Carl Icahn is one of the most iconic and controversial figures in modern financial history. For more than half a century, he has been recognized as one of Wall Street’s boldest investors, a man who made his fortune not by quietly buying and holding but by aggressively pushing for change in the companies where he invested. His name became synonymous with corporate raiding in the 1980s, when he took over companies like Trans World Airlines (TWA) in a highly publicized move that earned him both immense wealth and lasting notoriety.

Over the years, Icahn has refined his strategy into what is now widely known as activist investing. This means taking large stakes in companies, identifying inefficiencies or underperformance, and demanding changes to management practices, capital allocation, or strategic direction.

Through his firm Icahn Enterprises L.P., Icahn has waged battles with some of the biggest names in corporate America. From energy giants to technology leaders, pharmaceutical firms, and industrial companies, his reach has spanned almost every major sector. He has never been afraid of public confrontation. In fact, Icahn often leverages his visibility and reputation to pressure executives into adopting his proposals. Investors and financial media alike have followed his moves closely for decades, and many smaller investors have mimicked his trades under the belief that if Icahn was buying, there must be deep value hiding there.

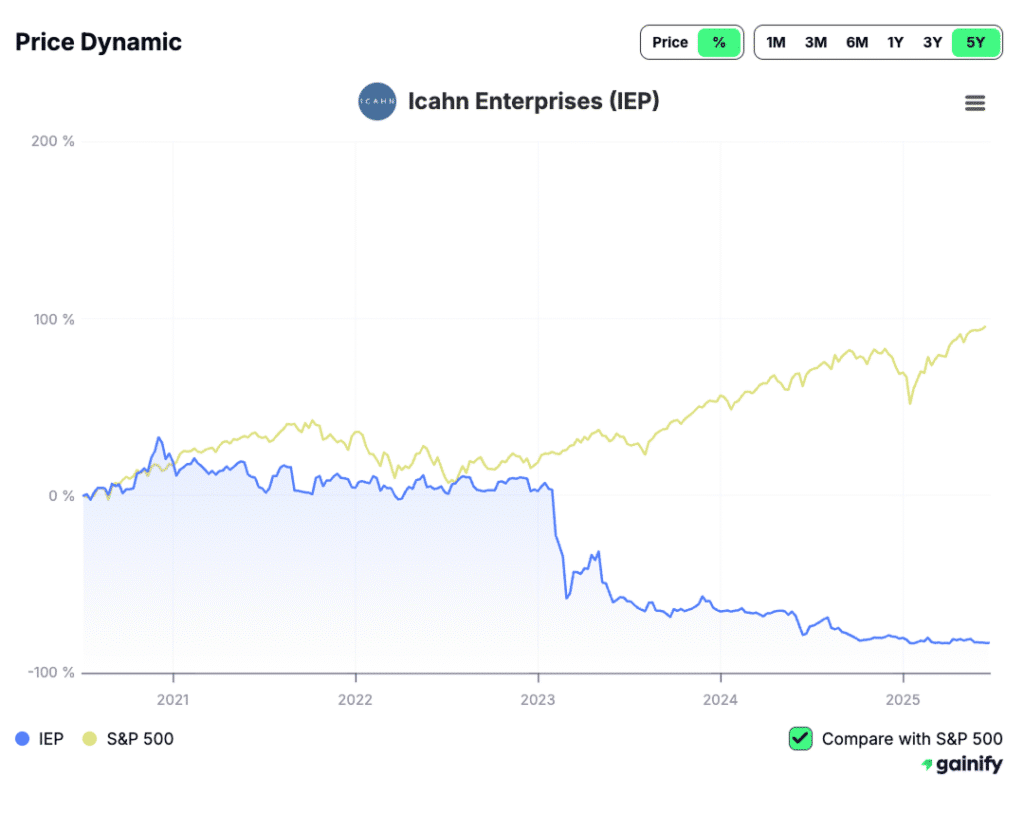

However, the landscape has changed in recent years. Icahn’s empire, once seen as nearly untouchable, has been forced to confront a far tougher reality. His portfolio, which was worth more than 24 billion dollars in early 2021, has now fallen to 7.9 billion dollars as of Q2 2025. That is a decline of more than 60 percent in just five years, and the numbers are even worse when viewed over three years. During this same period, the broader stock market, represented by indexes such as the S&P 500, delivered significant positive returns. The stark underperformance has raised questions about the sustainability of Icahn’s approach in today’s market environment.

This decline does not necessarily mean that Icahn has abandoned the principles that made him successful. His portfolio remains highly concentrated, his trades are still deliberate, and his activist approach is still central. What has changed is the outcome. Some of his largest and most aggressive bets have not produced the returns he expected, and in certain cases they have backfired. For investors, this situation is a case study in the risks of concentration, the volatility of cyclical industries, and the challenges even legendary figures face when markets evolve.

In the following sections, we will explore the details of Icahn’s current portfolio, examine the reasons behind the reduction in stock allocation, review his recent trades, and consider whether Carl Icahn remains as active and influential as he once was.

Who Is Carl Icahn and His Investment Philosophy

Carl Icahn is one of the most recognizable names in modern finance. Born in 1936 in Queens, New York, he started his career as a stockbroker before founding Icahn & Co. in 1968, a firm that specialized in risk arbitrage and options trading. From these beginnings, he built a reputation as one of Wall Street’s most aggressive and influential investors. His methods have often been controversial, but his impact on markets and corporate governance has been undeniable.

Icahn first came to prominence during the 1970s and 1980s, the era of corporate raiders. His takeover of Trans World Airlines (TWA) in 1985 became a symbol of that time. Icahn was unapologetic about selling assets, breaking up companies, and extracting value. This approach made him a billionaire but also earned him the reputation of being “the bane of CEOs,” as executives feared the arrival of Icahn as a shareholder in their company.

Over the years, his strategy evolved into what is now known as shareholder activism. Instead of purely dismantling companies, Icahn began taking large stakes in businesses he considered undervalued or poorly managed. He would then push aggressively for change. His campaigns often involved:

- Proxy battles to gain board seats

- Open letters to management and shareholders

- Public criticism of company leaders

- Demands for restructuring, spinoffs, or buybacks

The mere announcement of his involvement often boosted a stock’s price, as markets expected his pressure to unlock shareholder value.

At the center of Icahn’s philosophy is the belief that many corporations are inefficiently run. He argues that entrenched management teams often act in their own interests rather than those of shareholders. His solution has been to force change, whether by cutting costs, spinning off underperforming divisions, or returning cash through dividends and buybacks. This approach contrasts sharply with long-term investors like Warren Buffett, who prefer to back strong management teams and hold companies for decades.

Icahn has also been famous for running highly concentrated portfolios. Instead of spreading investments across dozens of companies, he often focuses on a handful of positions worth billions each. This high-conviction approach has delivered enormous wins, including successful investments in Apple, Netflix, Herbalife, and eBay. In these cases, he pushed for strategic changes that led to major gains. Yet the same concentration has also created vulnerability, as seen in recent years when large bets in energy, vehicle parts, and chemicals worked against him.

Another consistent feature of Icahn’s philosophy has been the use of hedging strategies. He has frequently taken large short positions or used credit default swaps to protect his holdings or profit from downturns. At times this produced spectacular returns, but it has also led to some of his most painful losses. His prolonged bet that the U.S. economy would collapse is a prime example. The crash never came, and the hedge ultimately cost him billions of dollars.

Despite criticism, Icahn continues to frame himself as a defender of the average shareholder. He insists that without activists like him, corporate leaders would remain complacent and continue wasting capital. Supporters view him as a watchdog who brings accountability, while critics argue that his focus on short-term financial engineering damages long-term corporate health.

Today, Icahn’s philosophy still revolves around activism, concentration, and the pursuit of undervalued companies. Yet the setbacks of recent years, combined with new challenges such as the rise of passive index funds and stronger corporate defenses, have made his path more difficult. Even so, Icahn remains committed to his belief that shareholders deserve better and that bold action is often the only way to achieve it.

Portfolio Value Decline

By mid-2025, Carl Icahn’s publicly disclosed stock holdings were valued at about $7.9 billion, down from more than $24 billion at their peak in early 2021. The shrinkage is dramatic, leaving his equity portfolio worth less than one-third of its former size and marking one of the most severe declines experienced by a prominent billionaire investor in recent memory.

Part of the damage came from Icahn’s own strategy. Between 2017 and 2023, he maintained a large bearish wager that the U.S. stock market would collapse. Instead, the market rallied, especially after massive government stimulus during the pandemic. According to the Financial Times, these hedging positions cost him nearly $9 billion in cumulative losses. Icahn later conceded that he had ignored his own long-held advice not to overcommit to timing the market, calling the bet “ill-advised.”

The situation worsened in 2023 when Hindenburg Research published a scathing short report on Icahn Enterprises. The firm alleged that Icahn’s company was overstating asset values and sustaining its famously high dividend through what it called a “ponzi-like” structure. The report triggered a violent sell-off: shares of Icahn Enterprises fell by nearly 37% intraday, its market capitalization was cut by about $6 billion, and Icahn’s personal net worth fell by more than $10 billion in a single day.

A few months later, the company was forced to halve its quarterly dividend for the first time since 2011, cutting it from $2 to $1 per share. That move sparked another plunge of about 25% in one session, wiping an additional $1.7 billion from Icahn’s fortune. By the end of 2024, nearly $20 billion in market value had been erased from Icahn Enterprises compared to its level before the Hindenburg report, and Icahn’s personal net worth had fallen from almost $25 billion in early 2023 to under $8 billion.

Taken together, the failed multi-year bet against the U.S. economy and the sharp fallout from the Hindenburg report transformed Icahn’s position on Wall Street. His portfolio is still active, but at a much smaller scale, and his reputation now carries the weight of some of the largest personal and corporate losses in recent financial history.

Recent Trading Activity in Q2 2025

During the second quarter of 2025, Carl Icahn’s portfolio adjustments were relatively limited compared to his past activity. No brand-new positions were initiated, and there were no cuts to existing holdings, apart from two full exits.

On the buying side, Icahn increased stakes in a handful of his core holdings:

- Icahn Enterprises (IEP): Share count rose by +9.76%, with a buy value of about $376.6 million.

- Centuri Holdings (CTRI): The most notable increase, with a +157.55% surge in shares, representing a buy value of $76.6 million.

- CVR Energy (CVI): Shares added modestly, up +2.75%, worth $41.5 million.

- CVR Partners (UAN): Stake grew by +1.59%, valued at $5.2 million.

On the selling side, Icahn fully exited two positions:

- Dana (DAN): Sold his entire stake at an average price of $14.93, realizing $213.3 million in value.

- Illumina (ILMN): Also sold out completely, at an average price of $81.16, with a total sell value of $17.9 million.

In summary, Q2 2025 saw Icahn doubling down on existing bets, especially with a very large increase in Centuri Holdings, while trimming his portfolio through the complete sale of Dana and Illumina. With no new names added, the quarter reinforced his strategy of concentrating capital into a smaller set of core positions rather than diversifying.

Holdings Breakdown

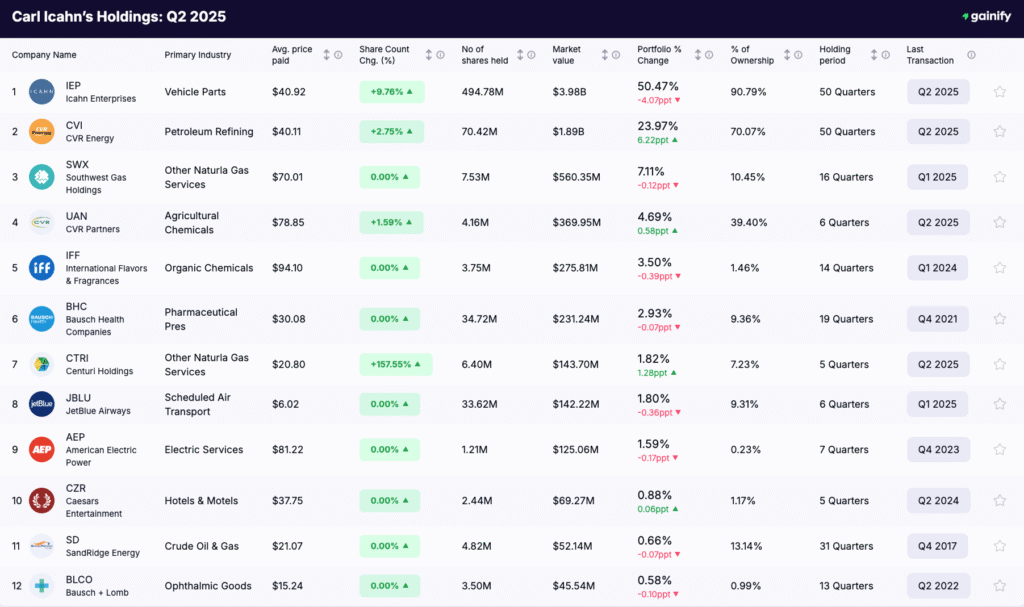

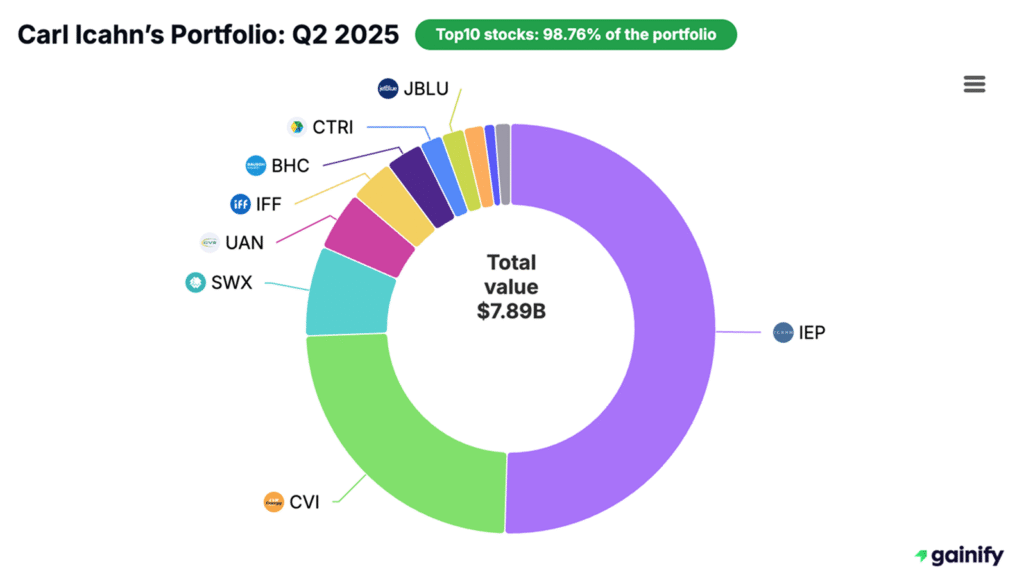

Here are the largest positions as of Q2 2025, illustrating just how concentrated Icahn’s equity portfolio remains:

- Icahn Enterprises (IEP): Vehicle Parts, 3.98 billion dollars, 50.47 percent of total portfolio.

- CVR Energy (CVI): Petroleum Refining, 1.89 billion dollars, 23.97 percent.

- Southwest Gas Holdings (SWX): Natural Gas Services, 560 million dollars, 7.11 percent.

- CVR Partners (UAN): Agricultural Chemicals, 370 million dollars, 4.69 percent.

- International Flavors & Fragrances (IFF): Organic Chemicals, 275 million dollars, 3.50 percent.

- Bausch Health Companies (BHC): Pharmaceuticals, 231 million dollars, 2.93 percent.

- Centuri Holdings (CTRI): Natural Gas Services, 144 million dollars, 1.82 percent.

- JetBlue Airways (JBLU): Airlines, 142 million dollars, 1.80 percent.

- American Electric Power (AEP): Electric Services, 125 million dollars, 1.59 percent.

- Caesars Entertainment (CZR): Hotels and Motels, 69 million dollars, 0.88 percent.

- SandRidge Energy (SD): Oil and Gas, 52 million dollars, 0.66 percent.

- Bausch plus Lomb (BLCO): Ophthalmic Goods, 46 million dollars, 0.58 percent.

Together, these holdings make up his entire reported equity portfolio.

Is Carl Icahn Still Active?

Yes, Carl Icahn is still active, but his activity looks different today compared to his earlier years. He continues to manage billions in stock positions, adjusts his holdings each quarter, and remains deeply invested in industries like energy and industrial services. His long average holding period, which is 17 quarters, shows that he still commits to positions for years at a time, even as he tactically trims or adds in the short term.

At the same time, it is undeniable that Icahn is managing a smaller and more fragile portfolio. The dramatic losses and exits suggest that he has scaled back from the aggressive expansion that once defined his strategy. He is still a presence in the market, but he no longer carries the same level of influence as during his peak years. Investors and analysts continue to watch his moves, but the narrative has shifted from celebration of his bold wins to questions about whether his concentrated, activist style is suited to the current market environment.

Final Thoughts

Carl Icahn’s career is a study in both the rewards and risks of activist investing. His ability to build wealth by taking large stakes and forcing change is unquestionable, but the past few years show the vulnerability of even the most famous investors when markets turn against their chosen sectors.

Today his portfolio is smaller, more concentrated, and deeply tied to a handful of companies. Despite suffering losses of more than 60 percent over five years, Icahn continues to place bets, reinforce positions, and exit holdings he no longer supports. That persistence highlights both his resilience and his conviction.

For investors, Icahn’s journey is an important reminder. Concentration can deliver extraordinary gains, but it also magnifies losses when things go wrong. Diversification, patience, and adaptability remain essential for long-term success. Icahn may no longer dominate headlines with massive wins, but his career and his current portfolio still provide lessons for anyone interested in the dynamics of high conviction investing.