SaaS (Software as a Service) stocks are at the core of today’s technology market. They power the digital systems that businesses depend on every day.

These companies earn steady, recurring revenue through subscription-based models that bring stability and growth potential.

2025 proved to be a difficult year for SaaS stocks, driven largely by sentiment rather than fundamentals. Concerns that artificial intelligence could disrupt traditional SaaS business models weighed on valuations, even as leading companies such as Adobe and Salesforce continued to deliver strong profitability and cash generation.

Now in 2026, the key question for the sector is whether SaaS companies can successfully monetize AI. Most providers are actively embedding AI capabilities into their platforms and rolling out new pricing tiers, usage-based models, and premium features.

From productivity software to cybersecurity and data platforms, SaaS providers continue to form the backbone of enterprise technology.

For investors, this sector offers a rare mix of long-term scalability, predictable income, and exposure to innovation.

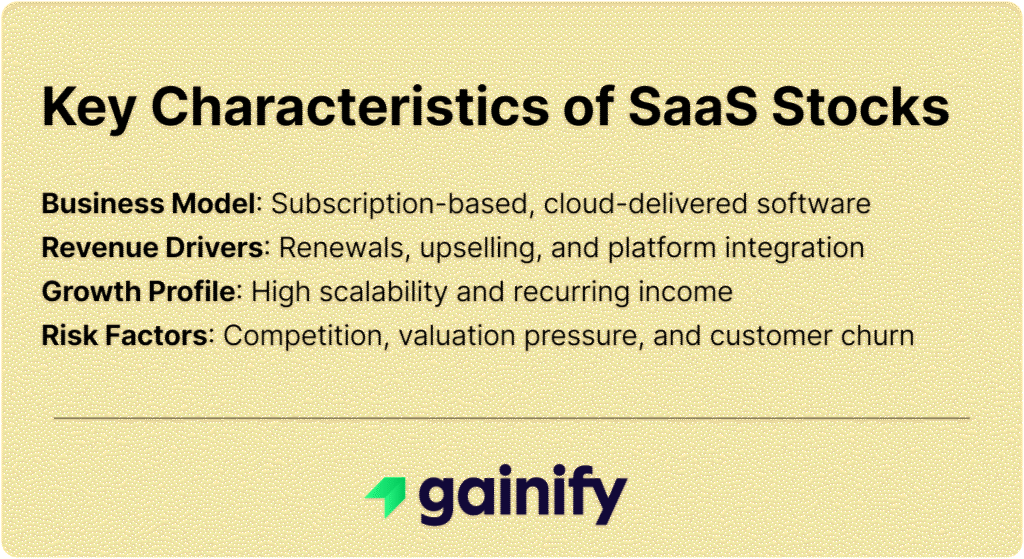

What Makes SaaS Stocks Unique

Unlike traditional software that relies on one-time license sales, SaaS companies deliver applications through the cloud and charge recurring fees, usually monthly or annually. This approach creates predictable revenue streams and deep, ongoing customer relationships.

The SaaS model is built around four key strengths:

- Recurring Revenue (ARR / MRR): steady, compounding income that supports long-term growth.

- High Margins: once the software is developed, it can scale globally at very low additional cost.

- Customer Retention: subscription models and deep integrations encourage long-term loyalty.

- Product Expansion: cloud ecosystems allow for cross-selling and upselling of new features or tiers.

Together, these factors make SaaS one of the most scalable and resilient business models in modern technology.

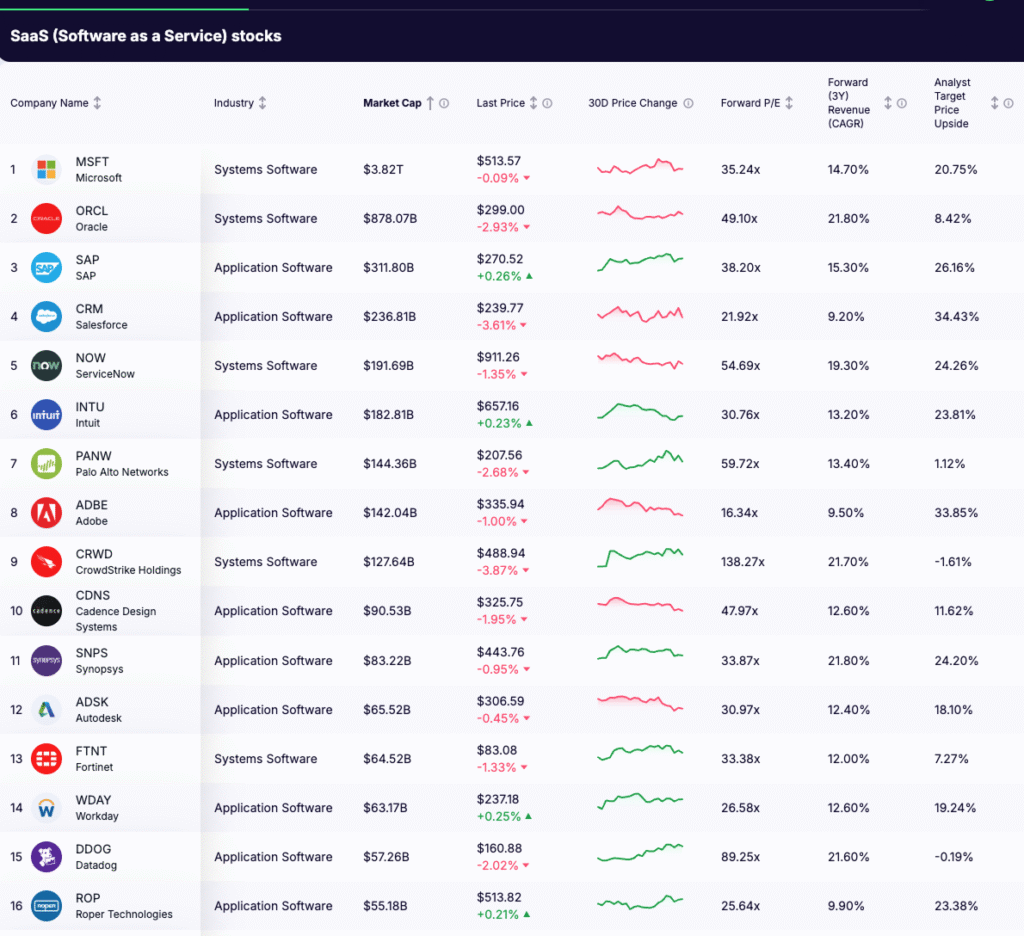

🏆 Top SaaS and Hybrid SaaS Stocks to Watch in 2026

Below are 16 leading SaaS and hybrid SaaS companies driving innovation, cloud adoption, and digital efficiency across global industries.

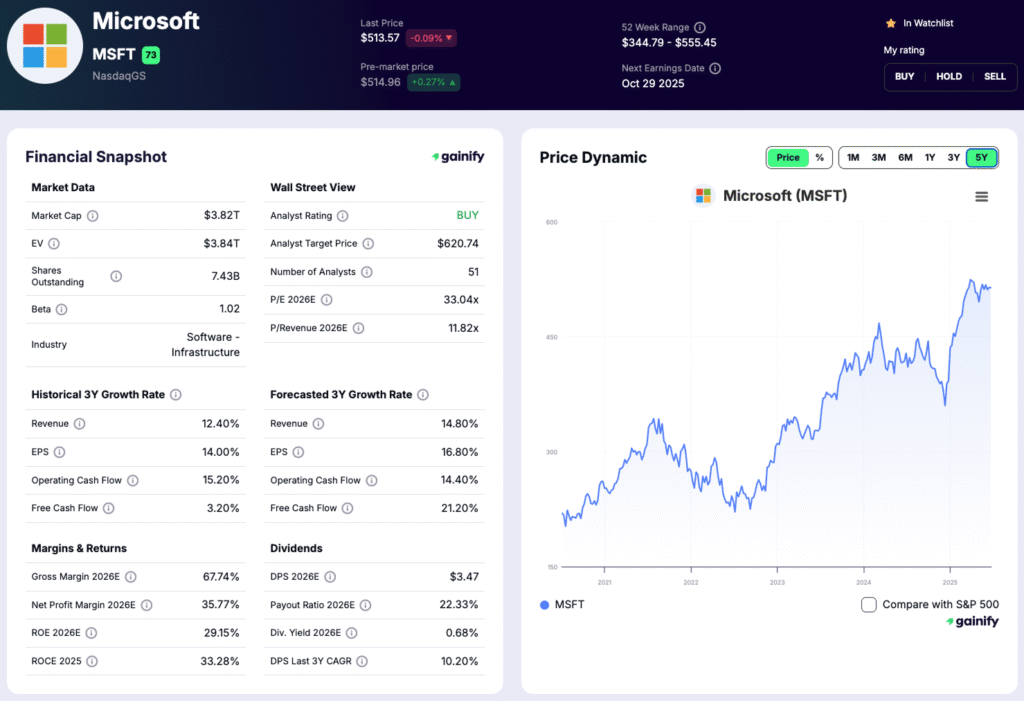

1. Microsoft (MSFT) — Hybrid SaaS

- Market Cap: $3.82T | Next 3Y CAGR: 14.7% | Analyst Upside: 20.75%

- Business Model: Microsoft (MSFT) combines cloud infrastructure (Azure) with recurring SaaS subscriptions like Microsoft 365 and Dynamics 365. AI tools such as Copilot are now integrated into its products, enhancing productivity subscriptions and stickiness.

- Why It’s Included: Microsoft is the world’s largest hybrid SaaS ecosystem, offering unmatched diversification, retention, and enterprise reach.

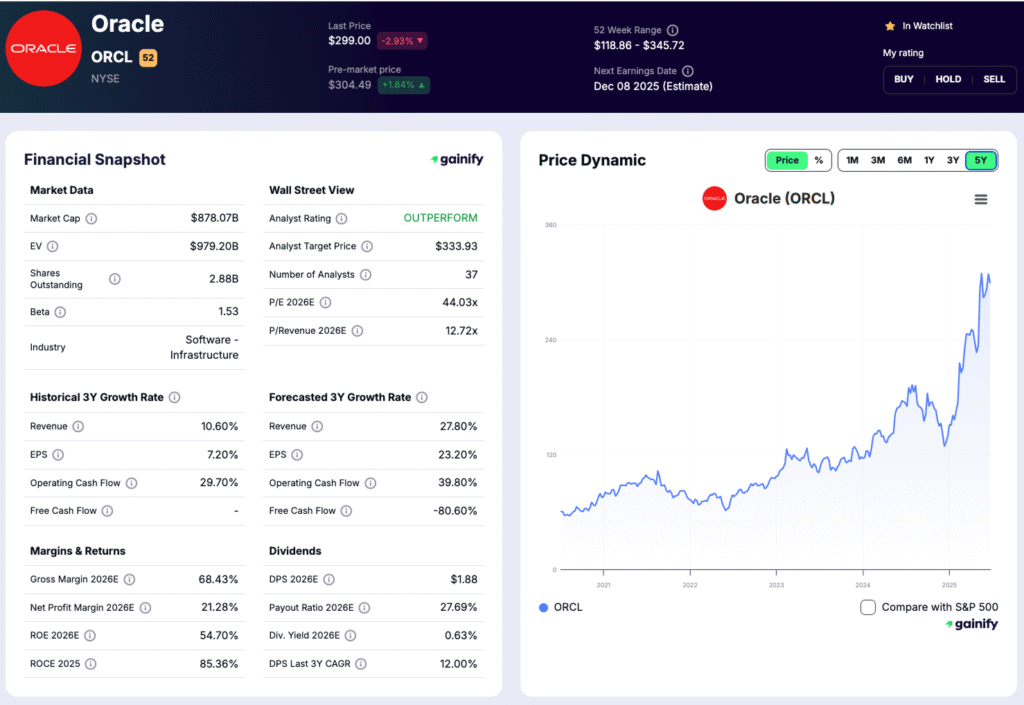

2. Oracle (ORCL) — Hybrid SaaS

- Market Cap: $878B | Next 3Y CAGR: 21.8% | Analyst Upside: 8.42%

- Business Model: Oracle (ORCL) delivers cloud-hosted enterprise software through Fusion Cloud ERP, HCM, and database services. The firm has evolved from license sales to cloud subscription billing, emphasizing long-term corporate clients.

- Why It’s Included: Its SaaS transformation is accelerating, and Oracle’s enterprise base ensures recurring, high-value contracts.

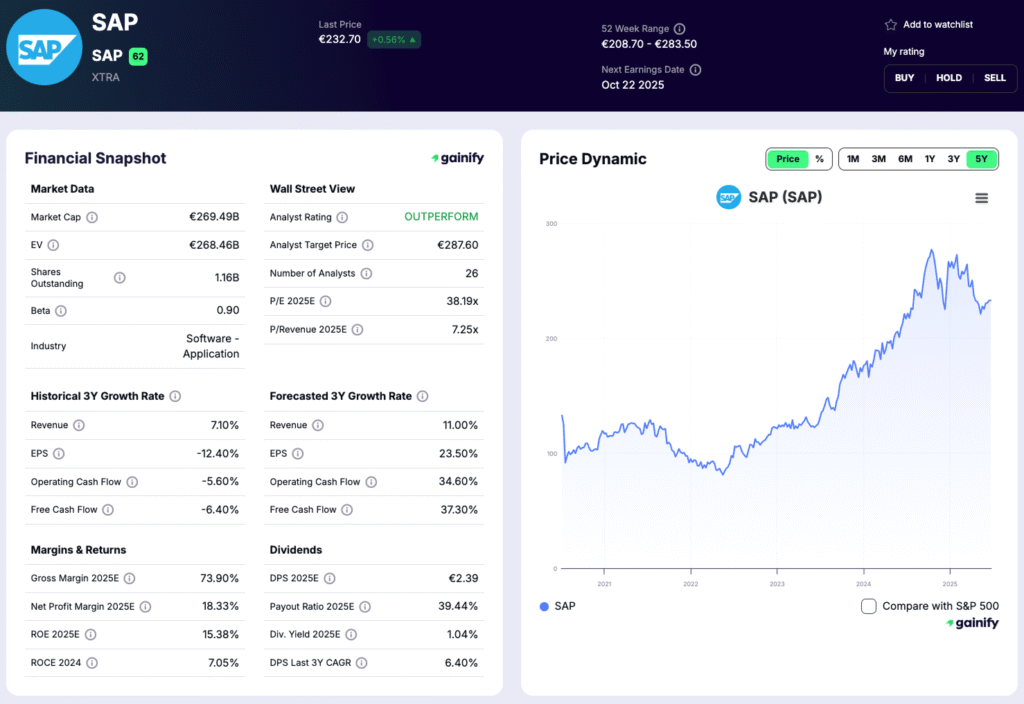

3. SAP (SAP) — Hybrid SaaS

- Market Cap: $311B | Next 3Y CAGR: 15.3% | Analyst Upside: 26.16%

- Business Model: SAP’s S/4HANA Cloud and analytics suites provide integrated SaaS tools for enterprise planning and operations. Clients subscribe to multi-year, recurring cloud service contracts.

- Why It’s Included: SAP’s global dominance in ERP and steady SaaS migration make it a key player in enterprise cloud adoption.

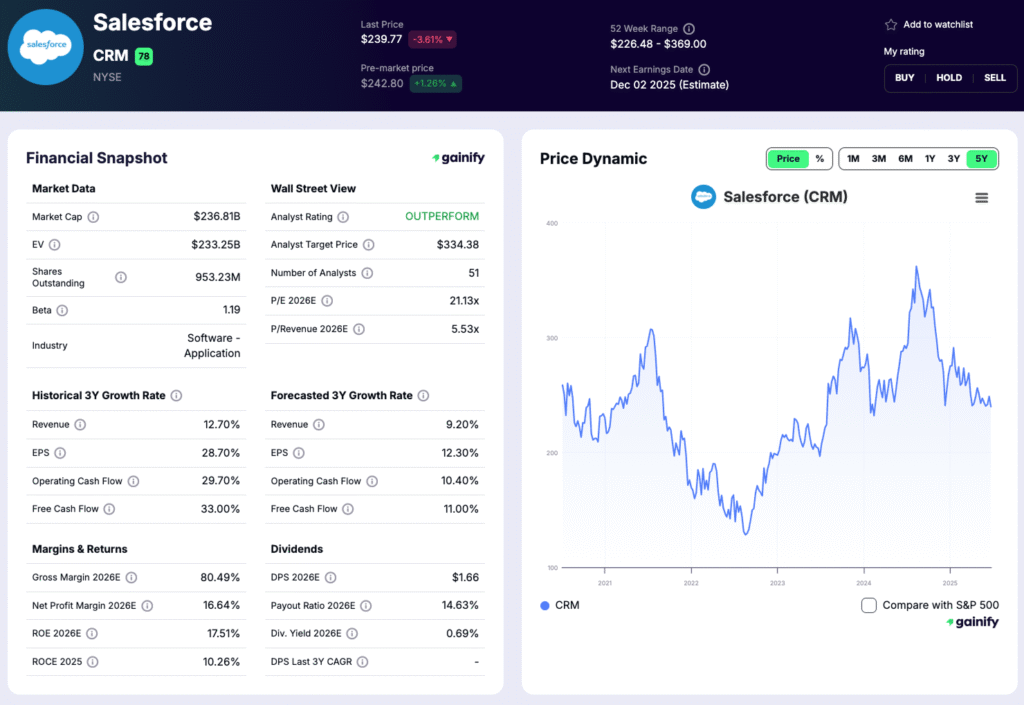

4. Salesforce (CRM) — Pure SaaS

- Market Cap: $236B | Next 3Y CAGR: 9.2% | Analyst Upside: 34.43%

- Business Model: 100% subscription-based CRM and marketing solutions, integrating customer data, automation, and AI insights via its Customer 360 platform.

- Why It’s Included: Salesforce (CRM) pioneered SaaS at scale and continues to expand margins through AI (Einstein 1) and multi-cloud integration.

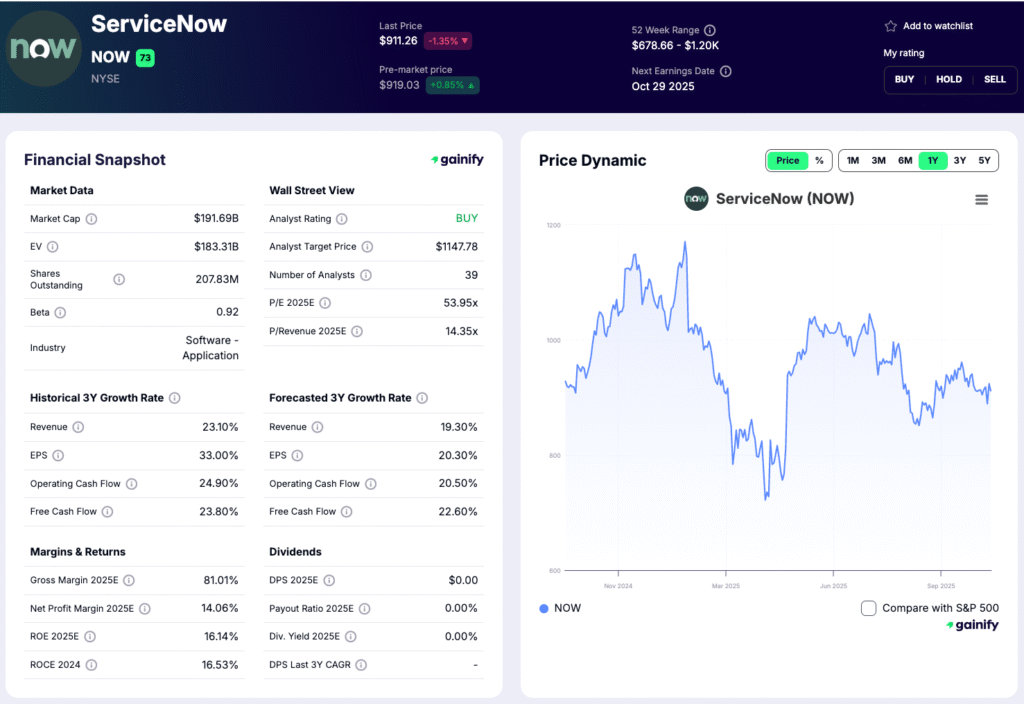

5. ServiceNow (NOW) — Pure SaaS

- Market Cap: $191B | Next 3Y CAGR: 19.3% | Analyst Upside: 24.26%

- Business Model: Provides cloud workflow and automation software through long-term enterprise subscriptions, managing IT, HR, and compliance operations.

- Why It’s Included: ServiceNow’s (NOW) high renewal rates and deep integration into enterprise processes drive sticky, recurring revenue growth.

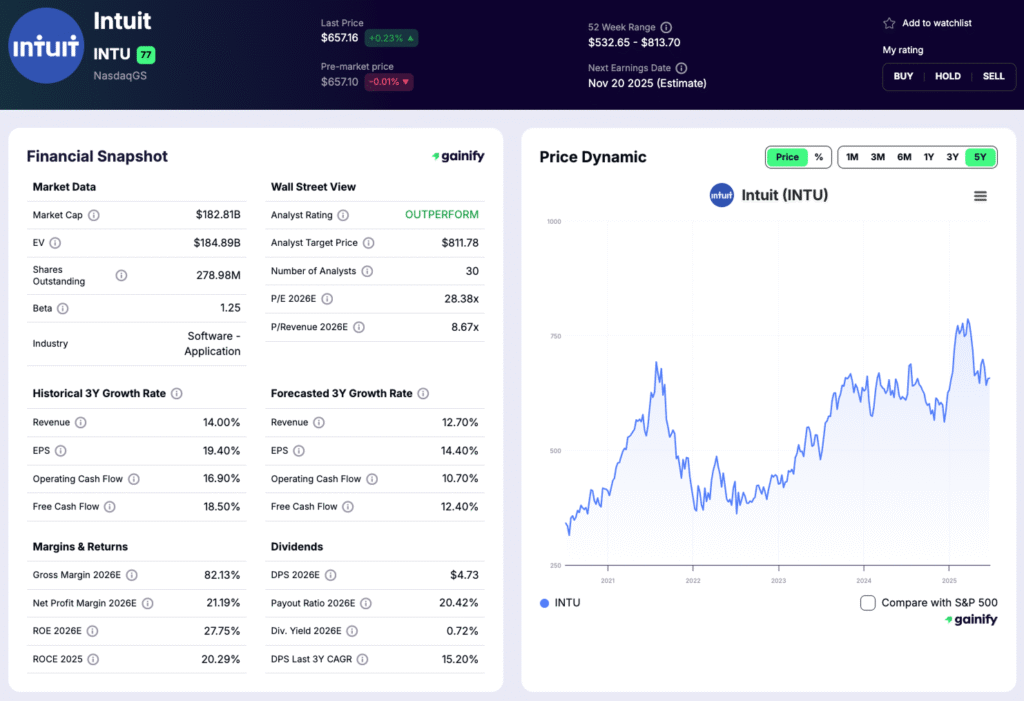

6. Intuit (INTU) — Pure SaaS

- Market Cap: $182B | Next 3Y CAGR: 13.2% | Analyst Upside: 23.81%

- Business Model: Cloud-based financial management tools like QuickBooks and TurboTax generate subscription and usage fees across small businesses and consumers.

- Why It’s Included: Intuit (INTU) blends financial automation with AI analytics, offering one of the most resilient SaaS-driven ecosystems in fintech.

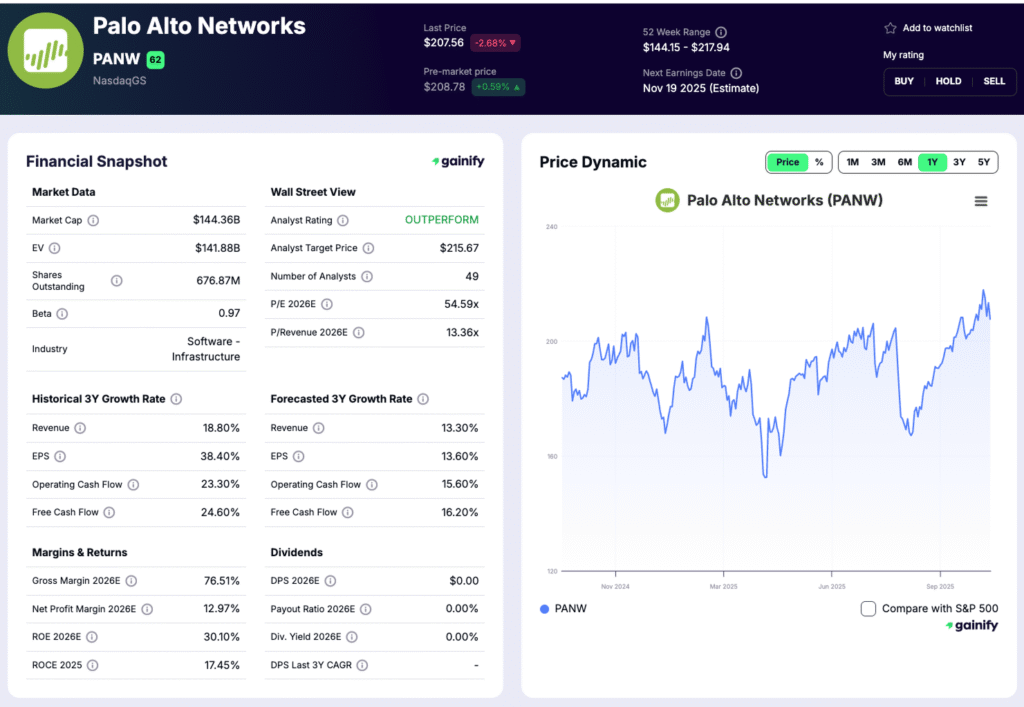

7. Palo Alto Networks (PANW) — Hybrid SaaS (Cybersecurity)

- Market Cap: $144B | Next 3Y CAGR: 13.4% | Analyst Upside: 1.12%

- Business Model: Offers cybersecurity platforms through both hardware and cloud-based subscription software. Services include threat detection and network protection as-a-service.

- Why It’s Included: A successful shift from hardware licensing to SaaS-based security subscriptions positions PANW as a key hybrid cloud player.

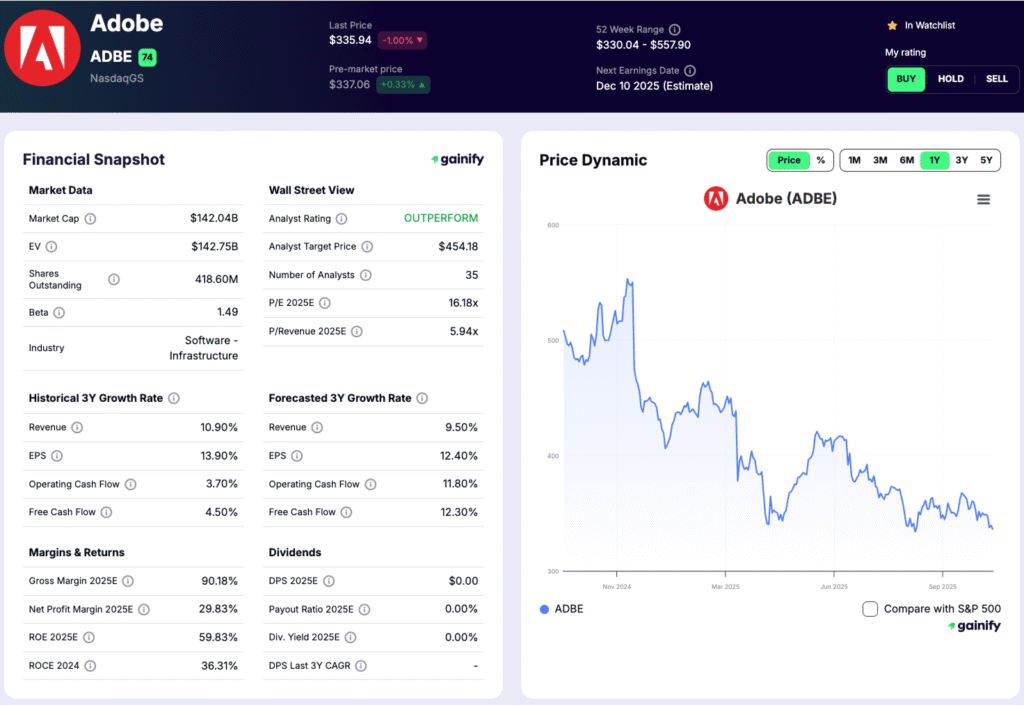

8. Adobe (ADBE) — Hybrid SaaS

- Market Cap: $142B | Next 3Y CAGR: 9.5% | Analyst Upside: 33.85%

- Business Model: Adobe’s Creative Cloud and Acrobat DC products operate on a pure subscription model, while enterprise document solutions add hybrid elements.

- Why It’s Included: Adobe’s (ADBE) SaaS pivot revolutionized creative software, with industry-leading renewal rates and pricing power.

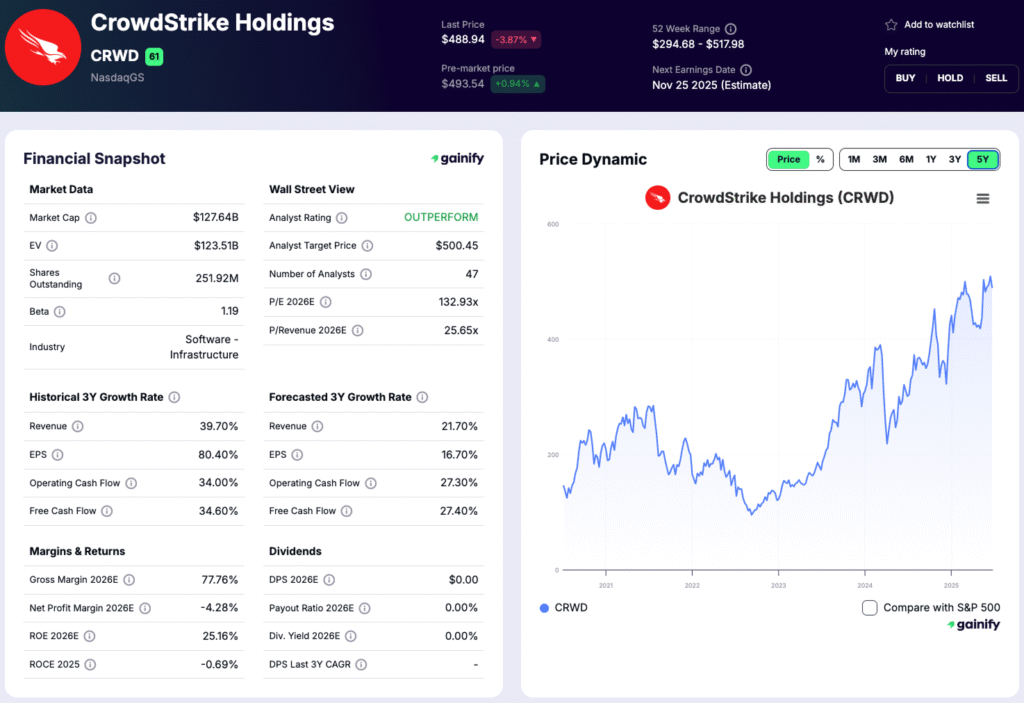

9. CrowdStrike (CRWD) — Pure SaaS (Cybersecurity)

- Market Cap: $127B | Next 3Y CAGR: 21.7% | Analyst Upside: -1.61%

- Business Model: 100% cloud-native, subscription-based security platform (Falcon) protecting endpoints using real-time AI analytics.

- Why It’s Included: Rapidly growing ARR and extremely low churn make CrowdStrike (CRWD) one of the most scalable SaaS cybersecurity models.

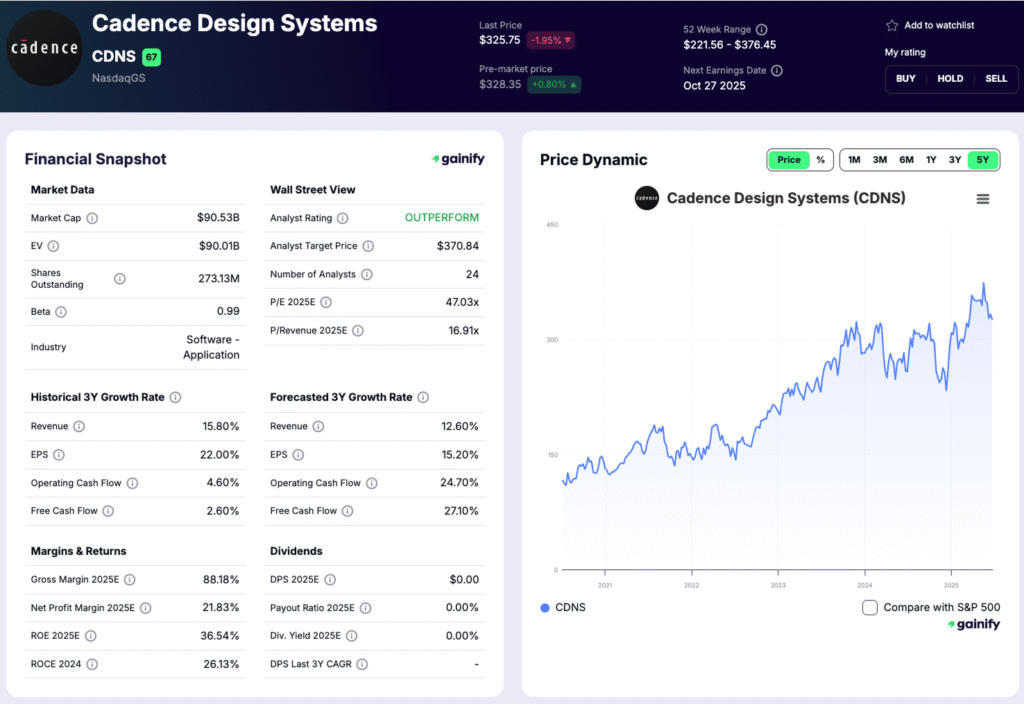

10. Cadence Design Systems (CDNS) — Hybrid SaaS

- Market Cap: $90B | Next 3Y CAGR: 12.6% | Analyst Upside: 11.62%

- Business Model: Offers EDA (Electronic Design Automation) tools primarily under subscription agreements, transitioning legacy license models into cloud-based workflows.

- Why It’s Included: Cadence (CDNS) is evolving toward a SaaS-first approach in semiconductor design, driven by recurring engineering software revenue.

11. Synopsys (SNPS) — Hybrid SaaS

- Market Cap: $83B | Next 3Y CAGR: 21.8% | Analyst Upside: 24.20%

- Business Model: Provides subscription-based chip design and IP software, combining perpetual licensing with SaaS delivery for cloud-native workflows.

- Why It’s Included: Synopsys’s (SNPS) design tools are mission-critical and increasingly consumed via recurring SaaS contracts.

12. Autodesk (ADSK) — Pure SaaS

- Market Cap: $65B | Next 3Y CAGR: 12.4% | Analyst Upside: 18.10%

- Business Model: 100% subscription-based software for engineering, architecture, and design professionals (AutoCAD, Revit, Fusion 360).

- Why It’s Included: Autodesk (ADSK) was an early leader in transitioning creative and industrial design tools to SaaS, offering strong recurring margins.

13. Fortinet (FTNT) — Hybrid SaaS (Security)

- Market Cap: $64B | Next 3Y CAGR: 12.0% | Analyst Upside: 7.27%

- Business Model: Combines physical firewalls with cloud-based security subscriptions, providing ongoing updates and threat intelligence.

- Why It’s Included: Fortinet’s (FTNT) SaaS revenue from security services now outpaces hardware, signaling a mature hybrid transition.

14. Workday (WDAY) — Pure SaaS

- Market Cap: $63B | Next 3Y CAGR: 12.6% | Analyst Upside: 19.24%

- Business Model: Delivers cloud-native HR, payroll, and finance software entirely through subscription-based access for enterprises.

- Why It’s Included: Workday’s deep integration across HR and finance workflows gives it one of the stickiest pure SaaS revenue bases.

15. Datadog (DDOG) — Pure SaaS

- Market Cap: $57B | Next 3Y CAGR: 21.6% | Analyst Upside: -0.19%

- Business Model: Provides cloud observability and analytics software under a usage-based SaaS model, scaling with client data activity.

- Why It’s Included: Datadog (DDOG) is one of the fastest-growing pure SaaS firms, benefiting from explosive cloud adoption and DevOps spending.

16. Roper Technologies (ROP) — Hybrid SaaS

- Market Cap: $55B | Next 3Y CAGR: 9.9% | Analyst Upside: 23.38%

- Business Model: Operates a portfolio of vertical-market software businesses, many shifting to cloud subscription models in healthcare and industrial analytics.

- Why It’s Included: Roper’s (ROP) diversified hybrid SaaS portfolio delivers steady, recurring income with strong cash generation.

Final Thoughts

SaaS stocks remain a cornerstone of technology investing—offering the rare combination of recurring revenue, scalability, and continuous innovation.

- Stable Compounders: Microsoft, Adobe, SAP, Oracle

Proven enterprise leaders with durable cash flows and strong pricing power. - High-Growth Innovators: Datadog, ServiceNow, CrowdStrike, Workday

Cloud-native disruptors driving the next wave of digital transformation through rapid adoption and product innovation. - Balanced Leaders: Salesforce, Palo Alto Networks, Intuit

Well-established platforms blending steady profitability with ongoing growth opportunities.

A thoughtfully diversified SaaS portfolio captures the resilience of mature enterprise platforms alongside the expansion potential of next-generation cloud innovators, positioning investors to benefit from the long-term evolution of software delivery.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always perform independent research or consult a licensed financial advisor before investing.