Brad Gerstner’s portfolio is a concentrated public equity allocation strategy built around technology infrastructure, dominant digital platforms, and scalable data businesses. Through Altimeter Capital, Gerstner deploys capital using a crossover model that favors companies controlling critical layers of the modern computing stack: semiconductors, cloud platforms, AI systems, and large-scale digital marketplaces.

This portfolio is not designed for sector diversification. It is constructed for asymmetric exposure to long-duration technology cycles, with position sizing reflecting conviction rather than index weight. The top holdings consistently represent the majority of capital, and turnover is used as a strategic reallocation tool rather than short-term trading.

According to Altimeter Capital’s SEC Form 13F filing as of December 31, 2025, the portfolio totaled $6.66 billion across 18 public holdings, with approximately 90% of capital concentrated in the top 10 positions. During Q4 2025, exposure increased to AI infrastructure, most notably through additions to CoreWeave and NVIDIA, while China-related exposure was fully eliminated through exits from Alibaba Group and PDD Holdings. At the same time, valuation risk was reduced through significant position cuts in Broadcom and Robinhood.

In the sections ahead, we will break down Altimeter’s Q4 2025 capital reallocation in detail, examine its top holdings, and highlight how Gerstner’s technology-first philosophy is shaping one of the most concentrated and forward-looking hedge fund portfolios on the market today.

Brad Gerstner Portfolio in 60 Seconds

- What it is: A highly concentrated public equity portfolio managed by Brad Gerstner through Altimeter Capital, focused on companies that control core layers of the global technology stack rather than broad sector exposure.

- How it’s built: Capital is allocated based on conviction and long-duration technology cycles, not index weights. A small number of positions account for most of the portfolio, and position sizing is the primary risk-management tool.

- Top positions: As of the SEC Form 13F dated December 31, 2025, the three largest holdings are NVIDIA, Meta Platforms, and Microsoft, together representing more than half of total portfolio value.

- Current positioning: The portfolio is structured for AI infrastructure demand, platform-scale monetization, and regulatory clarity, with reduced exposure to geopolitically sensitive and valuation-stretched segments.

Who Is Brad Gerstner?

Brad Gerstner is a technology-focused hedge fund manager and venture investor best known as the founder, chairman, and CEO of Altimeter Capital. He launched the firm in 2008 with a mandate to invest across private and public markets using a crossover strategy anchored in long-term technology adoption cycles.provide

Gerstner built his reputation by investing early in companies before they became public market leaders, including Uber, Snowflake, and Airbnb, and by continuing to hold these positions as the businesses scaled after IPO. At the same time, he has maintained long-term public-market positions in established platforms such as Amazon, Microsoft, and NVIDIA. This combination allows Altimeter to participate in value creation both before and after companies reach maturity in public markets.

Unlike short-term-oriented funds, Gerstner demonstrates patience in compounding growth. The average holding period in Altimeter’s portfolio is around nine quarters, with core positions such as Meta and Microsoft held for over 30 quarters. At the same time, he is pragmatic and willing to pivot, trimming or exiting lower-priority holdings when conditions change.

Over the past decade, Gerstner has become one of the most closely followed technology investors, with Altimeter frequently cited as a bellwether for long-term conviction in software, cloud infrastructure, and artificial intelligence.

Investment Philosophy

Brad Gerstner’s investment philosophy is shaped by a technology-first worldview and a belief that innovation cycles in software, cloud, and artificial intelligence will continue to drive outsized equity returns. Altimeter Capital is structured around a crossover model, enabling the firm to back high-growth companies in their private stages and hold them into public markets, bridging the gap between venture capital and hedge fund investing.

At the core of his approach are three principles:

- High-Conviction Concentration – Gerstner prefers to build large, focused positions in companies he believes have enduring competitive advantages, rather than spreading capital too thin across many names. This conviction has led to multi-billion-dollar stakes in firms like Meta, Microsoft, and Snowflake.

- Long-Term Compounding – While trading activity is a tool, Gerstner emphasizes patience. Core holdings are often kept for years, allowing secular growth trends in cloud infrastructure, data, and AI to compound over time.

- Adaptability and Opportunism – Despite his long-term orientation, Gerstner is not rigid. – Gerstner actively reallocates capital when risk-reward conditions change. In Q4 2025, this was demonstrated by increasing exposure to CoreWeave and NVIDIA, while fully exiting Alibaba Group and PDD Holdings.

This combination of patience and flexibility reflects Gerstner’s broader belief that the best returns come from holding the right companies through innovation cycles, while still keeping discipline to rotate away from lower-priority or overvalued positions.

Brad Gerstner’s Q4 2025 Portfolio Moves

Brad Gerstner used Q4 2025 to increase exposure to AI infrastructure and remove sources of elevated risk. The quarter was characterized by additions to AI-focused holdings, the complete exit of China-related positions, and selective valuation-driven reductions, resulting in a more concentrated portfolio.

1. Major Additions (Q4 2025)

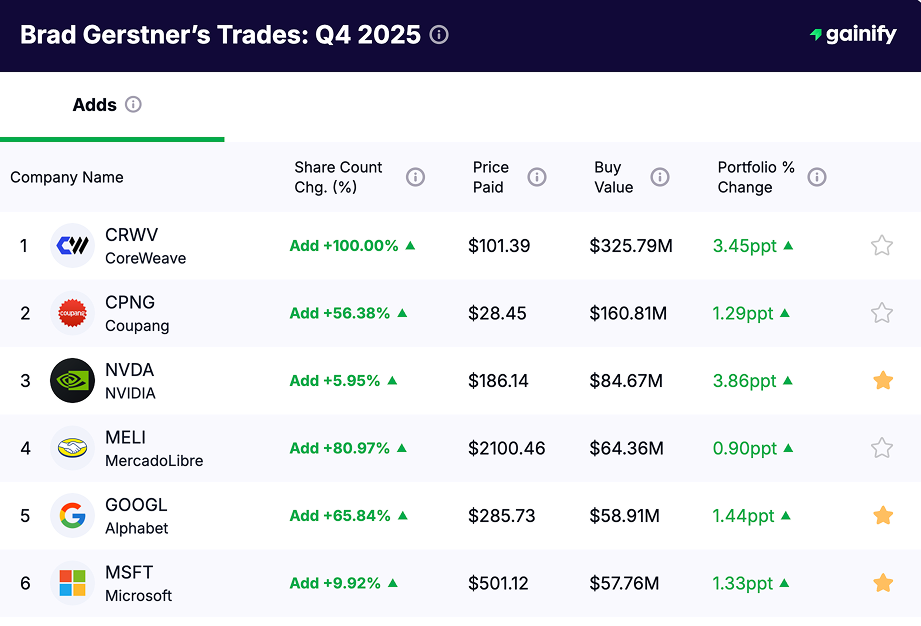

During Q4 2025, Brad Gerstner concentrated new capital into a small number of positions tied to AI infrastructure, platform scale, and global digital commerce, based on the SEC Form 13F as of December 31, 2025.

- CoreWeave (NASDAQ: CRWV): The position was doubled (+100%) with a $325.79 million purchase, making it the largest addition of the quarter and reinforcing Altimeter’s exposure to AI compute and data center infrastructure.

- Coupang (NYSE: CPNG): Added $160.81 million (+56.38%), increasing exposure to a scaled e-commerce and logistics platform with improving operating leverage in South Korea.

- NVIDIA (NASDAQ: NVDA): Increased by $84.67 million (+5.95%), maintaining NVIDIA as the portfolio’s largest holding and core AI hardware exposure.

- MercadoLibre (NASDAQ: MELI): Added $64.36 million (+80.97%), expanding exposure to Latin American e-commerce and fintech growth.

- Alphabet (NASDAQ: GOOGL): Increased by $58.91 million (+65.84%), reflecting confidence in large-scale AI monetization across search, cloud, and advertising.

- Microsoft (NASDAQ: MSFT): Added $57.76 million (+9.92%), reinforcing long-term exposure to enterprise cloud and AI integration.

➡️ In total, Altimeter added over $700M across high-growth technology and platform companies.

2. New Buys (Q4 2025)

Altimeter Capital initiated two new positions as part of a selective expansion into commerce and energy infrastructure In Q4 2025. He established a $91.55 million stake in Shopify, reflecting renewed conviction in Shopify’s role as a core operating layer for independent e-commerce with improving margin structure and platform leverage. At the same time, he opened a $27.39 million position in Bloom Energy, adding exposure to distributed power generation as electricity demand from data centers and AI-driven compute continues to rise.

3. Reductions (Q4 2025)

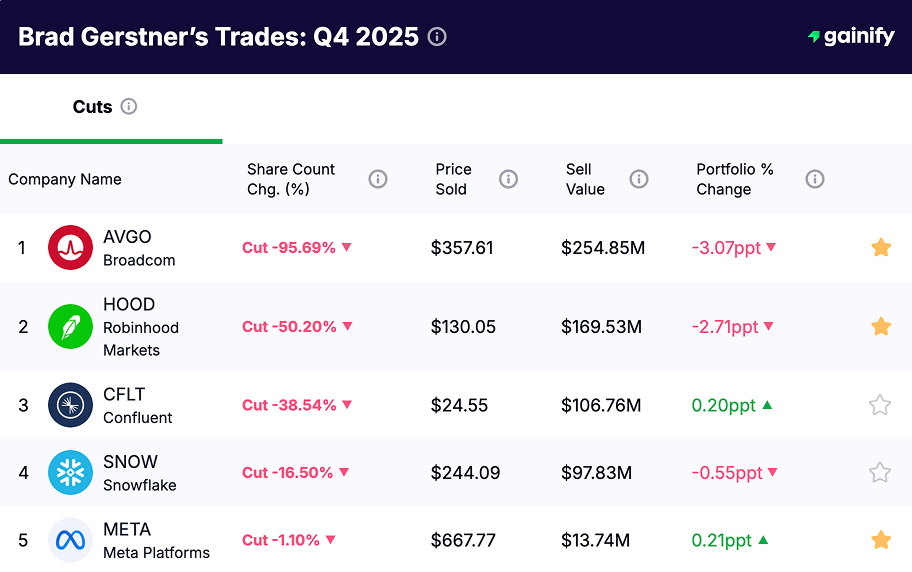

Altimeter Capital reduced exposure to positions where valuation expansion outpaced near-term fundamentals or where portfolio weight exceeded updated risk-reward expectations. These moves reflect position-sizing discipline mainly.

- Broadcom (NASDAQ: AVGO): The position was cut by 95.69% ($254.85M), signaling a decisive reduction after strong performance and elevated valuation relative to other AI infrastructure opportunities.

- Robinhood (NASDAQ: HOOD): Gerstner reduced the position by 50.20% ($169.53M), locking in gains following a sharp re-rating while maintaining residual exposure to retail trading activity.

- Confluent (NASDAQ: CFLT): A 38.54% trim ($106.76M) reflects continued caution toward consumption-based software models amid more selective enterprise spending.

- Snowflake (NASDAQ: SNOW): The 16.50% reduction ($97.83M) further compressed exposure to premium-valued cloud data platforms as growth normalization continues.

➡️ Reductions freed capital for higher-conviction bets in semiconductors and cloud infrastructure.

4. Exits (Q4 2025)

In Q4 2025, Altimeter Capital fully exited several positions as part of a broader effort to simplify the portfolio, eliminate China-related and cyclical exposure, and redeploy capital toward higher-conviction infrastructure assets. These exits were decisive and removed entire risk categories rather than trimming around the edges.

- PDD Holdings (PDD): The $170.31M full exit eliminated direct exposure to China’s consumer internet sector and associated regulatory and geopolitical risk.

- Arm Holdings (ARM): A $159.66M sell-out reflects reduced conviction in semiconductor IP licensing relative to other AI infrastructure opportunities.

- Alibaba Group (BABA): The $157.83M exit completed Altimeter’s withdrawal from China-centric platforms amid persistent policy and governance uncertainty.

- Maplebear (CART): Selling $136.09M removed exposure to consumer delivery economics with limited margin expansion and competitive intensity.

- Synopsys (SNPS): The $114.74M exit reduced exposure to semiconductor design tools with cyclical demand and less direct linkage to near-term AI compute growth.

➡️ These exits created liquidity that Altimeter redirected into AI infrastructure, semiconductor design, and large-scale platform companies with clearer monetization pathways.

Brad Gerstner’s Portfolio Top 10 Holdings: Q4 2025

Rank | Company | Market Value | % of Portfolio | Shares Held | Notes |

|---|---|---|---|---|---|

1 | NVIDIA (NVDA) | $1.51B | 22.68% | 8.10M | Largest holding, increased in Q4, core AI compute exposure |

2 | Meta Platforms (META) | $1.22B | 18.28% | 1.85M | Long-duration core position, scaled data and monetization platform |

3 | Microsoft (MSFT) | $617.75M | 9.27% | 1.28M | Anchor compounder across cloud, enterprise software, and AI |

4 | Amazon (AMZN) | $511.42M | 7.68% | 2.22M | AWS-driven infrastructure exposure and retail scale |

5 | Uber (UBER) | $456.66M | 6.85% | 5.59M | Scaled mobility and logistics platform |

6 | Snowflake (SNOW) | $444.78M | 6.68% | 2.03M | Trimmed in Q4, still core enterprise data exposure |

7 | Taiwan Semiconductor Manufacturing (TSM) | $370.51M | 5.56% | 1.22M | Increased exposure to global chip manufacturing |

8 | Coupang (CPNG) | $369.82M | 5.55% | 15.68M | Added aggressively, logistics-driven commerce platform |

9 | CoreWeave (CRWV) | $230.10M | 3.45% | 3.21M | Doubled in Q4, pure-play AI infrastructure |

10 | Confluent (CFLT) | $209.66M | 3.15% | 6.93M | Reduced position, retained as smaller data-platform exposure |

The Q4 2025 holdings place most of the portfolio’s weight behind a very small group of companies, with performance increasingly linked to outcomes at NVIDIA, Meta Platforms, and Microsoft. With these positions representing more than half of total value, portfolio results are shaped less by diversification and more by execution at the core platform and infrastructure layer of the technology stack.

Across the remainder of the top holdings, exposure is concentrated in businesses that control capacity, distribution, or data at scale. Semiconductors, cloud platforms, and AI infrastructure account for the majority of invested capital, reinforcing an orientation toward companies with structural pricing power and operating leverage as compute demand expands.

At the same time, the Q4 composition reflects fewer moving parts than in prior periods. Capital is allocated to a narrower set of businesses with clearer earnings visibility, reduced geopolitical sensitivity, and more direct linkage to long-duration technology demand, resulting in a portfolio that is simpler in structure and more intentional in risk profile.

Key Takeaways

Altimeter Capital’s Q4 2025 SEC Form 13F (as of December 31, 2025) reflects a portfolio that became more concentrated, more infrastructure-led, and less exposed to geopolitical risk.

Leaning further into AI infrastructure: A doubling of CoreWeave and additional capital allocated to NVIDIA reinforced exposure to compute capacity, data center demand, and AI accelerator deployment. These moves increased alignment with the supply side of AI rather than application-layer growth.

Complete withdrawal from China exposure: Full exits from Alibaba Group and PDD Holdings removed direct regulatory and geopolitical sensitivity from the portfolio. This action simplified the risk profile and reduced dependence on China’s domestic policy environment.

Valuation discipline through meaningful cuts: Significant reductions in Broadcom and Robinhood demonstrate active position sizing where forward returns appeared less asymmetric relative to alternatives.

Core concentration maintained: NVIDIA, Meta Platforms, and Microsoft remain the structural anchors of the portfolio, collectively driving the majority of capital allocation and linking performance to AI compute, platform monetization, and enterprise cloud expansion.

Bottom line: Q4 2025 shows Brad Gerstner tightening execution around infrastructure, removing geopolitical complexity, and increasing dependence on a smaller group of scaled technology leaders positioned at the center of AI-driven capital expenditure.