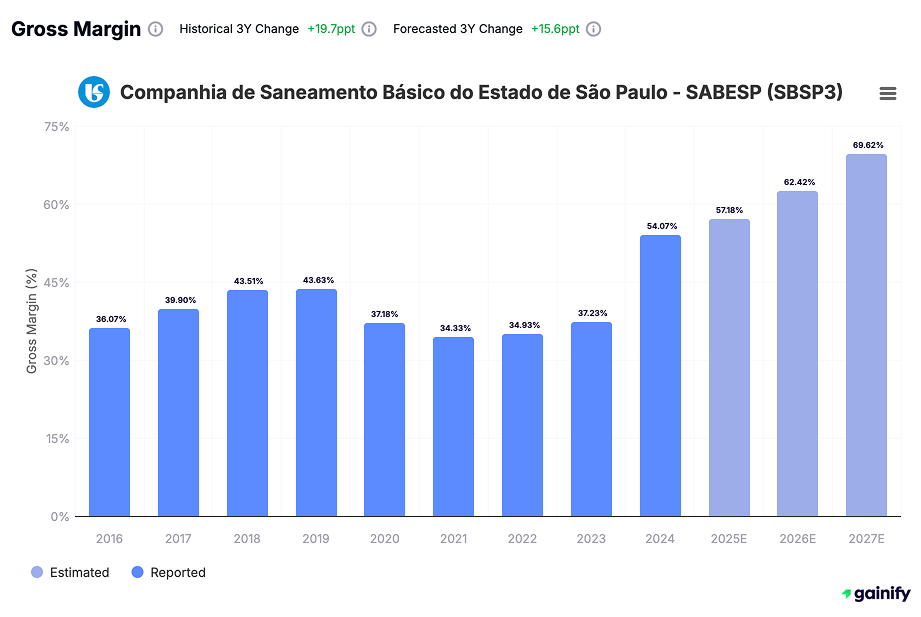

2) SABESP – Companhia de Saneamento Básico do Estado de São Paulo (NYSE:SBS)

Price: $24.73

P/E: 15.73x

Dividend yield: 2.09%

FCF yield: −0.86%

Target price: $24.99

Analyst view: Buy

What it does:

SABESP is Brazil’s largest water and sewage utility, serving about 28 million residents with water and 25 million with wastewater services in São Paulo state. The company manages supply, treatment, and distribution across more than 370 municipalities.

Investment thesis:

SABESP benefits from structural demand for sanitation and urban infrastructure in Brazil. Tariff mechanisms and ongoing modernization support steady revenue growth. The company’s multi-year investment plan focuses on efficiency, non-revenue water reduction, and service expansion. Despite temporary free cash flow pressure from elevated capital spending, the stock trades at a discount to peers due to country risk, offering long-term upside potential.

Latest developments:

In Q2 2025, net income rose 77% year over year to about R$2.1 billion and EBITDA margin reached 64%. Capital spending increased to R$3.6 billion as major network upgrades continued. Management announced a R$203 million provision related to the FAUSP social tariff fund that will affect Q3 results.

Catalyst watch:

Privatization progress, tariff adjustments, and results from water loss reduction programs. Stable currency and inflation trends remain important for valuation.

Key risks:

Regulatory or political delays, execution risk from heavy capital spending, and FX volatility. Weather conditions affecting reservoirs can also influence operating performance.

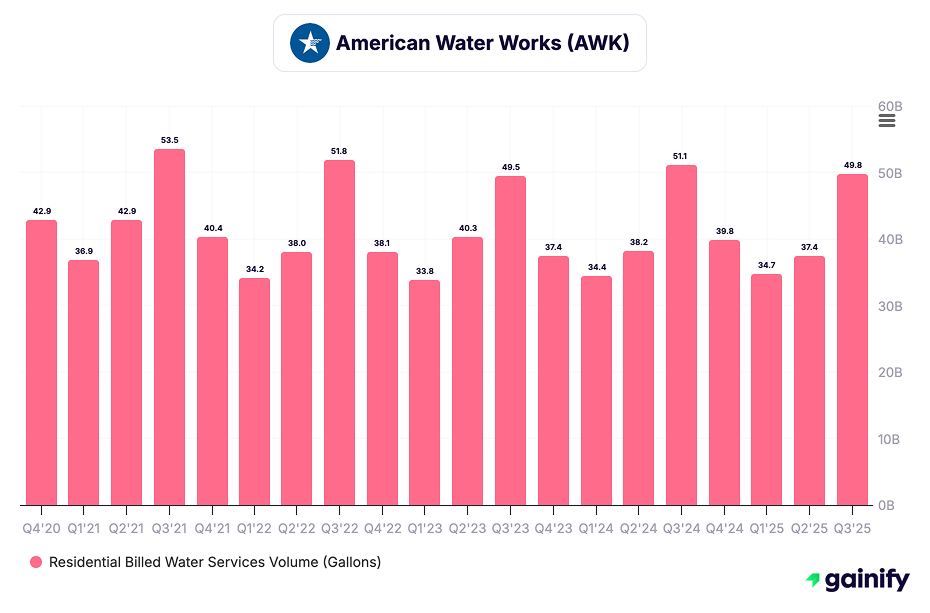

3) American Water Works (NYSE:AWK)

Price: $128.12

P/E: 22.4x

Dividend Yield: 2.5%

Free Cash Flow Yield: −3.7%

Target Price: $141.18

Analyst View: Hold

What it does:

American Water Works is the largest publicly traded water and wastewater utility in the United States, operating regulated systems across 46 states. The company provides essential water services to residential, commercial, and municipal customers under long-term rate frameworks that ensure predictable returns and cash flows.

Investment thesis:

AWK remains a cornerstone holding for investors seeking stable income and consistent dividend growth. The company’s strategy centers on regulated rate base expansion, disciplined system acquisitions, and operational efficiency. Its predictable cash flows and constructive regulatory environment support mid-single-digit earnings and dividend growth, making it one of the most defensive names in the utilities sector.

Latest developments:

In Q3 2025, AWK reported 8.2% year-over-year EPS growth on revenue of $1.34 billion, driven by new rate implementations and lower operating costs. The company secured favorable rate outcomes in multiple jurisdictions and maintained its full-year guidance for 7–9% EPS growth. Capital expenditure for 2025 is projected at $2.7 billion, primarily directed toward pipe renewal, treatment upgrades, and water quality compliance.

Catalyst watch:

Key catalysts include upcoming state-level rate case decisions, the pipeline of small municipal system acquisitions, and potential cost normalization as supply chain pressures ease.

Key risks:

Earnings could be affected by higher interest costs, adverse weather patterns, or regulatory delays in rate recovery. The company’s heavy capital spending program also keeps free cash flow negative in the near term.

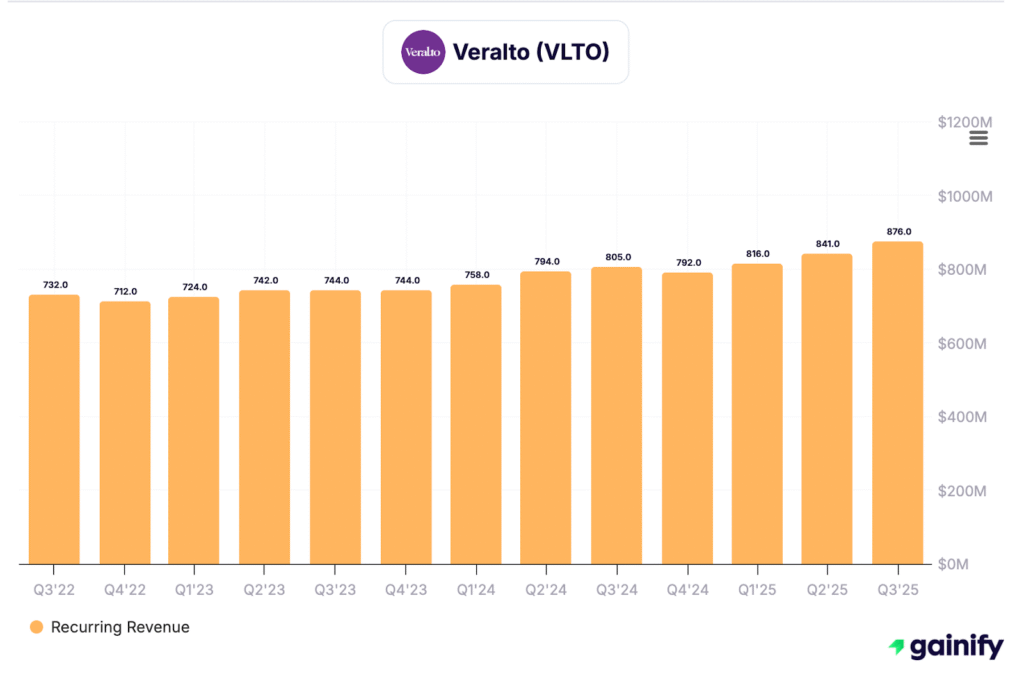

4) Veralto (NYSE:VLTO)

Price: $99.63

P/E: 25.9x

Dividend Yield: 0.4%

Free Cash Flow Yield: 3.9%

Target Price: $115.50

Analyst View: Outperform

What it does:

Veralto Corporation designs and produces water-quality testing, filtration, and analytical instruments used by laboratories, municipalities, and industrial clients to monitor water safety and compliance. Spun off from Danaher in 2023, Veralto operates through two main segments – Water Quality and Product Identification – with a strong focus on recurring consumables and aftermarket services that generate more than half of total revenue.

Investment thesis:

Veralto represents a rare combination of industrial reliability and secular growth. The company benefits from global investment in water safety, laboratory automation, and regulatory compliance. Its installed base drives recurring consumables demand, while new product innovation supports organic growth and operating leverage. With free cash flow consistently above 100% of net income, Veralto remains a high-quality compounder in the water technology space.

Latest developments:

In Q3 2025, Veralto reported revenue of $1.40 billion, up 6.9% year over year, with core sales growth of 5.1%. Adjusted EPS came in at $0.99, representing 11% annual growth, supported by strong consumables demand and cost discipline. Free cash flow reached $258 million, up from $215 million a year earlier, driven by improved working capital efficiency. Management reaffirmed full-year guidance and highlighted resilient demand across both operating segments.

Catalyst watch:

Investors should monitor the rollout of Veralto’s next-generation online water monitoring platform, continued cross-selling across its installed base, and disciplined acquisition activity that could expand its presence in analytical testing and filtration.

Key risks:

Exposure to industrial capital spending cycles could temper growth in softer macro conditions. Foreign-exchange volatility remains a modest earnings headwind given Veralto’s diversified global footprint.

5) United Utilities Group (LSE:UU.)

Price: £12.07

P/E: 15.7x

Dividend Yield: 5.8%

Free Cash Flow Yield: –2.5%

Target Price: £12.94

Analyst View: Outperform

What it does:

United Utilities operates regulated water and wastewater networks across North West England, serving millions of households and businesses. The company manages extensive infrastructure assets, including treatment plants, reservoirs, and thousands of kilometres of pipelines.

Investment thesis:

United Utilities provides a stable, inflation-linked income stream under the UK’s regulated framework. The business combines defensive cash flows with long-term asset growth through its AMP8 capital investment plan, which focuses on environmental upgrades, network resilience, and infrastructure renewal. The company’s strong balance sheet and predictable regulatory structure make it a cornerstone holding for income-focused investors.

Latest developments:

In the first half of fiscal year 2025/26, United Utilities reported 6.5% revenue growth and a steady improvement in operating profit, supported by tariff increases and lower energy costs. Management reaffirmed its inflation-linked dividend policy and confirmed that the £3 billion AMP8 programme, which includes the Haweswater aqueduct upgrade and storm overflow reduction projects, remains on track and fully funded.

Catalyst watch:

Upcoming Ofwat determinations on allowed returns and cost-of-capital assumptions will influence profitability. The company’s environmental performance scores and progress against regulatory leakage targets will also be key factors for investor sentiment.

Key risks:

Regulatory penalties related to service quality or environmental compliance could pressure returns. Political scrutiny over customer bills remains high, and extreme weather events pose ongoing operational risks to network performance.

6) Severn Trent (LSE:SVT)

Price: £27.89

P/E: 19.4x

Dividend Yield: 5.9%

Free Cash Flow Yield: –8.7%

Target Price: £28.93

Analyst View: Hold

What it does:

Severn Trent provides regulated water and wastewater services to around eight million people across the Midlands and Wales. The company operates under the UK’s regulatory framework and manages extensive infrastructure assets focused on network reliability, water quality, and environmental compliance.

Investment thesis:

Severn Trent offers investors reliable income and predictable earnings backed by regulated cash flows. The company is a key participant in the UK’s AMP8 investment cycle, which targets major upgrades in infrastructure, resilience, and environmental performance. Strong operational delivery and cost efficiency support the sustainability of its inflation-linked dividend, making it one of the most attractive yield plays in the UK utilities sector.

Latest developments:

For the year ended 31 March 2025, Severn Trent delivered revenue of £2,426.7 million, a 3.8 % increase year-over-year. The company’s five-year AMP8 investment programme is outlined at approximately £12.9 billion to £15 billion for the 2025-30 period. Management reaffirmed its inflation-linked dividend policy and confirmed the investment plan remains on track and fully funded.

Catalyst watch:

Upcoming Ofwat determinations on allowed returns, performance incentives tied to leakage and service metrics, and delivery milestones within the AMP8 plan will shape near-term investor sentiment.

Key risks:

High capital expenditure requirements continue to weigh on free cash flow. Regulatory scrutiny and political pressure around environmental performance and customer bills remain potential headwinds.

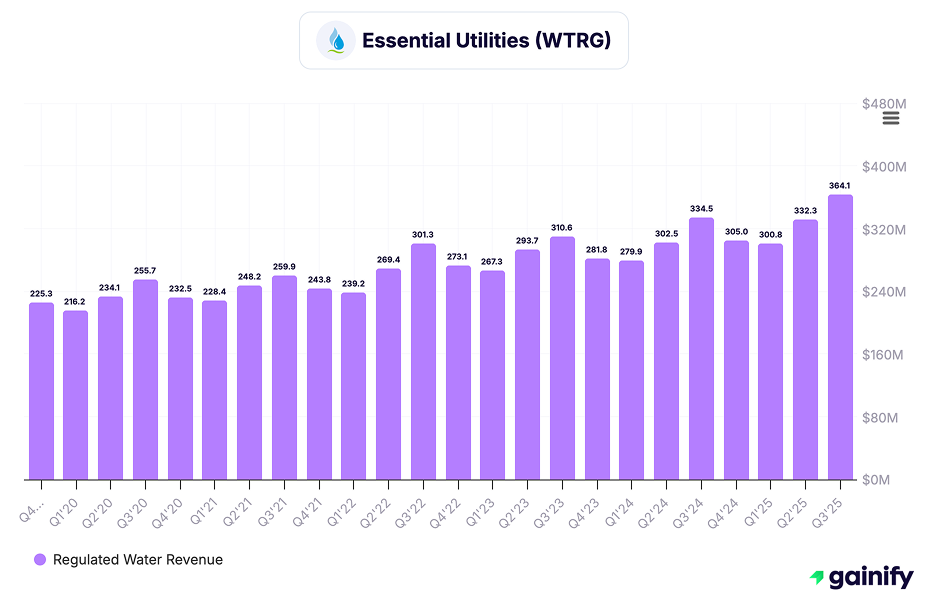

7) Essential Utilities (NYSE:WTRG)

Price: ~$38.39

P/E: ~18× (2025E)

Dividend Yield: ~3.5%

Free Cash Flow Yield: –3.6%

Analyst View: Outperform

What it does:

Essential Utilities provides regulated water, wastewater, and natural gas services across several U.S. states through its Aqua and Peoples brands. The company focuses on system acquisitions, infrastructure modernization, and rate-based asset growth to deliver stable, long-term earnings.

Investment thesis:

Essential combines the stability of a regulated utility with steady expansion through acquisitions and infrastructure investment. Consistent rate base growth, strong balance sheet management, and a track record of dividend increases support its position as a dependable income and growth holding.

Latest developments:

In Q3 2025, Essential Utilities reported revenue of $477 million, up 9.6% year over year, and EPS of $0.33, up 32% from the prior year. Year-to-date infrastructure investment reached $983 million, and management reaffirmed full-year spending of around $1.5 billion focused on pipe replacement, water quality, and system integration.

Catalyst watch: Key catalysts include rate case approvals, execution of new infrastructure projects, and continued acquisition activity in small municipal systems.

Key risks:

Potential regulatory delays, higher financing costs, or slower acquisition integration could pressure short-term results.

8) Geberit (SWX:GEBN)

Price: CHF 604.60

P/E: 33.38x

Dividend yield: 2.61%

FCF yield: 2.86%

Target price: CHF 548.13

Analyst view: Hold.

What it does:

Geberit is a European leader in sanitary systems, providing flush plates, piping, water-efficient fixtures, and other installation technology. The company combines strong brand recognition, extensive distribution in residential and commercial construction markets, and increasing focus on renovation and water-efficiency retrofit demand.

Investment thesis:

Geberit offers investors premium exposure to the structural shift toward water efficiency in building infrastructure. The business benefits from high pricing power, healthy margins, and diversified end-markets. Its reliance on renovation rather than new-build housing provides resilience in sluggish construction cycles and supports stable revenue streams even in weaker markets.

Latest developments:

In Q3 2025, Geberit reported net sales of CHF 783 million, up 2.7% in Swiss francs and 5.4% in constant currency, despite currency headwinds. Adjusted earnings increased 6.4% year over year, and free cash flow rose to CHF 215 million, representing strong conversion from profits. Management upgraded full-year guidance to ~4.5% sales growth in local currencies and expects an EBITDA margin of around 29%.

Catalyst watch:

Key catalysts include the rollout of new DuoFix installation systems, expansion of water-saving product lines, and incentive-driven growth in renovation markets across Europe and the Middle East.

Key risks:

Geberit remains exposed to cyclical weakness in European construction markets, foreign-exchange volatility (especially Swiss-franc strength), and a relatively high valuation that pressures margin for error if growth slows.

Key risks: European construction cycle, currency moves versus the Swiss franc, elevated multiple.

What drives water stock performance in 2026

Regulated rate growth

Water utilities benefit from transparent regulatory frameworks that allow returns indexed to inflation and linked to asset-base expansion. Tariff adjustments and new customer connections drive steady rate base growth and predictable cash flows.

Infrastructure renewal cycle

Aging networks and stricter environmental standards are fueling multi-year capital expenditure programs across developed markets. Investment in pipe replacement, wastewater treatment, and leakage reduction is now a structural driver rather than a cyclical one.

Technology adoption

Advanced sensors, data analytics, and filtration technologies are transforming the economics of water management. Companies that offer integrated digital systems enjoy higher margins, recurring revenue from service contracts, and growing global demand for efficiency and compliance solutions.

Funding costs and capital discipline

Elevated interest rates continue to pressure free cash flow across regulated utilities. Firms with robust balance sheets and favorable regulatory treatment of financing costs are best positioned to sustain dividends and capital programs without diluting returns.

Weather and climate impact

Increasing climate volatility, including droughts, floods, and extreme rainfall, is driving urgency for infrastructure resilience. While such events can raise near-term operating costs, they also reinforce long-term investment in system upgrades and adaptive capacity.

Policy and sustainability momentum

National and regional initiatives targeting water security, wastewater reuse, and pollution control are accelerating project pipelines. Government incentives and ESG-focused capital allocation continue to draw investment into both traditional utilities and technology innovators.

Portfolio construction ideas

- Income core. AWK, UU., SVT, and WTRG for dividend growth and defensive earnings.

- Growth sleeve. XYL and VLTO for digital water, testing, and reuse.

- Emerging-market optionality. SBS for tariff reform and network expansion.

- Quality in building systems. GEBN for European renovation and premium pricing.

Water remains a structural, long-duration investment theme that combines yield, growth, and sustainability. While sector returns may trail high-beta benchmarks during strong equity rallies, water stocks have a proven record of compounding steadily across cycles. A portfolio that blends regulated utilities for stability with water technology leaders for innovation offers a balanced, forward-looking exposure to one of the world’s most essential resources.

All figures reflect data shown on the screen as of November 5, 2025. This content is for information only and is not investment advice.