Chris Hohn’s portfolio, as reported in TCI Fund Management’s (TCI) SEC Form 13F filing for December 31, 2025, represents one of the most concentrated and highest-performing equity strategies in global hedge fund history. After generating an estimated $18.9 billion in net gains in 2025, the largest single-year profit ever recorded by a hedge fund according to Edmond de Rothschild’s annual rankings, TCI closed the year with $53.7 billion allocated across just nine U.S.-listed companies. This is not a diversified hedge fund model. It is a conviction-driven capital allocation strategy centered on financial infrastructure, industrial restructuring, and enterprise software platforms with durable pricing power and recurring revenue.

Chris Hohn built TCI on activist discipline and high-conviction ownership. The fund does not pursue broad diversification. It allocates capital where governance influence, operational improvement, and capital allocation reform can materially increase shareholder value. Each position is sized to have a measurable impact on overall returns rather than serve as incremental exposure.

As of Q4 2025, the top five holdings represent more than 80% of total equity capital. General Electric accounts for over 27% alone, making it one of the largest single-stock allocations among major global hedge funds. The rest of the portfolio is centered on financial infrastructure leaders such as Visa, Moody’s, and S&P Global, alongside Microsoft as the primary technology exposure. These businesses share characteristics that align with TCI’s framework: recurring revenue, global scale, and strong returns on capital.

In the sections ahead, this article examines Chris Hohn’s activist framework, details TCI’s Q4 2025 portfolio positioning, and analyzes how this high-conviction structure shapes the fund’s outlook for 2026.

Chris Hohn Portfolio in 60 Seconds

- Record year: $18.9B in net gains, the strongest annual result in hedge fund history.

- Extreme concentration: 9 stocks total; top five exceed 80% of portfolio value.

- General Electric dominance: GE represents over 27% of total capital, one of the largest single-stock allocations among major hedge funds.

- Financial infrastructure focus: Visa, Moody’s, and S&P Global form a core pillar alongside Microsoft as the primary technology holding.

Who Is Chris Hohn

Chris Hohn is one of the most powerful activist investors of his generation. He founded The Children’s Investment Fund Management (TCI) in 2003, building it into one of the world’s most concentrated and influential hedge funds. From the start, TCI distinguished itself with a combination of deep value investing and aggressive shareholder activism. The fund became known for demanding accountability from corporate boards, pressing for operational efficiency, and driving capital allocation reforms. Hohn’s reputation as an uncompromising negotiator in boardrooms earned him the label of “the world’s most feared activist investor” from The Telegraph.

Born in 1966 in Surrey, England, Hohn studied accounting and business economics at the University of Southampton, graduating at the top of his class. He later attended Harvard Business School, where he earned his MBA and graduated as a Baker Scholar, the highest academic distinction awarded to the top 5% of the class. His early career included a stint at private equity firm Apax Partners and later at Perry Capital, where he refined the activist investment approach that would define his career.

Since its founding, TCI has delivered long-term compound annual returns in the mid-teens, cementing its place among the most successful hedge funds globally. Unlike funds that hold hundreds of positions, TCI typically runs fewer than 15, with outsized allocations to companies Hohn believes are undervalued but capable of structural improvement. His campaigns have targeted major corporations across industries, including ABN Amro, Deutsche Börse, Canadian National Railway, Alphabet, and General Electric. Many of these campaigns resulted in sweeping changes to corporate governance, capital deployment, and long-term strategy.

Beyond the markets, Hohn has established himself as a leading philanthropist. He founded the Children’s Investment Fund Foundation (CIFF) in 2002, which today is one of the largest charitable foundations in Europe. CIFF focuses on children’s health, nutrition, education, and climate change, with Hohn personally committing at least $5 billion to philanthropic causes over his lifetime. His environmental advocacy has also extended to his role as a financier, where he has pressed companies to adopt stronger climate disclosures and supported shareholder campaigns tied to sustainability.

Chris Hohn’s Investment Philosophy

Chris Hohn’s investment philosophy is built on concentrated ownership, activist engagement, and long-term value creation. Since founding TCI Fund Management in 2003, Hohn has structured the firm around the belief that meaningful ownership stakes combined with active oversight generate superior returns. This approach is explored in The Biography of Chris Hohn: Funding Change — The Financial Architect of Global Philanthropy, which describes how his investment model combines financial discipline with long-term strategic influence.

At the center of Hohn’s philosophy is the idea that ownership scale creates leverage. TCI does not diversify across dozens of small positions. It builds large stakes in a limited number of companies where governance engagement, capital allocation discipline, and operational improvements can materially affect intrinsic value. Influence is part of the return strategy.

Core characteristics of Hohn’s approach include.

✓ Concentrated positions: TCI typically holds around 9–12 stocks. Each position is sized to meaningfully impact overall fund performance rather than serve as incremental exposure.

✓ Activist discipline: Hohn engages directly with boards and management teams to improve strategy, cost structure, governance, and capital allocation. His campaigns at companies such as General Electric and major rail operators demonstrate this hands-on model.

✓ Focus on structurally advantaged industries: The portfolio leans toward financial infrastructure, credit rating agencies, payments networks, and regulated assets. These industries benefit from high barriers to entry, recurring revenue, and durable pricing power.

✓ Selective technology exposure: TCI prefers enterprise platforms with proven economics and scale, such as Microsoft, over speculative or narrative-driven growth.

✓ Patience as a competitive advantage: Positions are often held for many years. The goal is to capture operational improvement and earnings compounding rather than short-term valuation shifts.

As described in biographical accounts of Hohn’s career, his strategy reflects a belief that disciplined capital allocation and shareholder engagement can reshape large institutions over time. The Q4 2025 portfolio remains a direct expression of that philosophy: few positions, high conviction, and ownership stakes large enough to influence outcomes.

Q4 2025 Changes in Detail: Chris Hohn’s Equity Portfolio

TCI Fund Management made measured adjustments in Q4 2025 without altering the overall structure of the portfolio. There were no new positions and no full exits during the quarter. Activity was limited to selective increases and reductions within existing holdings, maintaining the fund’s concentrated framework.

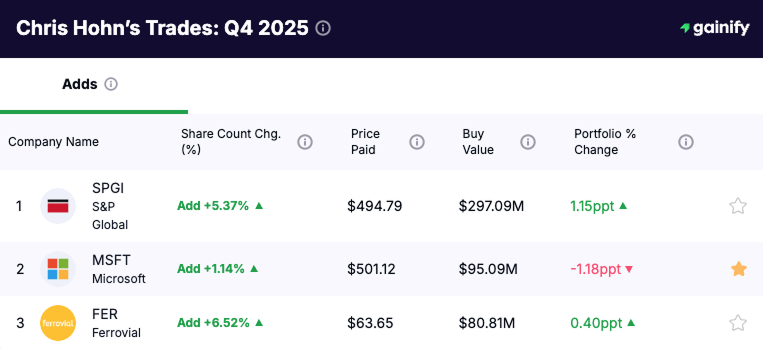

1. Additions: Reinforcing Financial Infrastructure and Software

TCI further increased exposure to businesses tied to financial data, ratings, and enterprise platforms.

- S&P Global (NYSE: SPGI) – Shares increased by 5.37%, adding approximately $297 million. The move reinforces exposure to global credit markets and financial data infrastructure.

- Microsoft (NASDAQ: MSFT) – Shares increased by 1.14%, adding roughly $95 million. Microsoft remains TCI’s primary technology allocation, focused on enterprise software and cloud infrastructure.

- Ferrovial (NASDAQ: FER) – Shares increased by 6.52%, adding about $81 million. The position provides exposure to regulated transport infrastructure and long-duration cash flow assets.

These additions reflect TCI’s preference for companies that generate steady, repeat revenue, operate in regulated or hard-to-replace positions, and maintain consistently strong profit margins.

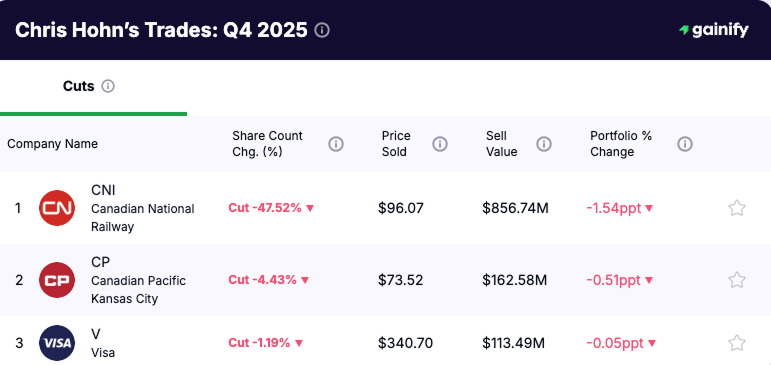

2. Reductions: Scaling Back Rail Exposure

The largest adjustment in Q4 was another reduction in Canadian rail holdings. This marks multiple consecutive quarters of trimming railway exposure, signaling a gradual reweighting rather than a one-time decision.

- Canadian National Railway (NYSE: CNI) – Shares reduced by 47.52%, representing approximately $857 million in value trimmed. This was the most substantial portfolio reduction during the quarter.

- Canadian Pacific Kansas City (NYSE: CP) – Shares declined by 4.43%, equating to roughly $163 million reduced. While the cut was smaller, it reinforces the ongoing reduction in aggregate rail exposure.

- Visa (NYSE: V) – Shares reduced by 1.19%, or approximately $113 million. Despite the trim, Visa remains a core holding within the financial infrastructure allocation.

The pattern is gradual rather than abrupt. Rail exposure remains in the portfolio, but at progressively lower weight over several quarters, while capital has been increasingly directed toward financial infrastructure and industrial restructuring themes.

3. What Did Not Change

- No new stocks added

- No complete position exits

- General Electric remained the largest holding at over 27% of portfolio value

Beyond the rail reductions and selective additions, the overall structure of the portfolio remained stable in Q4. There were no new positions initiated and no full exits, and the core allocations stayed intact. General Electric continued to represent more than 27% of total capital, while Visa, Moody’s, S&P Global, and Microsoft maintained their status as central holdings. The absence of major repositioning suggests that TCI’s current portfolio reflects sustained conviction rather than short-term tactical shifts heading into 2026.

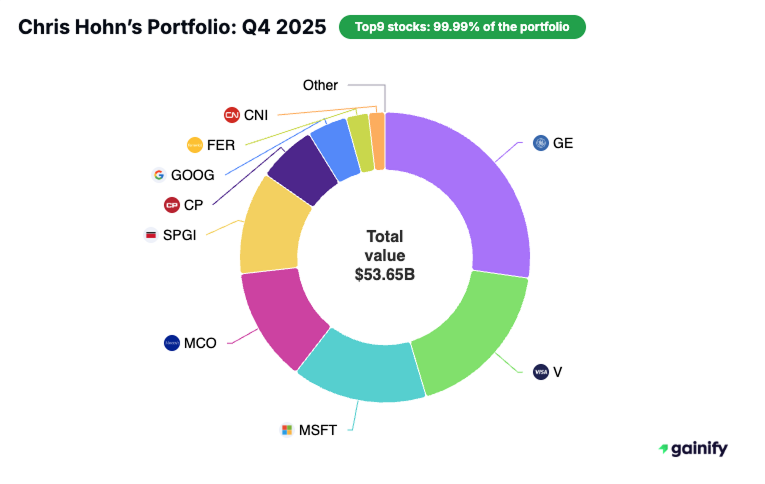

Chris Hohn Top 9 Holdings: Q4 2025 Equity Portfolio

As of the December 31, 2025 SEC Form 13F filing, TCI Fund Management reported $53.7 billion invested across nine U.S.-listed companies. The structure remains highly concentrated, with the top five holdings accounting for more than 80% of total portfolio value.

Rank | Company | Ticker | Market Value | Portfolio Weight |

|---|---|---|---|---|

1 | GE | $14.63B | 27.28% | |

2 | V | $9.72B | 18.12% | |

3 | MSFT | $8.12B | 15.13% | |

4 | MCO | $6.80B | 12.67% | |

5 | SPGI | $6.16B | 11.48% | |

6 | CP | $3.51B | 6.54% | |

7 | GOOG | $2.38B | 4.44% | |

8 | FER | $1.35B | 2.51% | |

9 | CNI | $0.97B | 1.82% |

Portfolio Structure Observations

The portfolio structure highlights how capital is intentionally concentrated in a small number of dominant positions. The top five holdings account for The portfolio is structured around a small number of dominant positions, with overall results driven by a handful of companies rather than wide sector exposure. Capital is allocated where conviction is highest and where ownership scale can influence outcomes.

- Extreme concentration: The top five holdings account for the vast majority of total equity capital, highlighting the fund’s focused structure.

- General Electric dominance: GE is the largest position at over 27% of assets, making it the primary contributor to portfolio performance.

- Financial infrastructure core: Visa, Moody’s, and S&P Global together represent more than 42% of total capital, anchoring the portfolio in payments and credit market infrastructure.

- Selective technology exposure: Microsoft is the main technology allocation, while Alphabet holds a smaller weight relative to other core positions.

Overall, the composition reflects a preference for ownership depth in structurally durable businesses rather than diversification across a wide range of industries.

FAQ: Chris Hohn and TCI Fund Management

What is Chris Hohn’s net worth?

Chris Hohn’s net worth is estimated at approximately $11–12 billion, according to recent financial rankings. His wealth is primarily derived from his ownership stake in TCI Fund Management and the firm’s long-term investment performance.

How did Chris Hohn make his money?

Chris Hohn built his fortune through TCI Fund Management, which he founded in 2003. The firm focuses on concentrated equity investments combined with activist engagement. In 2025 alone, TCI generated an estimated $18.9 billion in net gains, the largest single-year profit ever recorded by a hedge fund according to Edmond de Rothschild’s annual rankings.

What is TCI Fund Management?

TCI Fund Management is a London-based hedge fund managing tens of billions of dollars in assets. The firm runs a highly concentrated equity strategy, typically holding fewer than 10–15 companies and building large ownership stakes designed to influence corporate governance and capital allocation.

What is Chris Hohn’s largest holding?

As of Q4 2025, General Electric (GE) is TCI’s largest holding, representing over 27% of the portfolio. The position reflects Hohn’s long-term investment in GE’s aerospace-focused restructuring.

Is Chris Hohn an activist investor?

Yes. Chris Hohn is widely regarded as one of the most influential activist investors globally. Through TCI, he has engaged with companies on governance reform, cost discipline, and strategic restructuring to improve shareholder value.