Beer may be one of the world’s oldest products, but the business behind it has evolved into a global powerhouse. From mass-market lagers to high-end craft labels, today’s brewers combine brand power, pricing discipline, and global reach to drive growth.

For investors, beer stocks offer a unique balance. They’re part of the consumer staples sector, providing stability and reliable dividends, yet also carry cyclical upside tied to economic growth, tourism, and emerging-market demand.

The modern beer industry is led by a handful of global giants like Anheuser-Busch InBev, Heineken, and Carlsberg, alongside strong regional players in Japan, the U.S., and Latin America. Together, they brew billions of liters each year and generate enormous free cash flow.

Below are the top nine publicly traded beer stocks as of November 2025.

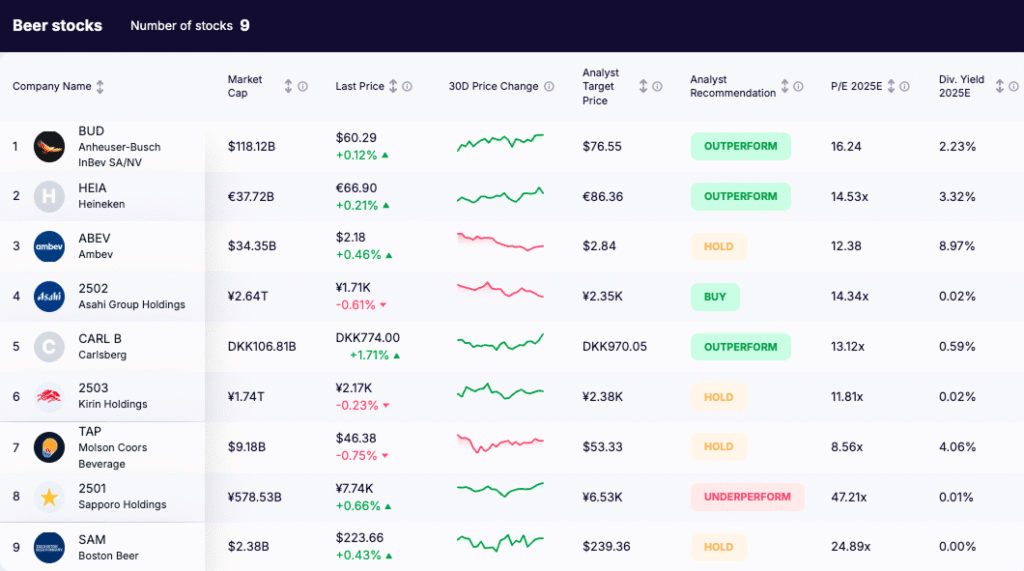

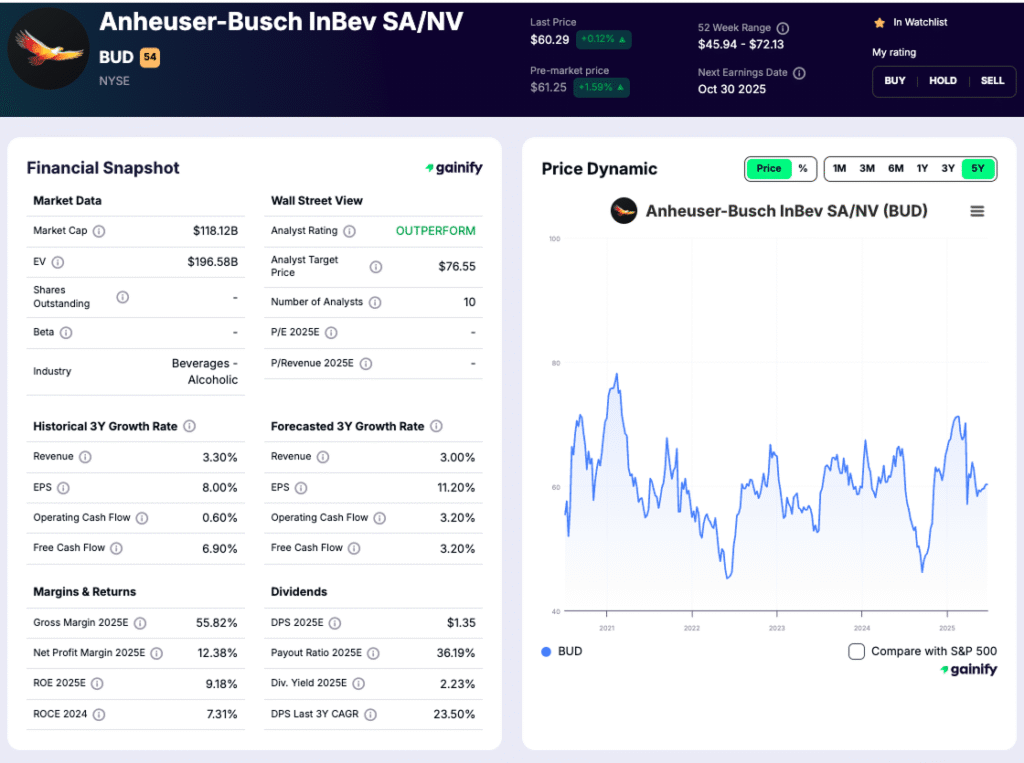

1. Anheuser-Busch InBev (BUD)

P/E 2025E: 16.2x | Free Cash Flow Yield 2025E: 8.9% | Dividend Yield 2025E: 2.2%

What they do:

Anheuser-Busch InBev (BUD) is the world’s largest brewer, producing and selling more than 500 beer brands, including Budweiser, Stella Artois, and Corona. The company operates in over 150 countries with leading market positions across Latin America, Europe, and Africa.

Why it matters:

In 2025, AB InBev is focused on margin recovery after two volatile years for input costs and FX swings. Its premium and no-alcohol lines are expanding quickly in Latin America and Europe, while North American volumes have stabilized after brand headwinds in 2023–24. Debt levels are now close to management’s medium-term target, giving room for higher shareholder returns.

What to watch:

- Pricing power in emerging markets as inflation cools

- Growth in Budweiser Zero and regional premium offerings

- Balance between deleveraging and dividend growth

Key risk:

A slowdown in emerging-market consumption or weaker brand performance in North America could weigh on earnings momentum.

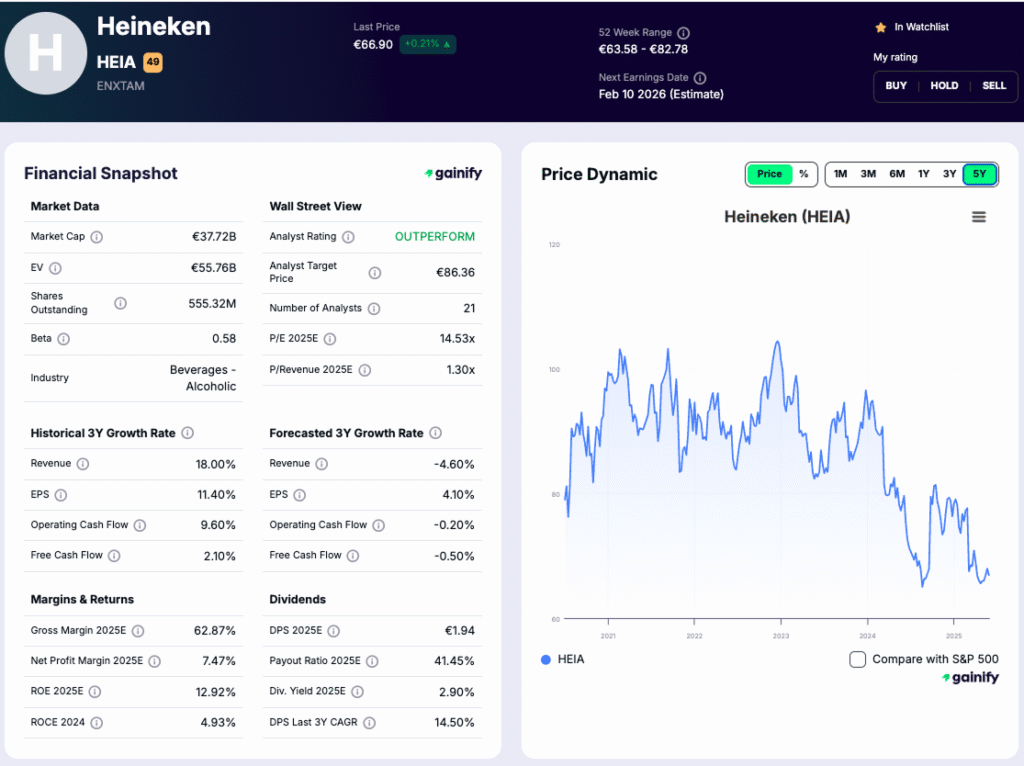

2. Heineken (HEIA)

P/E 2025E: 14.8× | Free Cash Flow Yield 2025E: 7.1% | Dividend Yield 2025E: 3.2%

What they do:

Heineken (HEIA) is the world’s second-largest brewer, producing over 300 beer and cider brands, including Heineken, Amstel, Tiger, and Birra Moretti. The company operates in more than 190 countries and has a strong presence across Europe, Africa, and Southeast Asia.

Why it matters:

In 2025, Heineken continues to prioritize premiumization and digitalization to drive margin expansion. Despite slower European volumes, pricing initiatives and strong growth in Asia and Africa are supporting revenue. The company’s cost-savings program and disciplined capital allocation are improving cash flow visibility after several years of input cost volatility.

What to watch:

- Volume recovery in Europe and sustained growth in Asia-Pacific

- Performance of premium and 0.0 (non-alcoholic) segments

- Execution on cost efficiency targets and working-capital control

Key risk:

Persistent cost pressures or currency volatility in key emerging markets could offset pricing gains, while weak consumer sentiment in Europe remains a drag on volume growth.

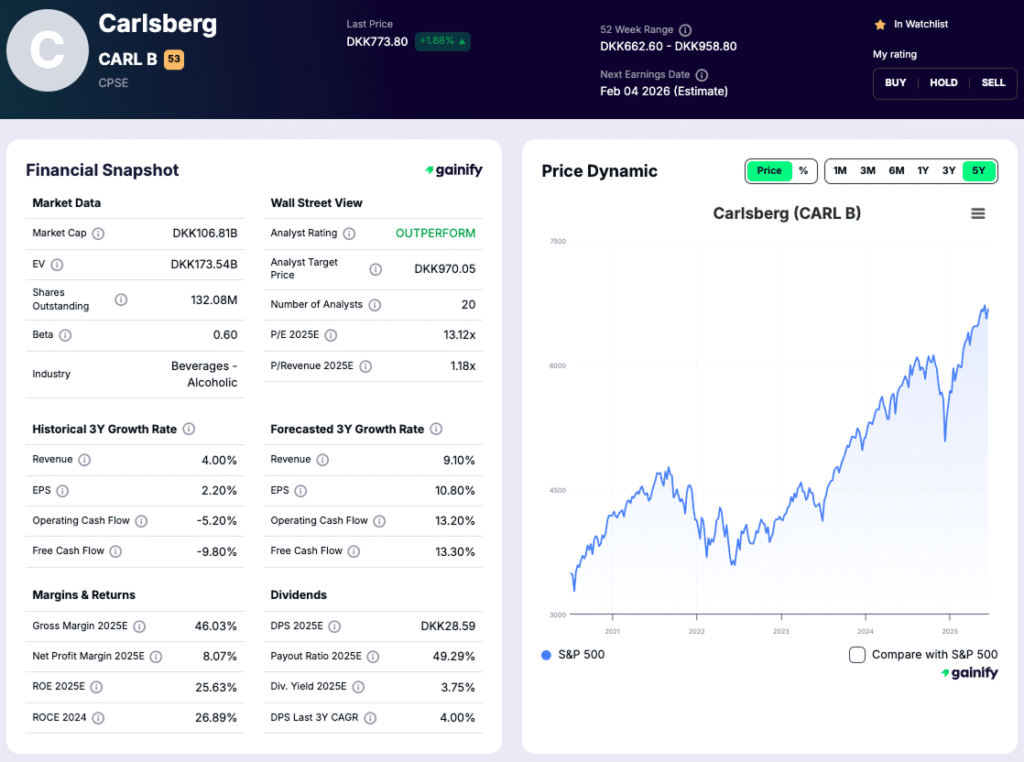

3. Carlsberg (CARL B)

P/E 2025E: 15.1× | Free Cash Flow Yield 2025E: 6.4% | Dividend Yield 2025E: 2.8%

What they do:

Carlsberg (CARL B) is one of Europe’s largest brewers, with leading brands such as Carlsberg, Tuborg, 1664, and Baltika. The company operates across Western Europe, Asia, and Eastern Europe, with Asia now accounting for more than 40% of group profits.

Why it matters:

In 2025, Carlsberg is leaning heavily on its Asian portfolio (particularly markets like China, Vietnam, and India) to drive growth as European demand stays soft. Management has focused on improving pricing discipline, brand mix, and cost efficiency after divesting its Russia operations in 2023.

What to watch:

- Volume growth and pricing power in Asia

- Ongoing brand premiumization and mix improvement

- Execution of its “SAIL’27” strategy, aimed at steady EPS and margin growth

Key risk:

Exposure to slower European markets and currency fluctuations in Asia could limit profit expansion. A rise in input costs, especially barley and packaging materials, remains another watchpoint.

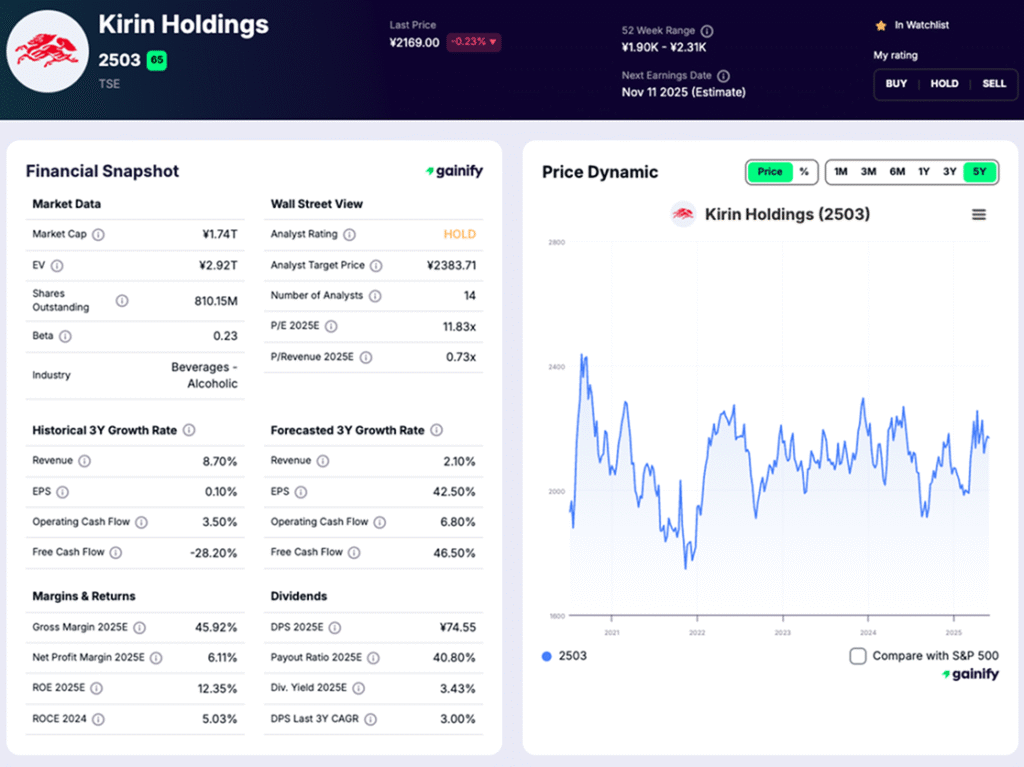

4. Kirin Holdings (2503)

P/E 2025E: 15.4× | Free Cash Flow Yield 2025E: 5.8% | Dividend Yield 2025E: 2.6%

What they do:

Kirin Holdings (2503) is one of Japan’s largest beverage and food companies, best known for Kirin Lager and Ichiban Shibori. Beyond beer, it operates diversified businesses in soft drinks, pharmaceuticals, and health sciences, giving it a broader revenue base than most brewers.

Why it matters:

In 2025, Kirin benefits from a rebound in on-premise sales across Japan and Southeast Asia, alongside steady growth in its wellness and biotech divisions. This diversification helps cushion earnings against beer-market volatility.

What to watch:

- Beer volume recovery in Japan and Asia-Pacific markets

- Growth contribution from its health and functional beverage segments

- Ongoing share buyback and shareholder-return policy execution

Key risk:

Weak domestic demand in Japan and a slower recovery in tourist-driven consumption could weigh on volumes. Currency fluctuations and soft consumer sentiment across Asia remain potential earnings headwinds.

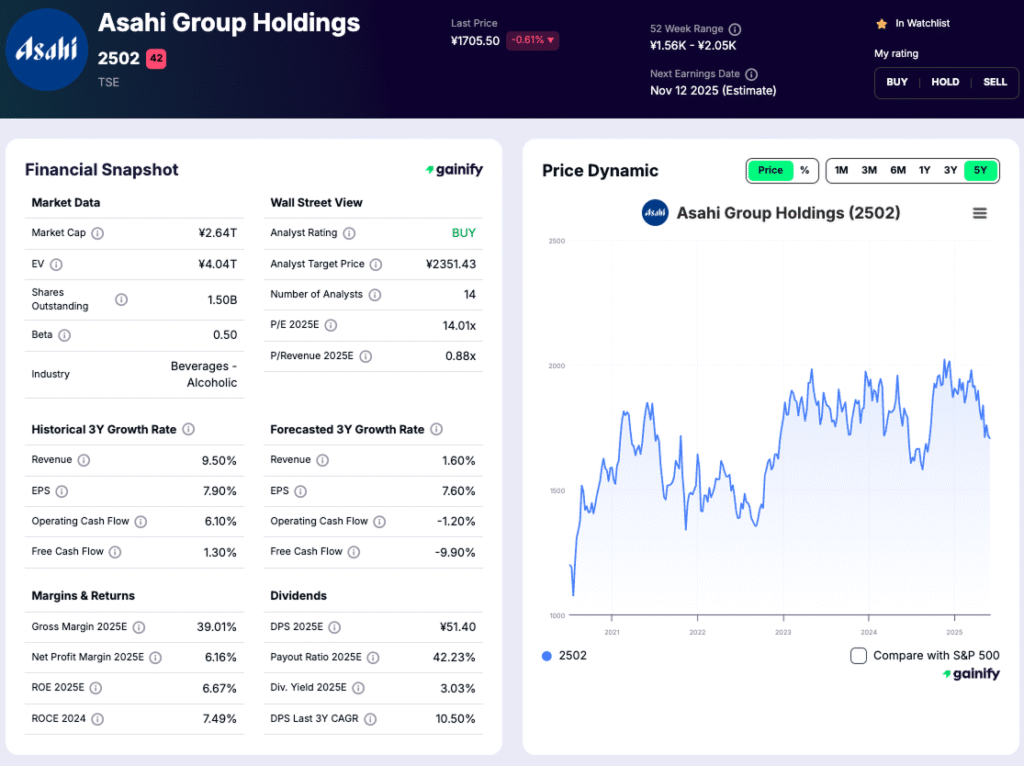

5. Asahi Group Holdings (2502)

P/E 2025E: 16.0× | Free Cash Flow Yield 2025E: 6.1% | Dividend Yield 2025E: 2.5%

What they do:

Asahi Group Holdings (2502) is a leading Japanese beverage company with global beer brands including Asahi Super Dry, Peroni, and Pilsner Urquell. The group also operates a large soft drinks business and has strong positions in Australia and Europe following major acquisitions in recent years.

Why it matters:

In 2025, Asahi is benefiting from premium brand strength and its broad geographic mix. The company continues to see strong sales in Europe and Southeast Asia, offsetting softer volumes in Japan. Management is focused on expanding non-alcoholic and low-alcohol lines, while maintaining disciplined capital allocation and cash generation.

What to watch:

- Growth of premium and non-alcoholic product categories

- Currency movements affecting overseas earnings repatriation

- Continued integration and cost synergies from global acquisitions

Key risk:

Weak demand in Japan and exposure to volatile input costs in Europe could limit near-term margin expansion. Slower global beer consumption could also weigh on top-line growth.

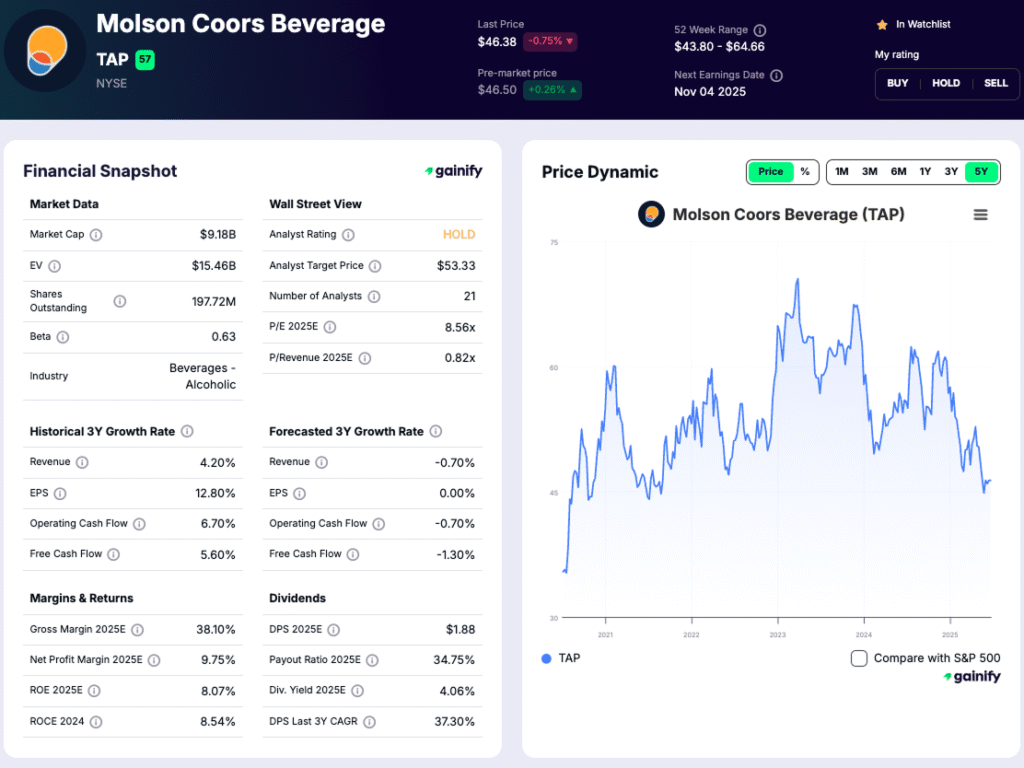

6. Molson Coors Beverage Company (TAP)

P/E 2025E: 12.4× | Free Cash Flow Yield 2025E: 8.3% | Dividend Yield 2025E: 3.1%

What they do:

Molson Coors (TAP) is one of North America’s largest brewers, known for Coors Light, Miller Lite, and Blue Moon. The company operates primarily in the U.S., Canada, and Europe, with a growing focus on beyond-beer products, including energy drinks, canned cocktails, and non-alcoholic beverages.

Why it matters:

In 2025, Molson Coors is emerging from several years of restructuring with improved margins and a stronger balance sheet. The company continues to benefit from its premiumization strategy, as well as market share gains in light beer following competitor brand controversies. Cash generation remains robust, supporting ongoing dividend increases and share buybacks.

What to watch:

- Ongoing shift toward premium and non-alcoholic segments

- Pricing and volume performance in the U.S. light beer market

- Expansion of the energy and ready-to-drink portfolio

Key risk:

Persistent cost inflation and slower North American beer demand could pressure margins. Shifting consumer preferences toward spirits or alternative drinks may limit long-term volume recovery.

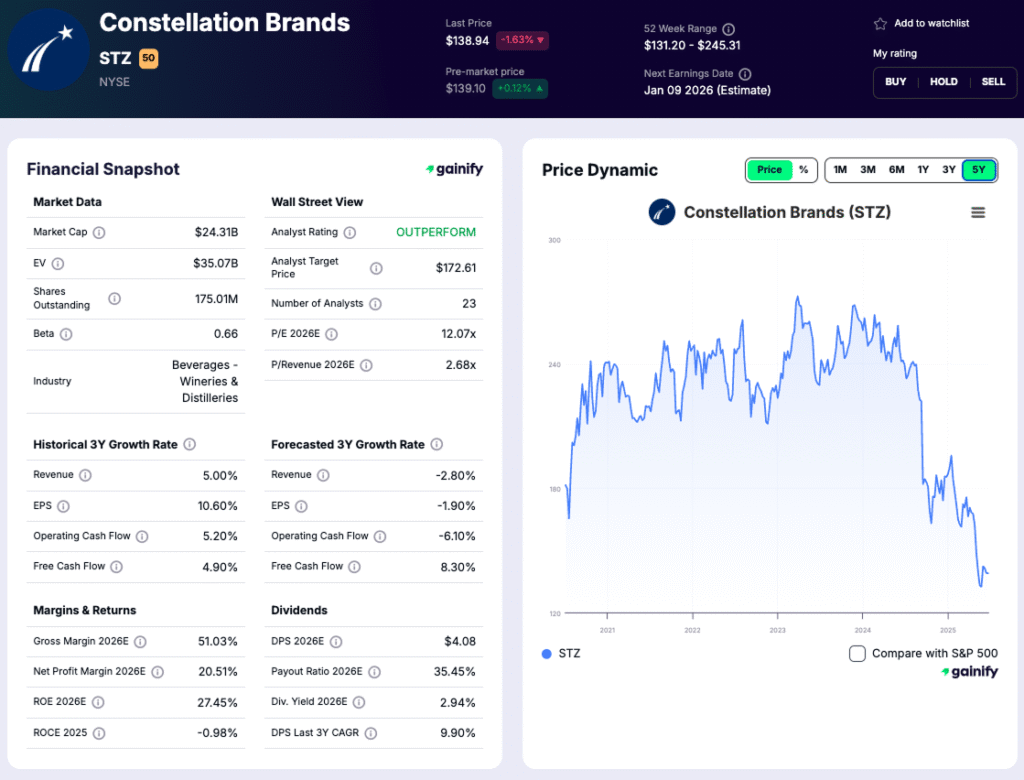

7. Constellation Brands (STZ)

P/E 2025E: 18.3× | Free Cash Flow Yield 2025E: 5.6% | Dividend Yield 2025E: 1.5%

What they do:

Constellation Brands (STZ) is a U.S.-based beverage company best known for its Mexican beer portfolio, which includes Corona, Modelo Especial, and Pacifico (imported under license from Grupo Modelo). The company also owns a portfolio of premium wines and spirits, although beer remains its largest and most profitable segment.

Why it matters:

In 2025, Constellation continues to deliver industry-leading growth within the U.S. beer market, driven by premium imports and Hispanic demographic trends. Modelo Especial has overtaken Bud Light as the top-selling beer in America, providing a major tailwind. Margin expansion and consistent free cash flow have allowed management to raise dividends and buy back shares while reducing leverage.

What to watch:

- Ongoing U.S. beer market share gains and pricing trends

- Potential impact of import cost inflation and FX volatility with Mexico

- Strategic updates on portfolio simplification and capital allocation

Key risk:

Heavy reliance on imported Mexican beer exposes the company to trade, logistics, and FX risk. A consumer shift toward local or craft brands could also temper long-term volume growth.

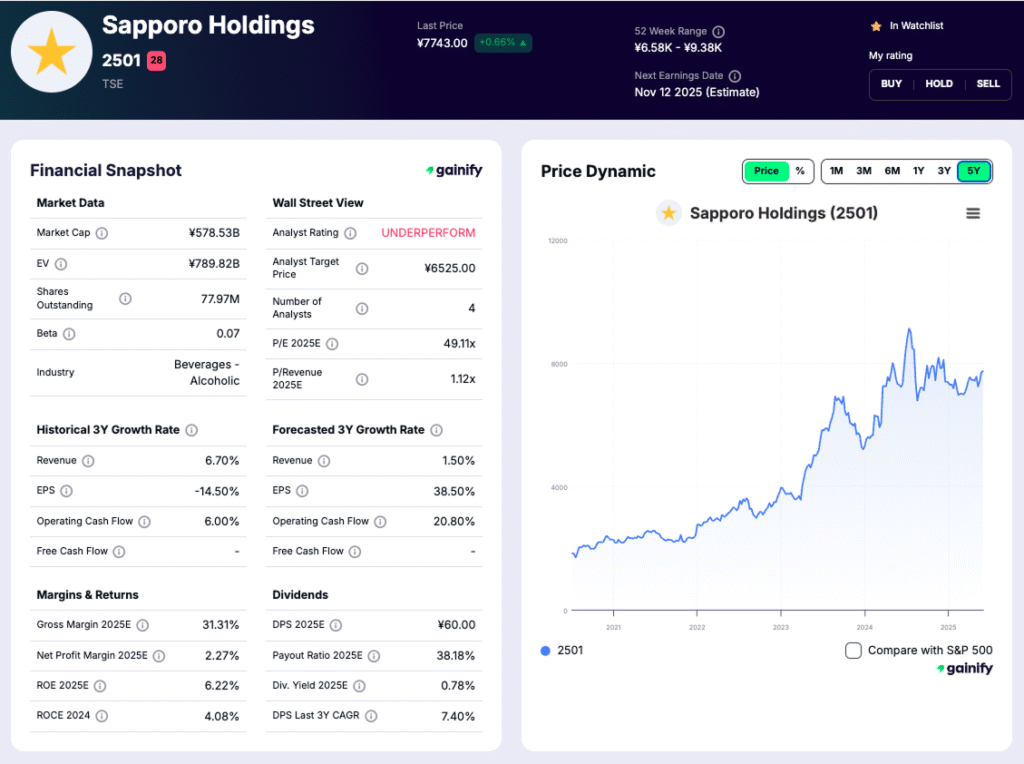

8. Sapporo Holdings (2501)

P/E 2025E: 14.2× | Free Cash Flow Yield 2025E: 5.1% | Dividend Yield 2025E: 2.1%

What they do:

Sapporo Holdings (2501) is one of Japan’s oldest brewers, best known for Sapporo Premium Beer and Yebisu. The company operates across Japan, North America, and Southeast Asia, and also manages a real estate and food division, which provides steady non-beer income.

Why it matters:

In 2025, Sapporo is focusing on international expansion and efficiency improvements following a multi-year restructuring. Its North American business continues to grow, especially after integrating Stone Brewing, which strengthened its U.S. craft presence. Management’s focus on profitability over volume and a refreshed brand lineup are helping margins recover.

What to watch:

- Integration progress and profitability from the U.S. business

- Recovery in Japan’s on-premise (bars and restaurants) consumption

- Expansion in Southeast Asia and premium craft categories

Key risk:

A weaker yen increases import costs, while slowing domestic demand and intense competition could pressure volume growth. Execution risk remains around overseas expansion and brand repositioning.

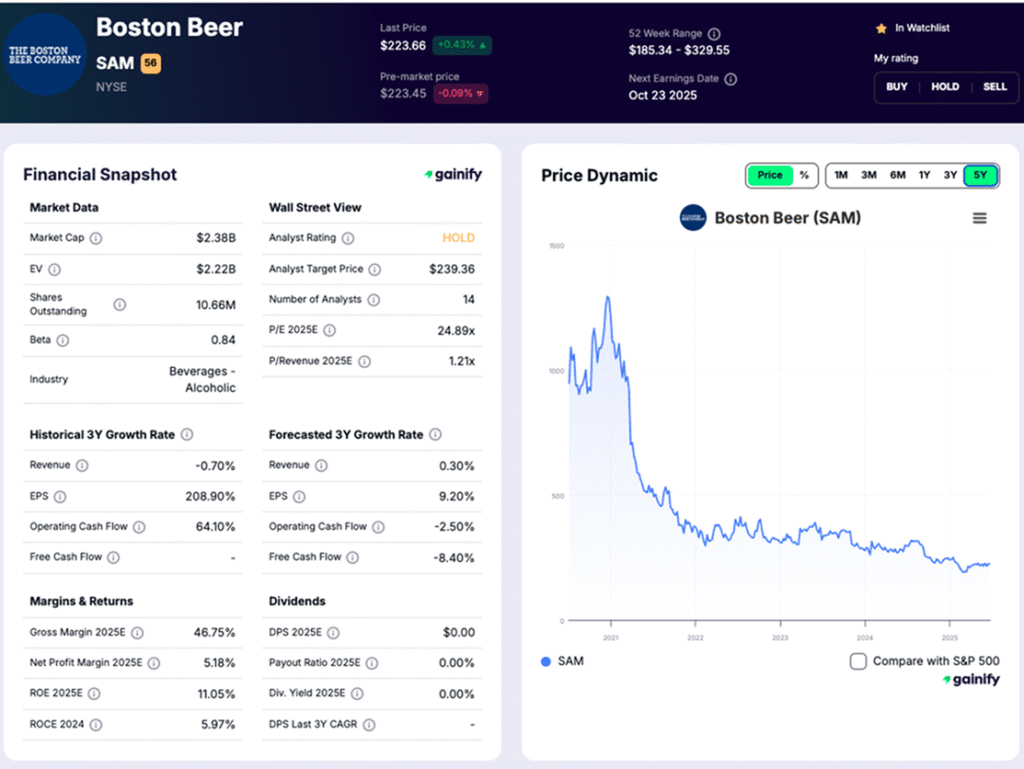

9. The Boston Beer Company (SAM)

P/E 2025E: 22.5× | Free Cash Flow Yield 2025E: 4.3% | Dividend Yield 2025E: N/A

What they do:

The Boston Beer Company (SAM) is one of the leading U.S. craft brewers, best known for Samuel Adams, Truly Hard Seltzer, Angry Orchard Cider, and Twisted Tea. The company distributes primarily in North America, with a growing focus on ready-to-drink (RTD) beverages and alcohol alternatives.

Why it matters:

In 2025, Boston Beer finds it hard to rebuild momentum after a few challenging years for the hard seltzer category. The company’s Twisted Tea brand continues to deliver strong double-digit growth, offsetting declines in Truly and boosting overall profitability. Management remains focused on innovation, cost efficiency, and expanding into new beverage categories, including non-alcoholic options.

What to watch:

- Growth trajectory of Twisted Tea and recovery of the Truly brand

- Expansion into RTD cocktails and other new beverage formats

- Cost control and gross margin improvement initiatives

Key risk:

Category volatility remains high as consumer tastes shift rapidly. A further slowdown in the seltzer market or weaker demand for craft beer could weigh on revenue growth. Input-cost inflation, especially for aluminum and transportation, also poses risk to margins.

Key Risks for Beer Stocks in 2026

Even with their defensive appeal, beer companies face a mix of structural and cyclical headwinds that investors should monitor closely.

A. Slower consumer demand

Inflation and weaker real income growth have made consumers more price-sensitive, especially in Europe and North America. Premium brands are holding up, but value tiers and low-cost competitors are regaining share.

B. Input cost volatility

Barley, aluminum, and energy prices remain unpredictable. While brewers have improved hedging and pricing power, margin compression is still a risk if raw materials rise faster than retail prices.

C. Currency and emerging-market exposure

With most major brewers generating 40–60% of profits outside their home markets, swings in FX — particularly the Brazilian real, Mexican peso, and Japanese yen — can significantly affect reported earnings and cash flow.

D. Regulatory pressure and health trends

Tighter rules on alcohol marketing, sugar content, and labeling continue to expand across Europe and Asia. At the same time, consumer preference is gradually shifting toward low- or no-alcohol alternatives, forcing portfolio adaptation and R&D costs.

F. Climate and sustainability challenges

Extreme weather events are increasingly disrupting crop yields and water supply. Sustainability investments are rising, but climate risk remains a long-term challenge to sourcing stability and production costs.

G. Shifting category dynamics

Competition from spirits, RTD cocktails, and cannabis-infused beverages is intensifying, particularly among younger consumers in North America. Beer brands must innovate to stay relevant in changing consumption patterns.

Beer Stocks: Key Market Trends (November 2025)

Trend Theme | Current Situation (2025) | Investor Takeaway |

Revenue Growth | Global beer volumes have grown only 1–2% annually, with pricing driving most of the top-line gains. Premiumization is offsetting weaker mass-market demand. | Growth is low-single-digit, making cost discipline and pricing strategy key to earnings momentum. |

Valuation Multiples | Sector trades at mid–to–high teens P/E (14x–18x), below historical averages and broader consumer staples. | Reflects slower growth and margin pressure; selective re-rating possible as inflation stabilizes. |

Free Cash Flow & Dividends | Strong cash generation (average 5–8% FCF yield) supports healthy dividends in the 2–4% range. | Cash returns remain a core attraction; dividend reliability anchors valuations. |

Profit Margins | Input-cost relief in 2025 is helping margins recover slightly after two inflation-heavy years. | EBITDA margins improving 50–100 bps, but still below 2021 peaks. |

Geographic Mix | Emerging markets now drive over half of industry EBITDA, led by Latin America, Africa, and Southeast Asia. | FX risk remains high, but long-term demand growth favors these regions. |

Market Performance (5Y) | Most beer stocks are flat to modestly up (0–25%) over the past five years, underperforming global equities. | Defensive but uninspiring returns; investors rewarded more for dividends than capital gains. |

Consumer Trends | Shift toward low-alcohol, no-alcohol, and premium offerings, especially in younger demographics. | Innovation is essential, as brewers must adapt to changing drinking habits to sustain relevance. |