Davis Selected Advisers, guided by portfolio manager Chris Davis, is one of the most enduring names in American asset management. The firm is known for its value investor heritage, disciplined investment strategy, and a commitment to long-term results over short-term speculation.

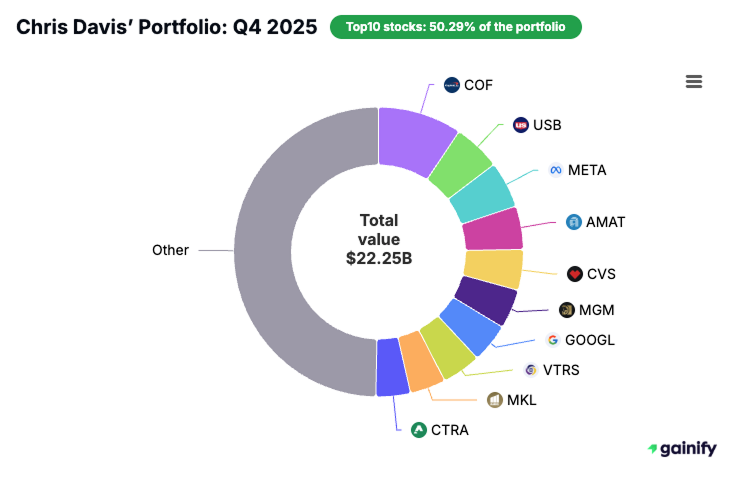

The latest 13F filing for Q4 2025 reveals a portfolio value of $22.25 billion, spread across 108 stock picks in a diversified equity portfolio. The average holding period remains at 32 quarters (eight years), which is exceptionally long by modern standards, especially when compared to many hedge funds and active managers who turn over portfolios several times a year. The low turnover rate is not a sign of inaction, but of conviction: Davis buys with the intention to own for years.

In this article, we will take a detailed look at Chris Davis’ Q4 2025 portfolio. You’ll see how his investment strategy works in practice, which companies make up his largest holdings, and the most significant changes he made this quarter. We will explain the top adds (increasing positions he already owned), new buys (brand-new positions), sold outs (completely exited holdings), and reductions (partial trims of existing positions). Along the way, we’ll discuss what each move reveals about his outlook and priorities. Finally, we’ll explore why the current portfolio fits the long-standing Davis Advisors playbook and highlight the key lessons individual investors can take from it.

Who Is Chris Davis

Chris Davis represents the third generation of one of America’s most respected investing families. He began his career at Davis Advisors in 1989, rising to become a portfolio manager in the mid-1990s, and now serves as chairman of the firm. His connection to investing is more than professional. It is personal and deeply rooted in family history. His grandfather, Shelby Cullom Davis, famously turned a modest investment into hundreds of millions of dollars by applying a disciplined, long-term focus to insurance stocks.

Today, Chris Davis oversees multiple strategies at Davis Advisors, including flagship products like the Davis New York Venture Fund, which has maintained the same core investment discipline since it launched in 1969. The firm’s culture values independent research, blends a quantitative approach with deep fundamental analysis.

The approach mirrors the principles of legendary investors Warren Buffett and Charlie Munger: focus on businesses you fully understand, buy their shares when the price offers good value, and hold them long enough for the company’s profits to grow. Over time, this allows earnings per share (EPS) growth, strong return on invested capital, and the power of compounding to steadily build wealth.

This philosophy has built a strong performance history over decades. It has also drawn attention from industry observers and authors such as Morgan Housel, who highlight Davis’ emphasis on patience, discipline, and the ability to make decisions without being swayed by short-term market emotions.

Investment Philosophy in Plain Language

Chris Davis focuses on owning businesses, not simply trading their stocks. This means looking well beyond the daily share price to understand how a company earns revenue, how it allocates that money, and how it plans to grow in the years ahead.

His team studies a range of key measures, including:

- P/E ratio and forward P/E to see how expensive or inexpensive a company’s earnings are compared to its share price.

- Price-to-book ratio (P/B), especially for asset-heavy businesses like banks and insurers, to compare market value with the value of assets on the balance sheet.

- Return on invested capital (ROIC) to judge how effectively management is using the company’s resources to create profits.

Davis Advisors also considers broader sector and industry trends along with economic factors like inflation and interest rates. For instance, financial services companies often see higher profits when interest rates rise, while consumer defensive companies such as Tyson Foods Inc can provide stability during periods of high inflation.

A defining feature of Davis’ strategy is maintaining a high active share, meaning the portfolio is built to look very different from benchmarks like the S&P 500 or the Russell 1000 Value Index. This is not an index-hugging strategy. Instead, it is a carefully selected, high-conviction collection of companies designed to perform well over a long-term bull market and remain resilient during downturns.

Portfolio Structure in Q4 2025

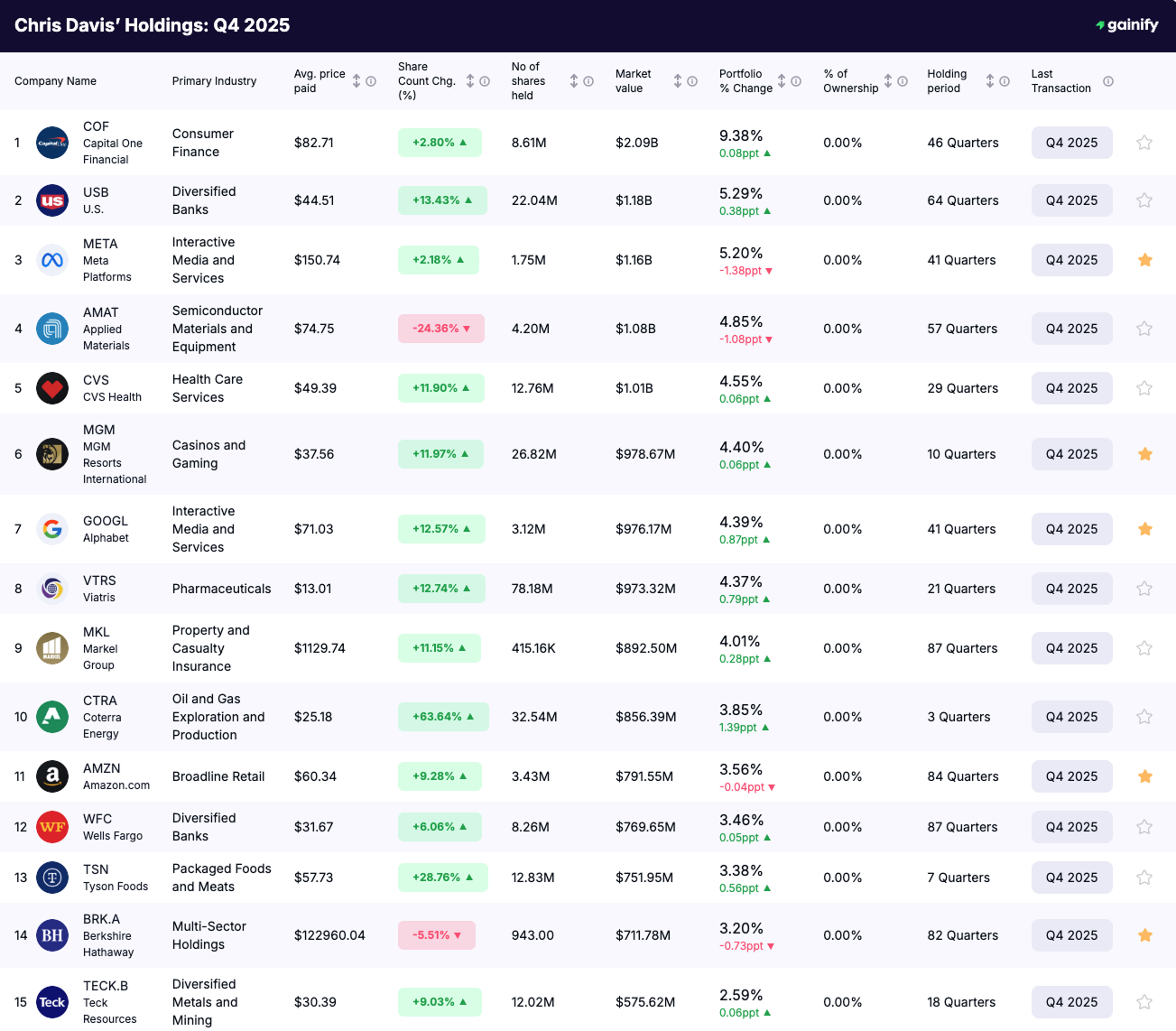

TheQ2 2025 13F portfolio consists of 108 stocks, with the top ten holdings making up 50.29% of total assets. That concentration means the performance of these companies has an outsized influence on overall returns.

Top 10 Holdings – Q4 2025

Rank | Company Name | Ticker | Portfolio Weight | Value ($B) | Industry / Sector |

|---|---|---|---|---|---|

1 | Capital One Financial | COF | 9.38% | 2.09 | Consumer Finance |

2 | U.S. Bancorp | USB | 5.29% | 1.18 | Diversified Banks |

3 | 5.20% | 1.16 | Interactive Media & Services | ||

4 | 4.85% | 1.08 | Semiconductor Materials & Equipment | ||

5 | CVS | 4.55% | 1.01 | Health Care Services | |

6 | MGM Resorts International | MGM | 4.40% | 0.98 | Casinos & Gaming |

7 | 4.39% | 0.98 | Interactive Media & Services | ||

8 | Viatris | VTRS | 4.37% | 0.97 | Pharmaceuticals |

9 | Markel Group | MKL | 4.01% | 0.89 | Property & Casualty Insurance |

10 | Coterra Energy | CTRA | 3.85% | 0.86 | Oil & Gas Exploration & Production |

The top of Chris Davis’ portfolio leans heavily toward financial services, which provide steady earnings and reliable dividends when managed well. These holdings are balanced with technology and communication services companies that offer higher growth potential through innovation and global reach. A smaller share is in consumer defensive and health care names, which can provide stability during economic slowdowns, while consumer discretionary positions like MGM Resorts add exposure to cyclical recovery and spending trends. Together, this mix combines dependable cash flow with selective growth opportunities, aiming to perform well across different market conditions.

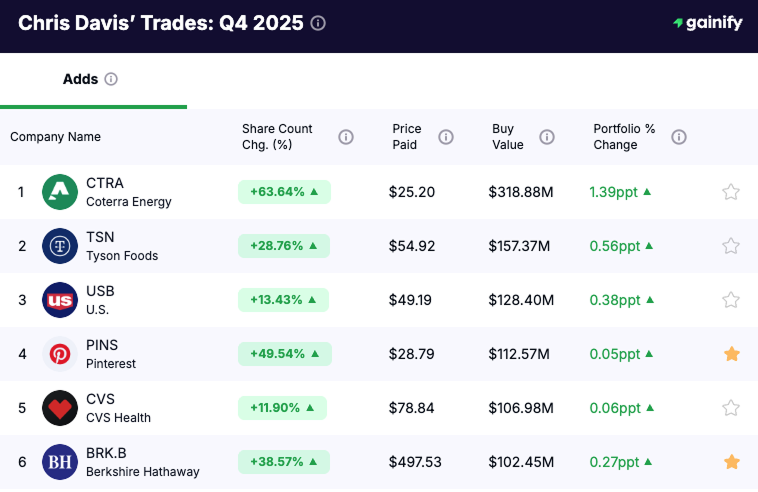

Top 6 Adds: Reinforcing Conviction

# | Company | Ticker | Change (%) | Current Shares | Current Value ($M) |

|---|---|---|---|---|---|

1 | Coterra Energy | CTRA | +63.64% | 32.54M | 856.39 |

2 | Tyson Foods | TSN | +28.76% | 12.83M | 751.95 |

3 | U.S. Bancorp | USB | +13.43% | 22.04M | 1,180.00 |

4 | Pinterest | PINS | +49.54% | 11.80M | 305.55 |

5 | CVS Health | CVS | +11.90% | 12.76M | 1,010.00 |

6 | BRK.B | +38.57% | 739.88K | 371.91 |

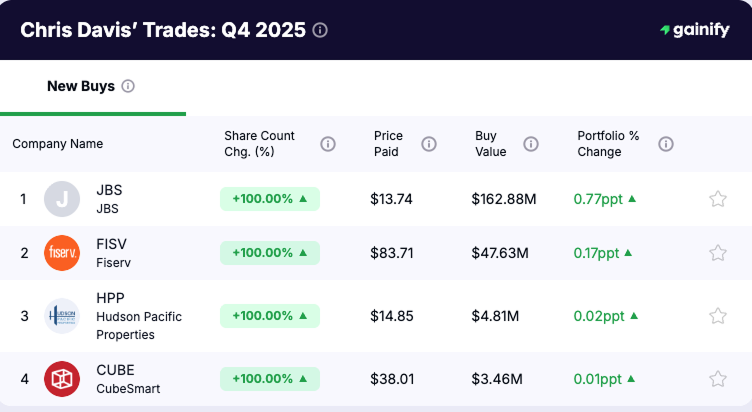

Top 4 New Buys: Fresh Opportunities

# | Company | Ticker | Change (%) | Buy Value ($M) | Portfolio % Change |

|---|---|---|---|---|---|

1 | JBS | JBS | +100.00% | 162.88 | +0.77ppt |

2 | FISV | +100.00% | 47.63 | +0.17ppt | |

3 | Hudson Pacific Properties | HPP | +100.00% | 4.81 | +0.02ppt |

4 | CubeSmart | CUBE | +100.00% | 3.46 | +0.01ppt |

Top 2 Sold Outs: Strategic Exits

# | Company | Ticker | Change (%) | Sell Value ($M) | Portfolio % Change |

|---|---|---|---|---|---|

1 | Humana | HUM | −100.00% | 101.07 | −0.52ppt |

2 | RH | RH | −100.00% | 0.38 | −0.00ppt |

Top 5 Reductions: Managing Risk and Rebalancing

# | Company | Ticker | Change (%) | Sell Value ($M) | Portfolio % Change |

|---|---|---|---|---|---|

1 | Applied Materials | AMAT | −24.36% | 324.29 | −1.08ppt |

2 | Bank of New York Mellon | BK | −48.38% | 54.10 | −0.30ppt |

3 | Berkshire Hathaway | BRK.A | −5.51% | 41.05 | −0.73ppt |

4 | NetEase | NTES | −28.34% | 23.93 | −0.21ppt |

5 | JPMorgan Chase | JPM | −4.04% | 7.44 | −0.15ppt |

6 | Extra Space Storage | EXR | −49.22% | 3.70 | −0.02ppt |

What Stands Out in Q4 2025

Chris Davis’ portfolio closed Q4 2025 back near 5-year highs, crossing $22B in value. This wasn’t driven by broad repositioning, but by steady conviction in existing holdings.

The most striking signal this quarter is concentration through confidence. 9 of the top 10 positions were increased, a strong indication that Davis leaned into what he already owns rather than rotating into new themes. That kind of behavior is consistent with his long-term approach and tends to show up near periods of high internal conviction.

Financials now clearly anchor the portfolio. Capital One and U.S. Bancorp sit as the top two positions, together representing a meaningful share of total assets. The positioning highlights Davis’ preference for scaled, cash-generative banks at a time when many investors remain cautious on the sector.

Outside of financials, increases across large holdings like Meta, Alphabet, CVS, and MGM suggest a broad willingness to add risk selectively, while trims elsewhere helped fund those moves without changing the portfolio’s overall character.

Taken together, Q4 2025 reflects a portfolio that is not chasing performance, but doubling down on core ideas as valuations, fundamentals, and long-term outlook align. Classic Davis behavior at a moment of renewed portfolio strength.

Why It Fits The Davis Playbook

Since 1969, Davis Advisors has built portfolios that combine resilience during market stress with the flexibility to capture growth when opportunities arise. That same formula is visible in the Q4 2025 holdings. The largest positions are companies with the financial strength and competitive advantages to weather downturns. At the same time, a carefully selected group of smaller holdings gives the portfolio room to adapt as new opportunities emerge.

The current mix leans toward leading financial institutions, advantaged technology platforms, and stable health care cash generators. Each has been chosen through deep, independent research and a focus on fundamentals like return on invested capital, balance sheet strength, and the ability to compound earnings over many years.

This disciplined ownership history – holding top companies for the long term while making selective, well-researched changes – has been central to Davis’ track record for more than five decades. Q4 2025 reflects that tradition, pairing patience with the conviction to act when the right ideas present themselves.