George Soros has spent more than half a century redefining what it means to be a macro investor. Unlike managers whose reputations are built on compounding through duration, Soros built his legacy by acting decisively at inflection points, sizing positions aggressively when probability skewed in his favor, and stepping aside just as quickly when reflexive dynamics began to reverse.

His most famous insight — “markets are always wrong” — is not a dismissal of prices, but a framework. Soros believes that prices shape fundamentals just as much as fundamentals shape prices. That feedback loop, which he formalized as reflexivity, remains the intellectual backbone of Soros Fund Management today.

Q4 2025 is a clear example of that philosophy in motion. The portfolio does not read like a directional bet on growth, rates, or geopolitics. Instead, it reflects adaptive positioning: selective exposure to large-cap platforms, tactical use of ETFs and options, decisive exits where reflexive upside has played out, and constant recalibration of risk.

As of 31st Dec, 2025, Soros Fund Management reported approximately $8.63 billion in public equity holdings, spread across 244 positions, with an average holding period of just three quarters, marking the largest disclosed equity portfolio in the firm’s recent history. That turnover alone tells a story. This is not a portfolio designed to sit still.

Key Insights from George Soros’ Q4 2025 Portfolio Update

- Record Scale: Public equity holdings reached $8.63 billion as of the December 31, 2025 filing, the largest portfolio size on record for Soros Fund Management.

- High Rotation, Low Commitment: With 244 positions and an average holding period of about three quarters, the portfolio emphasizes rapid capital recycling over long-term holding.

- Conviction vs. Tactics: Core large-cap equities remained stable, while most activity occurred in ETFs and options, allowing macro views to shift without disrupting structural positions.

- Derivatives-Centric Positioning: Index, sector, and regional ETFs were important tools for managing risk, convexity, and conditional exposure.

- Reflexivity Applied: Capital was actively reallocated as narratives evolved. Positions were sized to matter, but none were treated as permanent, reinforcing adaptability as the defining edge.

Soros’ Investment Style: Conviction Without Attachment

George Soros has never fit the mold of a traditional long-term investor. He is not guided by loyalty to positions, narratives, or even his own past convictions. What defines Soros is detachment. The ability to commit aggressively when the odds tilt in his favor, and to exit just as quickly when they do not.

His most famous trades were never built on certainty. They were built on asymmetry.

Breaking the Bank of England

The moment that cemented Soros’ reputation came in 1992, during the collapse of the British pound. At the time, the United Kingdom was part of the European Exchange Rate Mechanism, a system that forced the pound to trade within a fixed band against other European currencies. The framework looked stable on paper. In reality, it was fragile.

Soros identified the contradiction early. The British economy was weak. Interest rates were painfully high. Defending the currency peg required political will and economic sacrifice that could not last. The longer the Bank of England fought the market, the more pressure built.

Soros did not ask whether the pound was undervalued or overvalued. He asked a more important question.

What happens if this breaks?

The answer was clear. If the peg survived, losses were limited. If it failed, the upside was enormous. That imbalance mattered more than being “right.”

As pressure mounted, Soros increased his short position. When the UK government finally abandoned the peg, the pound collapsed. Soros reportedly made more than one billion dollars in a single day, while the Bank of England was forced to withdraw from the ERM. The trade worked not because Soros predicted the future, but because market pressure itself accelerated the outcome.

It was reflexivity in action.

A Philosophy Built on Risk, Not Certainty

That episode did more than define Soros’ public image. It defined his approach to risk.

As Soros famously said: “It’s not whether you’re right or wrong, but how much money you make when you’re right and how much you lose when you’re wrong.”

This philosophy explains why Soros portfolios often look complex at first glance. They are not designed for elegance. They are designed for adaptability.

ETFs sit alongside individual stocks. Options coexist with outright equity positions. Long exposures appear next to hedges that seem to contradict them. Positions are layered, resized, reduced, and sometimes eliminated entirely within a single quarter.

Soros believes markets are reflexive rather than efficient. Prices shape behavior. Behavior reshapes fundamentals. Those fundamentals then feed back into prices. Because of this loop, conviction must always remain conditional.

When the feedback loop strengthens, Soros presses. When it weakens, he steps away without hesitation.

George Soros’ Role Today

George Soros is no longer involved in day-to-day trading, but his influence remains central. Soros Fund Management has operated as a family office since 2011, with portfolio execution led by a professional investment team under CEO and CIO Dawn Fitzpatrick.

Soros now plays a strategic and philosophical role. He helps shape how risk is framed, how reflexivity is applied, and how capital is structured, rather than making individual trade decisions. The emphasis on flexibility, use of ETFs and derivatives, and rapid position changes all reflect his enduring framework.

Q4 2025 fits this model well. The portfolio is not driven by a single macro call, but by a system built on Soros’ ideas and executed by a modern investment team.

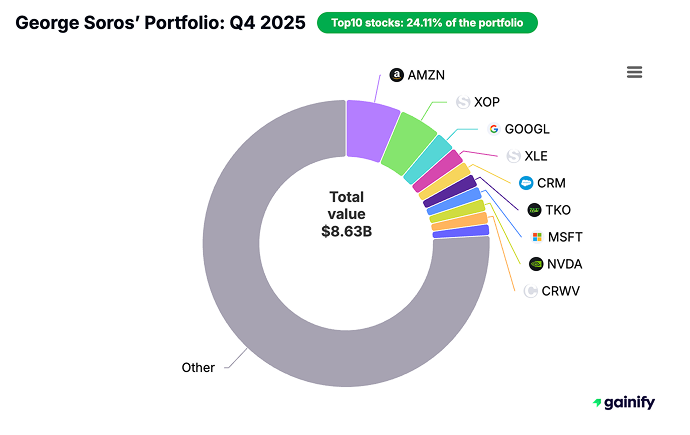

Portfolio Overview: Q4 2025

As of December 31, 2025, based on the SEC 13F filed on February 13, 2026, George Soros’s public equity portfolio reflects a clear shift from Q3 2025 in both scale and structure.

- Portfolio value: $8.63B

- Number of holdings: 244

- Average holding period: ~3 quarters

- Top 10 holdings: ~24.1% of total portfolio value

Compared with Q3 2025, total portfolio value increased materially (from ~$7.0B), while the number of positions also rose, reinforcing Soros Fund Management’s preference for breadth with tactical flexibility rather than concentration.

The Big Picture in Q4 2025: What Changed vs. Q3

The defining change from Q3 to Q4 2025 was an acceleration in capital rotation. In Q4, that calibration turned into active re-risking and rebalancing at scale, supported by a larger capital base. Net exposure was reshaped rather than simply increased. Capital was recycled aggressively across equities, ETFs, and options to reflect updated reflexive signals.

Three changes stand out relative to Q3:

- Record portfolio size paired with faster turnover. The portfolio reached a new high in disclosed value while the average holding period shortened. This combination signals confidence in near-term opportunity density alongside a clear willingness to exit positions quickly when narratives weaken or feedback loops shift.

- Greater reliance on ETFs and derivatives as primary tools. Broad market, sector, and regional ETFs, often combined with options, became more central to portfolio construction. These instruments were used to express conditional views, manage convexity, and adjust exposure efficiently rather than serve as passive allocations.

- Clear separation between conviction and tactics. Core equity positions remained relatively stable, while most capital movement occurred in tactical vehicles. This structure allows macro views to evolve without disrupting longer-term equity holdings, preserving strategic exposure while maintaining flexibility.

As a result, capital above meaningful size thresholds remained concentrated in a relatively small group of positions, while the long tail of the portfolio functioned as a source of optionality, hedging capacity, and tactical responsiveness.

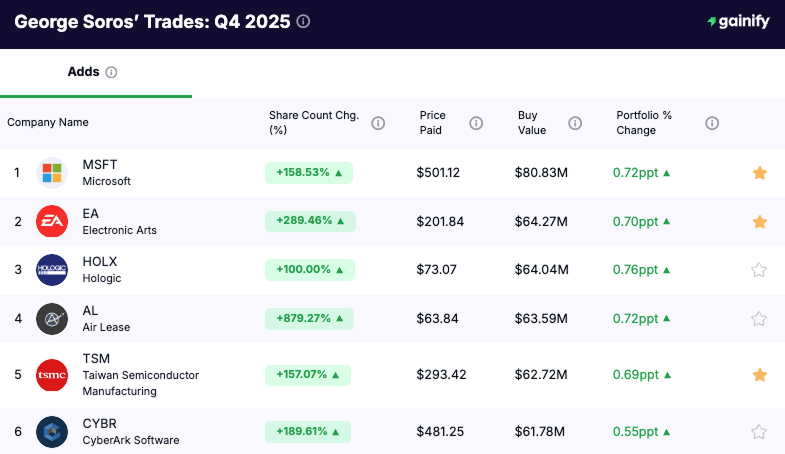

Soros Fund: Concentrated Additions in Q4 2025

The most consequential activity in Q4 2025 came from decisive increases in a focused group of equities. These additions were not incremental adjustments. They materially expanded exposure and signal where conviction strengthened as the portfolio reached a record asset base.

Microsoft (NASDAQ: MSFT)

Share count change: +158.53%

Capital deployed: $80.8 million

Microsoft was one of the most significant increases of the quarter. The size of the addition reflects conviction in durable enterprise software economics, AI integration across the product stack, and recurring cloud revenue streams. The increase lifts exposure to large-cap technology without relying on speculative positioning.

Electronic Arts (NASDAQ: EA)

Share count change: +289.46%

Capital deployed: $64.3 million

Electronic Arts was expanded aggressively. The scale of the increase suggests confidence in recurring digital monetization, franchise durability, and margin stability within interactive entertainment. The position size indicates a targeted allocation rather than a tactical trade.

Hologic (NASDAQ: HOLX)

Share count change: +100.00%

Capital deployed: $64.0 million

Hologic was doubled during the quarter. The addition points to confidence in defensive healthcare cash flows and earnings visibility. The sizing increases exposure to medical technology without introducing outsized cyclicality.

Air Lease (NYSE: AL)

Share count change: +879.27%

Capital deployed: $63.6 million

Air Lease saw the most dramatic percentage increase. The move represents a high-conviction expansion tied to aircraft leasing economics and global travel normalization. The scale of the adjustment signals a willingness to lean into cyclical recovery when valuation remains attractive.

Taiwan Semiconductor (NYSE: TSM)

Share count change: +157.07%

Capital deployed: $62.7 million

TSM was increased meaningfully, reinforcing exposure to semiconductor manufacturing capacity at the center of global AI and compute demand. The addition complements large-cap software exposure by strengthening the supply-side component of the technology stack.

Taken together, Q4 2025 additions show a clear pattern. Soros Fund Management increased exposure selectively in large-cap technology, semiconductors, healthcare, cybersecurity, and cyclical aviation leasing. The moves were concentrated, capital-intensive, and deliberate, signaling a controlled re-risking within defined areas of conviction.

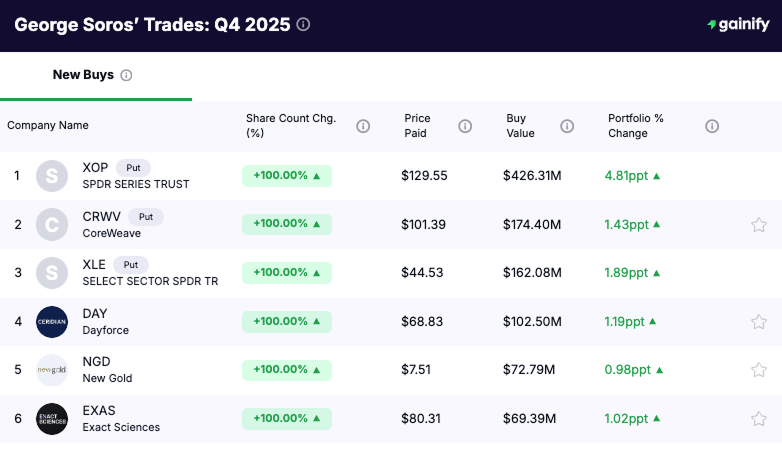

Soros Fund: New Buys in Q4 2025

New positions initiated in Q4 2025 were deliberately sized and structurally differentiated, combining outright equity exposure with sizable derivative positions. The defining feature of this cohort is not exploration, but gross exposure management. Several of the largest “new buys” were established via put options, allowing Soros Fund Management to express macro and sector views with strictly defined downside.

SPDR Oil & Gas Exploration ETF (XOP) – Put Options

Share count change: +100%

Gross exposure deployed: $426.3 million

XOP puts were the largest new position of the quarter by capital. The size indicates a high-conviction bearish or hedging stance on energy equities, implemented through options rather than direct short exposure. This structure maximizes payoff asymmetry while capping downside risk.

CoreWeave (CRWV) – Put Options

Share count change: +100%

Gross exposure deployed: $174.4 million

The CRWV put position reflects skepticism toward AI infrastructure valuation or financing dynamics. Using puts allows participation in downside scenarios without long equity exposure to an early-stage, capital-intensive business model.

Energy Select Sector SPDR (XLE) – Put Options

Share count change: +100%

Gross exposure deployed: $162.1 million

XLE puts complement the XOP position by targeting the broader energy complex. Together, these trades represent a coordinated sector-level expression, suggesting concern around energy pricing, margins, or macro sensitivity rather than idiosyncratic company risk.

Taken together, the three put positions account for over $760 million in gross exposure, underscoring how derivatives were used as primary instruments for macro positioning rather than marginal hedges.

Dayforce (NYSE: DAY)

Share count change: +100%

Capital deployed: $102.5 million

Dayforce was added as a meaningful equity position, indicating confidence in enterprise software demand, payroll infrastructure stickiness, and recurring revenue visibility. The position size places it firmly within the active risk bucket.

New Gold (NYSE: NGD)

Share count change: +100%

Capital deployed: $72.8 million

New Gold introduces direct exposure to precious metals. This position likely functions as a macro hedge against monetary instability or geopolitical risk, contrasting with the energy-sector downside expressed through puts.

Exact Sciences (NASDAQ: EXAS)

Share count change: +100%

Capital deployed: $69.4 million

Exact Sciences was initiated as a healthcare growth position, reflecting confidence in diagnostics demand and long-term testing adoption. The sizing suggests conviction without overconcentration.

What New Buys Signal in Q4 2025

The Q4 2025 new buys show a clear separation between gross exposure and net risk. Large notional positions were established through put options to express macro and sector views with defined downside, while equity capital was deployed selectively into software, healthcare, and gold-related assets.

This mix highlights a core Soros principle in practice: use derivatives to shape macro exposure and convexity, while reserving equity ownership for businesses with identifiable cash flow and structural durability.

Soros Fund: Cuts in Q4 2025

Cuts in Q4 2025 were targeted, high-impact reductions, focused on positions where upside had compressed or where exposure no longer justified its capital footprint. Each reduction materially altered portfolio composition and reflects Soros Fund Management’s discipline in withdrawing capital once feedback loops weaken.

Smurfit Westrock (NYSE: SW)

Share count change: -68.99%

Capital reduced: $203.8 million

Smurfit Westrock was the largest cut of the quarter by portfolio impact. The scale of the reduction signals that the original consolidation and pricing thesis had largely played out. With valuation reflecting integration benefits and cost synergies, expected reflexive upside diminished, prompting a decisive de-risking.

Invesco S&P Equal Weight ETF (RSP)

Share count change: -87.46%

Capital reduced: $137.7 million

RSP was trimmed aggressively after having served its purpose as a breadth-based exposure. The reduction suggests that the anticipated broadening of market leadership either materialized or lost convexity, making the risk-reward less attractive relative to other macro instruments.

Flutter Entertainment (NYSE: FLUT)

Share count change: -81.04%

Capital reduced: $89.4 million

Flutter was reduced sharply as regulatory complexity, execution risk, and competitive intensity became more fully reflected in price. The cut indicates tighter control over consumer discretionary exposure where narrative-driven upside had matured.

Interactive Brokers Group (NASDAQ: IBKR)

Share count change: -51.30%

Capital reduced: $54.4 million

IBKR was trimmed rather than exited, reflecting a recalibration rather than a loss of conviction. As interest-rate tailwinds and trading activity normalized, the position size was adjusted to reflect lower marginal upside while retaining core exposure.

What These Cuts Signal

Across these four positions, the common thread is capital discipline. Exposure was reduced where valuation, consensus, or macro conditions compressed future returns. The moves reinforce a central Soros principle: capital is allocated dynamically, and positions are reduced decisively once reflexive advantages fade, regardless of prior success.

Soros Fund: Sold Outs in Q4 2025

Q4 2025 featured complete exits from multiple equity and options positions, marking a deliberate capital reset rather than incremental trimming. These sold outs removed defined-risk macro structures and individual equity exposure, freeing capital for redeployment and reducing gross derivative exposure.

Wolfspeed (NYSE: WOLF) – Put Options

Share count change: -100%

Capital exited: $134.6 million

The full exit from Wolfspeed put options eliminated a defined-risk bearish expression on semiconductor cyclicality. The position had offered convex downside participation; its removal signals either payoff realization or reduced confidence in further asymmetry.

iShares China Large-Cap ETF (FXI) – Call Options

Share count change: -100%

Capital exited: $128.0 million

FXI call exposure was fully closed, removing leveraged upside to Chinese large-cap equities. This suggests a reassessment of near-term policy-driven catalysts or a decision to avoid concentrated directional risk in China through options.

KraneShares CSI China Internet ETF (KWEB) – Call Options

Share count change: -100%

Capital exited: $92.3 million

KWEB calls were eliminated entirely, further reducing exposure to Chinese technology momentum. The combined FXI and KWEB exits represent a meaningful unwind of China-focused convex positioning.

iShares 20+ Year Treasury ETF (TLT) – Call Options

Share count change: -100%

Capital exited: $89.4 million

TLT call options were fully closed, removing rate-sensitive upside exposure. This materially reduced duration convexity and suggests shifting expectations around long-term yield dynamics.

Aramark (NYSE: ARMK)

Share count change: -100%

Capital exited: $86.6 million

Aramark was exited outright, eliminating direct equity exposure to food services and facilities management. The move reflects capital reallocation rather than portfolio rebalancing.

What These Sold Outs Signal

The defining characteristic of Q4 sold outs is the sharp reduction in gross options exposure, particularly across China equities and long-duration Treasuries. Soros Fund Management removed multiple convex macro expressions simultaneously, simplifying the portfolio and lowering derivative-driven sensitivity.

This was not passive portfolio drift. It was active capital recycling. Tactical instruments were closed decisively once their risk-reward shifted, reinforcing the fund’s emphasis on flexibility over attachment.

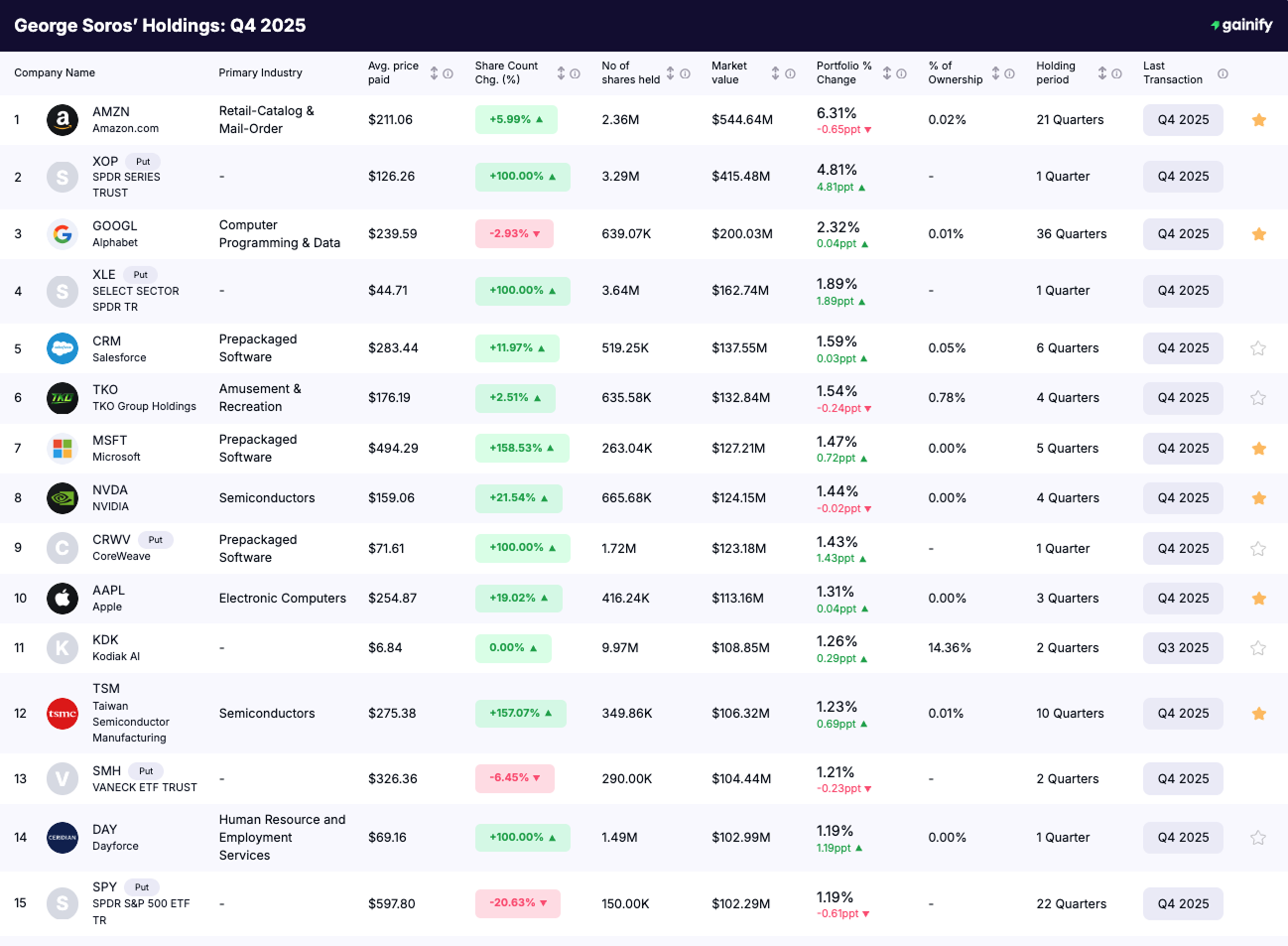

George Soros: Top 15 Portfolio Holdings as of December 31, 2025

The Q4 2025 disclosure shows Soros Fund Management operating at record scale with an emphasis on flexibility rather than concentration. While individual positions remain relatively modest in size, capital is actively allocated across equities, ETFs, and derivatives, with options frequently ranking among the fund’s largest exposures. The structure highlights a portfolio built to adapt quickly, separating long-term equity holdings from tactical instruments used to shape risk and express conditional views.

Rank | Company / Instrument | Ticker | Market Value | Portfolio Weight | Share Count Change | Holding Period |

|---|---|---|---|---|---|---|

1 | Amazon.com | AMZN | $544.64M | 6.31% | +5.99% | 21 Quarters |

2 | SPDR Series Trust (Put) | XOP | $415.48M | 4.81% | +100.00% | 1 Quarter |

3 | Alphabet | GOOGL | $200.03M | 2.32% | −2.93% | 36 Quarters |

4 | Select Sector SPDR (Put) | XLE | $162.74M | 1.89% | +100.00% | 1 Quarter |

5 | Salesforce | CRM | $137.55M | 1.59% | +11.97% | 6 Quarters |

6 | TKO Group Holdings | TKO | $132.84M | 1.54% | +2.51% | 4 Quarters |

7 | Microsoft | MSFT | $127.21M | 1.47% | +158.53% | 5 Quarters |

8 | NVIDIA | NVDA | $124.15M | 1.44% | +21.54% | 4 Quarters |

9 | CoreWeave (Put) | CRWV | $123.18M | 1.43% | +100.00% | 1 Quarter |

10 | Apple | AAPL | $113.16M | 1.31% | +19.02% | 3 Quarters |

11 | Kodiak AI | KDK | $108.85M | 1.26% | 0.00% | 2 Quarters |

12 | Taiwan Semiconductor | TSM | $106.32M | 1.23% | +157.07% | 10 Quarters |

13 | VanEck Semiconductor ETF (Put) | SMH | $104.44M | 1.21% | -6.45% | 2 Quarters |

14 | Dayforce | DAY | $102.99M | 1.19% | +100.00% | 1 Quarter |

15 | SPDR S&P 500 ETF (Put) | SPY | $102.29M | 1.19% | -20.63% | 22 Quarters |

Conclusion: Reflexivity in Practice

The George Soros portfolio in Q4 2025 is best understood not as a static collection of stocks, but as a living expression of reflexivity and risk control. The quarter was defined by movement, structure, and intent. Capital flowed decisively toward positions where upside remained asymmetric and was withdrawn just as forcefully where narratives had matured or payoff dynamics narrowed.

At the top of the portfolio, Amazon’s rise to the largest position reflects conviction in durable platforms with embedded optionality. At the same time, the heavy use of ETFs and options shows that exposure was not taken blindly. Market breadth was expressed through equal-weight indices, macro views through rate-sensitive and index derivatives, and regional exposure through defined-risk structures rather than permanent commitments.

Technology remains core, but not concentrated. AI exposure is spread across platforms, infrastructure, and sector-level instruments, avoiding dependence on any single outcome. China exposure reappears, but only through options. Downside protection is adjusted, not abandoned. This is positioning designed to evolve, not to sit still.

Most importantly, Q4 2025 reinforces a principle that has defined Soros’ investing for decades: conviction without attachment. Positions are sized to matter, but none are sacred. When reflexive feedback loops strengthen, capital is added. When they weaken, capital is removed. The result is a portfolio built not to predict the future, but to adapt to it.