Earnings Per Share (EPS) shows how much of a company’s net income belongs to each common share after dividing total profits by the number of shares outstanding and adjusting for dilution.

In practical investing terms, the EPS meaning is that it converts total earnings into a standardized per-share unit that can be compared across companies, time periods, and capital structures.

EPS matters because it directly underpins how stocks are valued and evaluated. Public companies are required to report EPS under U.S. GAAP, and it is the core input for valuation metrics such as the price-to-earnings (P/E) ratio. As defined in accounting standards issued by the Financial Accounting Standards Board and enforced by the U.S. Securities and Exchange Commission, both basic EPS and diluted EPS must be disclosed to reflect the true earnings available to shareholders.

This article explains EPS in a strictly functional way. It defines how EPS is calculated, clarifies the difference between basic and diluted EPS, explains how EPS is used in valuation and forecasting, and outlines the key limitations investors must account for when relying on EPS in analysis.

Earnings Per Share in 60 Seconds: 5 Key Takeaways

- EPS is profit per share: it shows how much net income is attributable to each common share.

- Two EPS types matter: n the calculation, basic EPS uses current shares outstanding, while diluted EPS also includes potential shares from options, stock awards, and convertibles.

- EPS is not a cash flow metric: reported earnings per share can diverge materially from operating cash flow and free cash flow.

- Share buybacks can lift EPS: reducing the share count increases EPS even if total net income is unchanged.

- Adjusted EPS requires scrutiny: management-defined exclusions can raise “adjusted” EPS, so compare it against the standard GAAP EPS.

What is EPS?

Earnings per share (EPS) is a profitability metric that converts a company’s total earnings into a per-share figure. It answers a simple investor question: how much of the period’s reported profit is attributed to each share of common stock. This is why EPS is used to compare profitability across companies and to evaluate earnings growth over time.

Under U.S. GAAP, EPS is not an informal metric. It is a standardized disclosure governed by the Financial Accounting Standards Board (FASB) in ASC 260 (Earnings Per Share). The purpose of this standard is comparability: two companies with the same net income can produce different earnings per share if their share counts differ or if one has meaningful dilution from stock-based compensation or convertible securities.

U.S. GAAP requires companies to present two EPS figures on the income statement. Basic EPS uses the current weighted-average shares outstanding. Diluted EPS expands the share count to include securities that could become common shares, such as options, restricted stock awards, and convertibles. This requirement exists because dilution changes the economic claim each share has on earnings.

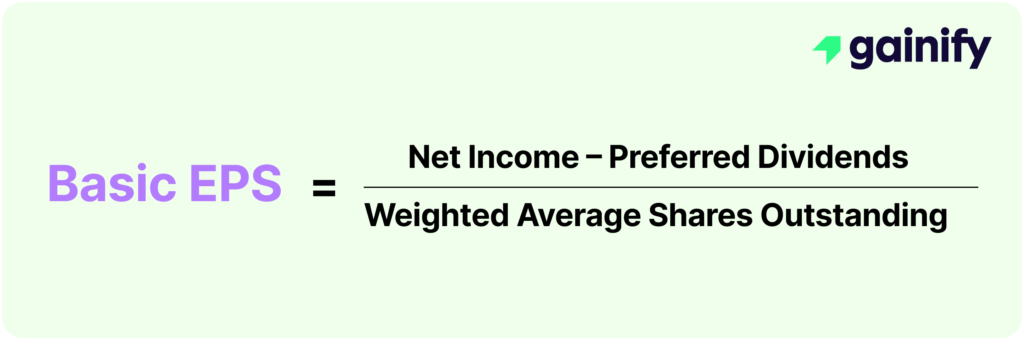

Basic EPS

Basic EPS is the earnings per share figure calculated using only common shares that were actually outstanding during the period. Under U.S. GAAP, the goal of basic EPS is to express profit attributable to common shareholders on a per-share basis using the period’s real share base, adjusted for any share count changes through a weighted-average approach.

Basic EPS Formula

Basic EPS = (Net income − Preferred dividends) ÷ Weighted-Average Common Shares Outstanding

Two inputs determine basic EPS:

- Net income attributable to common shareholders: the profit remaining for common shareholders after any amounts allocated to preferred shareholders and other non-common interests.

- Weighted-average common shares outstanding: the time-weighted share count that reflects issuances and buybacks during the reporting period, rather than a single point-in-time share number.

This is the baseline EPS figure investors see in filings before any adjustment for potential dilution. Next, we’ll show how companies compute the weighted-average share count and why that step matters for accurate EPS.

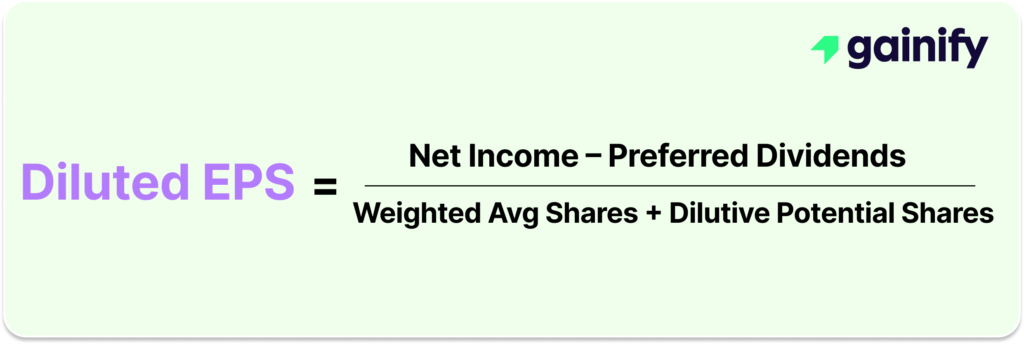

Diluted EPS

Diluted EPS is the earnings per share figure calculated using a share count that includes common shares outstanding plus additional shares that could be created from dilutive securities. Under U.S. GAAP, diluted EPS is required when a company has instruments that can convert into common stock or create new shares, because those instruments reduce the earnings attributable to each share.

Diluted EPS Formula

Diluted EPS = (Net Income − Preferred Dividends) ÷ (Weighted-Average Shares Outstanding + Dilutive Potential Shares)

The key difference versus basic EPS is the denominator. Diluted weighted-average shares start with the basic weighted-average share count, then add incremental shares that could be created from dilutive securities, including:

- Stock options and warrants

- Restricted stock units (RSUs) and other equity awards

- Convertible debt

- Convertible preferred stock

Under U.S. GAAP, only instruments that reduce earnings per share are included. Instruments that would increase EPS (anti-dilutive instruments) are excluded.

Next, we apply this to Tesla’s filing and show how its diluted share count translates into a lower diluted EPS versus basic EPS.

Example: Tesla EPS in a Real Income Statement

Tesla reports basic EPS and diluted EPS in its Form 10-K because earnings per share changes depending on the share count used in the calculation. In its income statement, Tesla discloses both EPS values and the matching weighted-average shares used for each figure. Investors need to separate these two numbers because they represent different per-share earnings claims.

For the year ended December 31:

Tesla | 2025 | 2024 | 2023 |

|---|---|---|---|

EPS (Basic) | 1.18 | 2.23 | 4.73 |

EPS (Diluted) | 1.08 | 2.04 | 4.30 |

Weighted-avg shares (Basic) | 3,225 | 3,197 | 3,174 |

Weighted-avg shares (Diluted) | 3,528 | 3,498 | 3,485 |

In each year shown, diluted EPS is lower than basic EPS because the diluted share count is higher than the basic share count. That mechanical difference is why filings present both lines and why analysts treat them separately in models.

Tesla’s EPS differences come directly from the denominator. The income statement shows a larger diluted weighted-average share count than the basic share count in every year, which automatically produces a lower diluted EPS even if the numerator (net income available to common shareholders) stays the same.

For 2025, Tesla reports:

- Basic EPS: 1.18 using 3,225 million weighted-average basic shares

- Diluted EPS: 1.08 using 3,528 million weighted-average diluted shares

That means the diluted share count is 303 million shares higher (3,528M − 3,225M) than the basic share count for the same period. When the same earnings are spread across more shares, the per-share figure declines. The same pattern appears in 2024 and 2023, where diluted shares exceed basic shares and diluted EPS prints below basic EPS.

Common Sources of Dilution in EPS Calculations

Dilutive potential shares are securities that can increase the common share count, which reduces earnings per share when included in diluted EPS. In practical terms, these instruments represent future equity issuance tied to employee compensation or financing terms.

The most common sources in public company filings are:

- Stock options and warrants: contracts that allow holders to buy shares at a set price, creating new shares when exercised.

- RSUs and other stock awards: equity compensation that converts into shares as it vests.

- Convertible debt: bonds that can convert into common shares, increasing share count if conversion is assumed.

- Convertible preferred stock: preferred shares that can convert into common shares under specified terms.

Companies include only instruments that are dilutive under U.S. GAAP. If an instrument would increase EPS rather than reduce it, it is classified as anti-dilutive and excluded from diluted EPS.

Where to Find EPS Metrics in Company Reports

EPEPS metrics are disclosed in two places inside a company’s SEC filings, and each has a specific role. The income statement in the Form 10Q (quarterly) and Form 10K (annual) shows the headline EPS numbers because it reports basic EPS, diluted EPS, and the related weighted-average share counts for the period. This is where you capture the “what” quickly: the EPS the company reported and the share base used to calculate it. The detail that explains those numbers sits in the notes to the financial statements within the same 10-Q or 10-K, typically in an Earnings Per Share footnote. That footnote shows the share-count build and the dilution mechanics, including which instruments (options, RSUs, warrants, convertibles) increased diluted shares and which instruments were excluded as anti-dilutive.

- Where to look: income statement in the 10Q/10K (basic EPS, diluted EPS, share counts) + EPS footnote in the notes (dilution sources and share-count reconciliation)

Next, we move to why earnings per share matters and how investors use EPS in valuation and earnings expectations.

Why EPS Matters in Equity Valuation

EPS is one of the most integral metrics in the toolkit of equity investors, financial analysts, and institutional asset managers. It serves as a standardized gauge of per-share profitability and plays a pivotal role in assessing value, tracking performance, and guiding investment decisions.

Here’s why EPS is so essential:

- Valuation Benchmark: EPS is the denominator in the Price-to-Earnings (P/E) ratio, one of the most widely used valuation multiples. The P/E ratio helps investors assess how much they are paying for each unit of earnings. A higher EPS can reduce a company’s P/E multiple, suggesting potential undervaluation if share price remains constant.

- Earnings Growth Tracking: Consistent and growing EPS over time is a hallmark of financially healthy, well-managed companies. Accelerating EPS growth often drives stock price appreciation and signals strong business momentum.

- Impact on Dividend Policy: EPS is a key factor in determining a company’s capacity to pay and grow dividends. A high or rising EPS gives companies more flexibility to increase payouts or reinvest in growth initiatives. Conversely, declining EPS may limit future dividend potential.

- Market Sentiment and Volatility: Quarterly EPS results often influence short-term market sentiment. Earnings “beats” or “misses” relative to consensus EPS forecasts frequently move stock prices and trigger revisions in analyst ratings.

Ultimately, EPS is a bridge between a company’s financial performance and its market valuation. While it should never be viewed in isolation, it remains one of the most insightful indicators of shareholder value creation and business strength.

Limitations of EPS

EPS is useful, but it is not a complete measure of shareholder value because it compresses multiple moving parts into one accounting output. Investors misread earnings per share when they ignore what sits behind the numerator (earnings quality) and denominator (share count mechanics). EPS can hide the following issues.

- Capital Structure Sensitivity: EPS can be distorted by changes in share count. Share buybacks artificially inflate EPS without necessarily improving true profitability, while new share issuance can dilute EPS even when earnings remain unchanged.

- Ignores Balance Sheet Risk: EPS provides no insight into a company’s leverage, liquidity, or capital efficiency. Two companies with identical EPS may have very different financial risk profiles depending on their debt levels and balance sheet strength.

- Earnings Management Exposure: Companies can influence EPS through accounting choices such as accelerating revenue, deferring expenses, or using reserves. These techniques can legally manipulate reported results, making EPS potentially misleading if not supported by strong earnings quality.

- Adjusted EPS Lack of Uniformity: Non-GAAP EPS figures are calculated differently across companies. Management teams have wide discretion in what they include or exclude, making cross-company comparisons challenging and sometimes misleading.

- Variability Across Accounting Standards: EPS results may differ significantly under GAAP versus IFRS or other local standards due to differences in revenue recognition, expense treatment, and depreciation. This affects comparability across regions and jurisdictions.

- Overemphasis on Short-Term Performance: Because markets often react to quarterly EPS surprises, there can be pressure on management to focus on short-term earnings at the expense of long-term strategy and investment.

EPS is a vital part of the financial analysis toolkit but should be interpreted alongside a broader set of metrics, including cash flow, return on capital, and balance sheet health, to gain a holistic view of company performance.

How Share Buybacks and Dilution Change EPS

Share buybacks and dilution change EPS by changing the denominator of the EPS calculation: the weighted-average share count. When the share count falls, the same earnings are allocated across fewer shares, which increases earnings per share. When the share count rises, the same earnings are spread across more shares, which reduces earnings per share.

Share Buybacks

A buyback reduces shares outstanding. If net income stays flat, EPS increases mechanically because the denominator declines. This is why companies with stable earnings can still report EPS growth when they consistently repurchase stock. The effect is strongest when buybacks are large relative to the share base and executed over long periods.

Dilution

Dilution increases the share count through equity issuance and through the conversion or exercise of dilutive instruments. The most common source in modern public companies is stock-based compensation (RSUs and options), which increases diluted shares even when the company is also repurchasing stock. In that case, buybacks may only offset dilution rather than reduce the net share count.

In practice, investors assess whether a company is truly shrinking its share base or simply using buybacks to neutralize dilution. That distinction determines whether EPS growth reflects real per-share value creation or only maintenance of the per-share earnings claim.

Next, we move to GAAP vs non-GAAP (adjusted) EPS and explain why “adjusted EPS” often differs from the standardized EPS reported under U.S. GAAP.

U.S. GAAP EPS vs Non-GAAP EPS

GAAP EPS is the standardized earnings per share number reported in a company’s Form 10-Q and Form 10-K under U.S. GAAP rules (FASB ASC 260). Non-GAAP EPS (often called “adjusted EPS”) is a management-defined version that modifies GAAP earnings to remove selected items. Investors use the table below to separate what is standardized from what is discretionary.

Feature | GAAP EPS | Non-GAAP (Adjusted) EPS |

|---|---|---|

Where you see it | 10-Q / 10-K income statement | Earnings release, investor deck, call transcript |

Who sets the rules | FASB (ASC 260) | Management-defined methodology |

What it measures | Reported net income per share under GAAP | “Core” earnings per share after exclusions |

Comparability | High across companies | Low–medium (varies by company) |

Common exclusions | None (includes all GAAP items) | Restructuring, impairments, litigation, acquisition costs, stock-based comp, one-time gains/losses |

Main risk | Can be affected by accounting estimates | Can be selectively adjusted to improve optics |

Required disclosure | Must report basic and diluted EPS | Must show GAAP EPS alongside and reconcile adjustments (SEC requirement) |

EPS Meaning: Bottom Line

EPS remains one of the most essential and widely scrutinized metrics in modern financial analysis. It condenses complex income statement data into a single, per-share figure that reflects the company’s ability to generate profits for its shareholders. Whether used for valuation, profitability assessment, dividend forecasting, or performance benchmarking, EPS is deeply embedded in both fundamental and quantitative investing frameworks.

EPS becomes useful only when the inputs are understood. Basic vs. diluted EPS changes the share base, buybacks and dilution can move EPS without changing the business, and GAAP vs. adjusted EPS can change the earnings figure without improving underlying economics.

Use EPS as a starting point, not a final answer. The correct workflow is to identify what drove EPS, then validate it against cash flow, balance-sheet risk, and share count trends to determine whether per-share profitability reflects durable value creation.

EPS Meaning FAQ

What is EPS meaning in simple terms?

EPS meaning is profit per share: how much net income is allocated to each common share for a reporting period after accounting for the share count and, in diluted EPS, potential dilution.

What is the EPS formula?

The basic EPS formula is (Net income − preferred dividends) ÷ weighted-average common shares outstanding.

What is diluted EPS in the calculation?

Diluted EPS in the calculation uses a larger share count by adding dilutive potential shares (options, RSUs, warrants, convertibles) to the weighted-average shares.

Should I use basic EPS or diluted EPS?

You should use diluted EPS for most stock analysis because it reflects the earnings claim after potential dilution from equity awards and convertible securities.

Why is diluted EPS lower than basic EPS?

Diluted EPS is lower than basic EPS because diluted weighted-average shares are higher, so the same earnings are divided across more shares.