David Einhorn’s portfolio represents the publicly disclosed U.S. equity holdings managed by DME Capital Management, structured as a concentrated, conviction-weighted deployment of capital into businesses he believes are mispriced relative to their normalized earnings and asset value. In Q4 2025, the portfolio totals $2.85 billion across 41 positions, with more than 65% of capital allocated to the top 10 holdings. This structure reflects Einhorn’s disciplined strategy of assigning significant capital to a limited number of high-conviction ideas based on intrinsic value analysis.

Few names in modern investing carry as much weight as David Einhorn. For nearly three decades, Einhorn has been one of Wall Street’s most closely watched hedge fund managers – a man known equally for his brilliant long-term bets on undervalued companies and his fearless short positions that exposed corporate weaknesses. His investment philosophy is documented in his book “Fooling Some of the People All of the Time” (2008), where he outlines a research-intensive approach centered on intrinsic value, accounting scrutiny, and asymmetric risk-reward positioning. The framework described in that book remains visible in today’s portfolio structure: concentrated exposure, sector selectivity, and willingness to diverge from consensus positioning.

As of the reporting period ending December 31, 2025, DME Capital’s allocation reveals clear sector concentration and thematic positioning. The largest position remains Green Brick Partners (GRBK) at over 20% of total assets, reinforcing Einhorn’s long-standing exposure to residential homebuilding. Additional core holdings include infrastructure contractor Fluor (FLR), insurer Brighthouse Financial (BHF), and pharmaceutical manufacturer Teva Pharmaceutical (TEVA). Together, these holdings represent over 40% of the entire portfolio, underscoring Einhorn’s belief in concentration over diversification.

This article breaks down David Einhorn’s Q4 2025 portfolio by examining top holdings, position sizes, sector allocation, new buys, reductions, and exits. It focuses on measurable capital shifts and concentration levels to show where conviction increased, where exposure was reduced, and what the current structure signals about his value-driven strategy going forward.

David Einhorn Portfolio in 60 Seconds

- High-Conviction Allocation: 65% of capital is concentrated in the top 10 holdings.

- Intrinsic Value Focus: Positions are selected based on normalized earnings power and asset value.

- No Mega-Cap Tech Exposure: The portfolio has no meaningful allocation to Big Tech or the “Magnificent 7,” reinforcing its divergence from benchmark-heavy growth indices.

- Post-Underperformance Discipline: After multi-year relative underperformance versus growth benchmarks, the strategy remains firmly rooted in concentrated value investing.

Who Is David Einhorn?

David Einhorn, born in 1968, is one of the most recognized names in value investing. He founded Greenlight Capital in 1996 with just under $1 million in seed money and built it into a multi-billion-dollar investment firm through a research-intensive, long-short equity strategy focused on intrinsic value and balance sheet analysis.

Greenlight Capital’s early performance established Einhorn’s reputation. During its first decade, the fund generated strong double-digit annualized returns, materially outperforming broad market benchmarks. The strategy was based on concentrated long positions in undervalued companies and selective short positions in businesses with structural weaknesses, accounting distortions, or overstated earnings.

Some of his most influential public investment cases include:

- Allied Capital (2002): Einhorn publicly challenged the company’s accounting practices, initiating a multi-year dispute that brought national attention to his forensic accounting approach.

- Lehman Brothers (2007): He warned about leverage and balance sheet risk ahead of the 2008 financial crisis, reinforcing his reputation as a disciplined credit and equity analyst.

- The “Einhorn Effect”: His public presentations often triggered immediate stock price reactions, reflecting the market’s sensitivity to his fundamental critiques.

His investment philosophy is outlined in his book “Fooling Some of the People All of the Time” (2008), where he details a framework centered on intrinsic value estimation, earnings quality assessment, downside protection, and asymmetric risk-reward positioning. A core element of his process is identifying discrepancies between reported financial results and underlying economic reality.

For years, Einhorn delivered exceptional performance. Between inception and the early 2000s, Greenlight Capital returned around 26% annually, vastly outpacing the broader market. Over the full history of the fund, annualized returns have been closer to 13%, still ahead of the S&P 500.

But like many value investors, Einhorn faced difficult years when growth stocks and passive index funds dominated markets. Starting in 2015, performance weakened, culminating in a -34% loss in 2018, which triggered investor redemptions and a shrinking asset base. Despite setbacks, Einhorn never abandoned his principles of long-short, value-oriented investing grounded in fundamental research and risk awareness.

The 2024 Restructuring: From Greenlight to DME Capital

In 2024, Greenlight Capital formally transitioned into DME Capital Management reflecting structural changes. The reorganization streamlined operations, reduced external capital complexity, and reinforced a focused, conviction-driven investment framework while preserving Einhorn’s long-standing strategy.

The core elements of the DME Capital structure include:

- Long-Short Equity Discipline: Capital is allocated to undervalued equities while selectively shorting structurally impaired businesses.

- High-Conviction Concentration: Position sizing remains deliberate, with meaningful capital assigned to a limited number of ideas.

- Active Engagement: The firm maintains the ability to engage with management teams when capital structure or governance improvements can unlock value.

- Risk-Aware Construction: Portfolio structuring emphasizes downside analysis, balance sheet strength, and liquidity considerations.

The transition also acknowledged a changed market environment. Over the past decade, passive capital flows and multiple expansion in growth sectors reduced dispersion across many equities. Under DME Capital, Einhorn reinforced a focus on valuation-driven mispricings, cyclical dislocations, and special situations that require fundamental analysis rather than benchmark alignment.s and special situations that many larger, index-driven funds ignore.

Einhorn’s Portfolio in Q4 2025

David Einhorn’s DME Capital entered 2026 with a $2.85 billion portfolio spread across 41 positions, but as always, it remains highly concentrated. His top 10 holdings account for 65% of the portfolio’s value, reflecting a strategy of taking large, conviction-driven stakes rather than diversifying broadly.

The portfolio composition highlights Einhorn’s long-standing playbook: deep-value bets in housing and infrastructure, contrarian healthcare exposures, and selective energy/resource positions that hedge against inflation and global uncertainty.

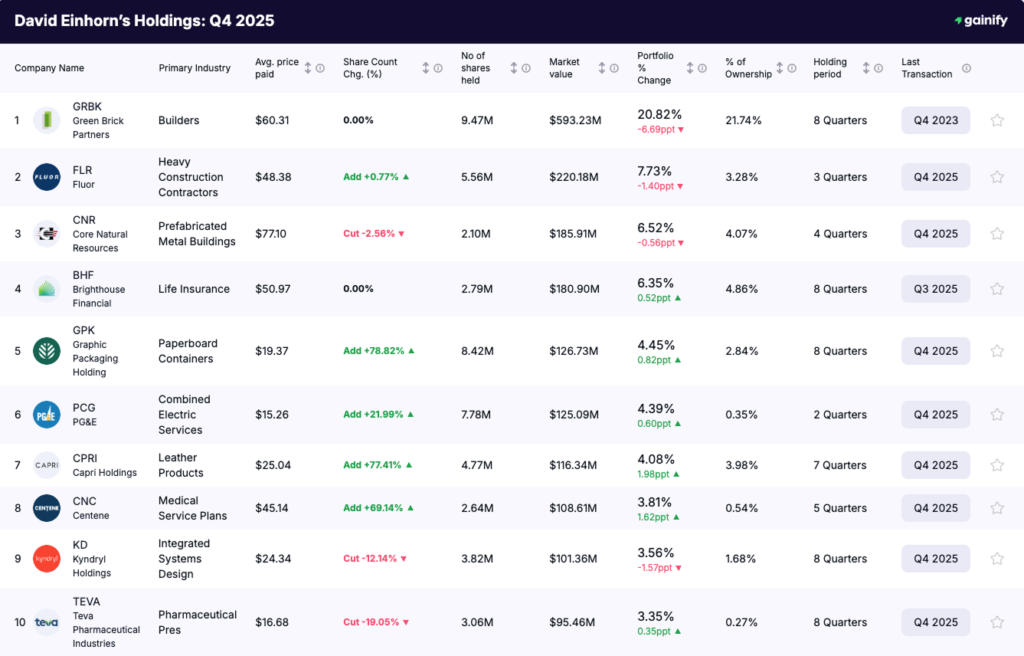

Top 10 Portfolio Holdings

David Einhorn’s top 10 holdings represent 65.1% of DME Capital’s $2.85B portfolio, confirming a concentrated allocation strategy built on high-conviction intrinsic value positions. Below is a breakdown of each core holding, its portfolio weight, and its strategic role.

1. Green Brick Partners (NYSE:GRBK) – $593.2M (20.8%)

Green Brick Partners is a U.S. homebuilder and land developer, focused primarily on high-growth Texas markets. It is David Einhorn’s largest position and has been held for 8 quarters with no Q4 share change. The allocation reflects long-term conviction in housing supply-demand imbalance and land-backed asset value. As chairman, Einhorn combines capital exposure with governance influence.

2. Fluor (NYSE:FLR) – $220.2M (7.7%)

Fluor is a global engineering and construction company serving infrastructure, energy, and industrial markets. The position was modestly increased (+0.77%) in Q4. This holding provides exposure to large-scale capital expenditure cycles and U.S. infrastructure spending.

3. Core Natural Resources (NYSE:CNR) – $185.9M (6.5%)

Core Natural Resources operates in commodity-based materials and energy-linked resources. Einhorn trimmed the position slightly (-2.56%) while maintaining it as a top holding. The allocation provides commodity cash flow exposure and inflation-sensitive earnings.

4. Brighthouse Financial (NASDAQ:BHF) – $180.9M (6.4%)

Brighthouse Financial is a life insurance and annuities provider. The share count remained unchanged in Q4. This position offers leverage to interest rate spreads and capital return potential through balance sheet revaluation.

5. Graphic Packaging Holding (NYSE:GPK) – $126.7M (4.5%)

Graphic Packaging manufactures paperboard and consumer packaging solutions. Einhorn increased the position significantly (+78.82%), making it one of the largest adds in the top 10. The thesis centers on stable cash flow generation and valuation normalization.

6. PG&E (NYSE:PCG) – $125.1M (4.4%)

PG&E is a regulated electric utility serving California. The position was increased by 21.99% in Q4. The allocation adds regulated earnings visibility and infrastructure-linked revenue stability.

7. Capri Holdings (NYSE:CPRI) – $116.3M (4.1%)

Capri Holdings is a global luxury fashion group (Michael Kors, Versace, Jimmy Choo). Einhorn increased the position by 77.41%, indicating conviction in brand value realization and earnings recovery potential.

8. Centene (NYSE:CNC) – $108.6M (3.8%)

Centene is a managed healthcare insurer focused on government-sponsored programs. The position was increased by 69.14% in Q4. The allocation reflects confidence in reimbursement-driven earnings and valuation compression reversal.

9. Kyndryl Holdings (NYSE:KD) – $101.4M (3.6%)

Kyndryl is an IT infrastructure services company spun off from IBM. Einhorn reduced the position by 12.14% while keeping it within the top 10. The trim suggests capital rebalancing as the restructuring thesis progresses.

10. Teva Pharmaceutical (NYSE:TEVA) – $95.5M (3.4%)

Teva Pharmaceutical is a global generic drug manufacturer undergoing operational restructuring. The position was reduced by 19.05% in Q4. Despite the trim, it remains a core exposure to pharmaceutical turnaround potential.

David Einhorn’s Q4 2025 portfolio shows limited exposure to large-cap technology stocks and no meaningful allocation to mega-cap AI-driven names that dominate benchmark indices. Unlike many hedge funds whose performance is heavily tied to technology multiples, Einhorn’s capital is deployed primarily in asset-backed, cash-generating, and cyclical businesses.

This allocation profile indicates preference for companies with tangible assets, predictable cash flows, or restructuring potential rather than high-duration growth equities. The absence of large technology exposure reduces sensitivity to multiple compression in growth sectors but increases dependence on cyclical recovery, interest rate development, and sector-specific catalysts.

Biggest Conviction Moves – Q4 2025

Q4 2025 shows selective capital concentration into existing core holdings, measured trims in restructuring names, and several full exits. The activity reinforces David Einhorn’s conviction-weighted allocation model.

Largest Additions in Q4 2025

1. Graphic Packaging (NYSE: GPK) +78.8%

Graphic Packaging was one of the largest percentage increases in the portfolio. The position now stands at $126.7M (4.45%). The scale of the add signals increased conviction in packaging cash flow durability and valuation support.

2. Capri Holdings (NYSE: CPRI) +77.4%

Capri Holdings rose to $116.3M (4.08%) after a significant increase. The move suggests Einhorn sees earnings normalization or corporate action potential in the luxury apparel group.

3. PG&E (PCG) +22.0%

The regulated utility position grew to $125.1M (4.39%), adding defensive, rate-based earnings exposure.

4. Centene (NYSE: CNC) +69.1%

Centene increased to $108.6M (3.81%). The sizable addition indicates confidence in managed care reimbursement economics and valuation compression reversal.

5. Fluor (NYSE:FLR) +0.77%

Fluor remains the second-largest holding at $220.2M (7.73%). The modest increase reflects position maintenance within a high-conviction infrastructure thesis

Reductions in Q4 2025

1. Teva Pharmaceutical (NYSE:TEVA) -19.05%

Teva was reduced to $95.46M (3.35%). The trim suggests capital rebalancing while maintaining exposure to the restructuring thesis.

2. Kyndryl (NYSE:KD) -12.14%

Kyndryl was lowered to $101.36M (3.56%), indicating moderated conviction as the turnaround progresses.

3. Core Natural Resources (NYSE:CNR) -2.56%

A small reduction while preserving a top-three portfolio position at $185.91M (6.52%).

Full Exits (100% Sold Out) in Q4 2025

According to the Q4 2025 13F filing, David Einhorn fully exited the following positions:

- Seadrill (NYSE:SDRL)

- Nexstar Media Group (NASDAQ:NXST)

- HP Inc. (NYSE:HPQ)

- VanEck Oil Services ETF (OIH)

A full exit means the entire reported equity position was reduced to zero during the quarter. These disposals indicate deliberate capital reallocation rather than incremental trimming.

New Positions Initiated in Q4 2025

In Q4 2025, David Einhorn initiated several new equity positions, signaling fresh capital deployment into select ideas rather than broad expansion of portfolio breadth.

- Eastman Chemical (NYSE:EMN)

- Tenet Healthcare (NYSE:THC)

- CNX Resources (NYSE:CNX)

A new position in a 13F filing indicates that the holding did not exist in the prior quarter and capital was deployed during Q4.

The additions reflect targeted exposure across chemicals, hospital operations, and natural gas production. Rather than initiating large-scale new bets, Einhorn introduced measured allocations in sectors tied to industrial activity, healthcare services utilization, and domestic energy production. The position sizes suggest exploratory but thesis-driven entries that may be scaled in future quarters depending on valuation and operating performance developments.

Conclusion: Einhorn’s Next Chapter

David Einhorn’s journey from Greenlight to DME Capital reflects both the challenges and the resilience of a legendary investor. While his performance has seen highs and lows, his philosophy remains consistent: value first, risk-aware structuring, and patience in conviction bets.

The Q4 2025 portfolio shows Einhorn adapting to today’s markets by leaning into housing, infrastructure, and healthcare while exiting weaker consumer names and speculative plays. His willingness to hold concentrated positions like GRBK alongside contrarian bets like TEVA demonstrates that he continues to embrace both discipline and courage in his investing.

For students of investing, Einhorn’s portfolio remains a masterclass in how to balance conviction with adaptability. Even after decades in the spotlight, his positions still reflect the same deep research and bold thinking that defined his rise.