EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a key metric used to evaluate a company’s core profitability and broader financial performance. While it’s widely cited across earnings calls and analyst reports, it’s also one of the most misunderstood figures in financial analysis.

For investors, understanding how EBITDA reflects operational performance — separate from financing and accounting choices — is crucial to identifying true business health.

In this guide, we’ll cover:

- What is Adjusted EBITDA – a refined version of EBITDA that excludes one-time or non-core items to give a cleaner view of ongoing profitability.

- How to calculate EBITDA margin – a quick formula investors use to gauge operating efficiency as a percentage of revenue.

- Is EBITDA the same as gross profit? – a common misconception clarified by comparing their place in the income statement.

- What makes a good EBITDA margin by industry – contextual benchmarks that help investors evaluate whether a company’s margin is strong or weak relative to peers.

We’ll also touch on how EBITDA relates to cash flow, why it matters in valuations, and when to be cautious using it as a proxy for performance.

What is EBITDA?

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a widely used financial metric that measures a company’s operating performance by focusing on its core profitability. It strips out the effects of capital structure (interest), tax policy, and non-cash accounting items (depreciation and amortization), offering a clearer view of how the business performs on a purely operational basis.

EBITDA is typically calculated as:

Net Income + Interest + Taxes + Depreciation Expense + Amortization Expense

This formula allows investors to analyze a company’s performance without the noise of financing decisions or accounting conventions. As a result, EBITDA is commonly used in valuation multiples such as EV/EBITDA, making it easier to compare businesses across industries, especially those with varying capital intensity or tax environments.

What Is Adjusted EBITDA?

Adjusted EBITDA builds on the standard EBITDA calculation by excluding non-operating and non-recurring expenses that may distort a company’s true operating performance. Common adjustments include legal settlements, foreign currency losses, stock-based compensation, and other one-time costs. These exclusions aim to provide a clearer view of a company’s core profitability, making comparisons across firms more meaningful — especially when they differ in accounting methods, capital structures, or experience unusual events.

Companies typically adjust EBITDA by removing:

- Stock-based compensation

- Restructuring or reorganization costs

- Legal settlements or litigation expenses

- Foreign exchange gains or losses

- Impairment charges (e.g. goodwill write-downs)

- One-time or non-recurring expenses (e.g. acquisition-related costs)

- Gains or losses from asset sales

- Natural disaster or pandemic-related costs

- Changes in fair value of financial instruments

- Other non-operating income or expenses

Although Adjusted EBITDA is a non-GAAP financial measure, it is widely used in business valuation because it filters out accounting distortions related to depreciation, amortization, and complex tax structures. It is especially useful when analyzing companies with significant intangible assets or high capital expenditures, where GAAP net income may not fully reflect ongoing financial health.

How to Calculate EBITDA Margin

EBITDA margin is a key profitability metric that indicates how efficiently a company converts revenue into earnings from its core operations, before factoring in interest expense, taxes, or depreciation-related write-downs of tangible and intangible assets.

Formula:

EBITDA Margin = (Total Revenue / EBITDA) × 100

Example:

If a company reports $20 million in EBITDA on $100 million in revenue, the EBITDA margin is: 20 / 100 × 100 = 20%

This means that for every dollar of revenue, 20 cents represent operating profits before non-cash expenses and financial adjustments.

EBITDA margin is a powerful measure of profitability in cost-benefit analysis, often tracked in Power BI dashboards and Business Intelligence platforms like Power Platform or Power Apps for real-time decision-making.

Is EBITDA the Same as Gross Profit?

No — EBITDA and gross profit are distinct metrics that serve different analytical purposes.

While gross profit focuses solely on production efficiency not taking into consideration administrative expenses, EBITDA provides a broader view of a company’s overall operational profitability, capturing performance before financing costs and non-cash accounting items.

Key Differences:

Metric | Gross Profit | EBITDA |

Focus | Production profitability | Operational profitability |

Formula | Revenue – Cost of Goods Sold (COGS) | Net Income + Interest + Taxes + Depreciation + Amortization |

Includes | Only direct production costs | All operating expenses excluding D&A |

Excludes | Overhead, SG&A, admin costs | Depreciation, amortization, and non-operating expenses |

Where gross profit highlights efficiency at the production level, EBITDA gives a more comprehensive picture by incorporating overhead and other operating expenses, making it a more relevant metric for assessing core business performance and cash flow potential.

What Is a Good EBITDA Margin by Industry?

There is no universal benchmark for a “good” EBITDA margin — it varies significantly by sector due to differences in capital intensity, pricing power, competitive dynamics, and fixed cost structures. Some industries naturally operate with high EBITDA margins due to scalable models or recurring revenue, while others face structural margin limitations.

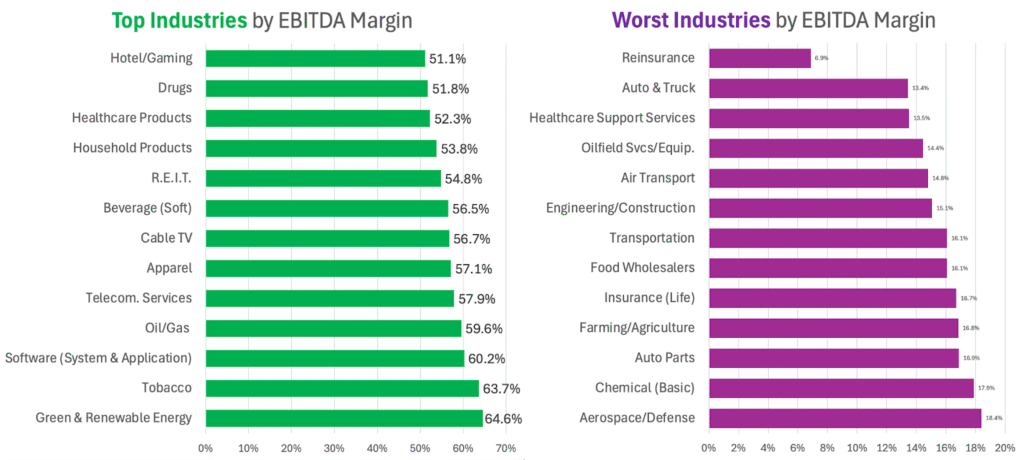

According to data from NYU Stern (January 2025), the average EBITDA margin across all industries is approximately 32.2%, with the range extending from under 10% in sectors like Reinsurance to over 60% in Green & Renewable Energy and Tobacco.

Sample Industry EBITDA Margins (2025):

- Green & Renewable Energy: 64.6%

- Tobacco: 63.7%

- Software (System & Application): 60.2%

- Oil & Gas: 59.6%

- Telecom Services: 57.9%

- REITs: 54.8%

- Healthcare Products: 52.3%

- Railroads (Transportation): 46.8%

- Semiconductors: 39.1%

- Education: 38.4%

- Retail (General): 29.7%

- Restaurants/Dining: 30.6%

- Construction Supplies: 26.6%

- Auto & Truck: 13.4%

- Reinsurance: 6.9%

When evaluating EBITDA margins, it’s critical to compare a company to its industry peers rather than to an absolute standard. High EBITDA margins often signal strong operational leverage and pricing power — but context is key. A 20% margin may be exceptional in transportation, while it would be below average in software.

Investors should also monitor margin trends over time and compare performance against peer averages, not just one-off results. Sustained EBITDA margin expansion often reflects durable business quality, not just cyclical tailwinds.

Why EBITDA Is a Valuable Tool

EBITDA is widely used as a proxy for operating cash flow, allowing investors, lenders, and analysts to assess a company’s ability to service debt, fund capital expenditures, and reinvest in its core operations. It strips out non-operating and non-cash items, making it particularly useful in evaluating performance without the noise of financing decisions or accounting conventions.

Unlike net income, EBITDA standardizes profitability across companies and industries, especially those with differing capital structures, tax treatments, or depreciation schedules. It helps mitigate the impact of variables like amortization of intangible assets, asset sales, or restructuring charges that can obscure underlying business performance.

In valuation, capital budgeting, and credit analysis, EBITDA remains a key metric for benchmarking financial health and operational efficiency.

Real-World Context: EBITDA in Practice

Warren Buffett has famously cautioned against overreliance on EBITDA, noting that it can sometimes present an overly optimistic view of a company’s financial health. By excluding critical expenses like capital expenditures, interest, and taxes, EBITDA may understate the true cost of doing business, particularly in capital-intensive industries or those carrying significant debt.

In strategic and economic analysis, EBITDA continues to play a central role in evaluating sector resilience, competitive positioning, and capital efficiency. Thought leaders such as Edward Alden and Matthew P. Goodman have emphasized that overlooking such performance metrics can weaken policy and investment frameworks meant to support industrial competitiveness and long-term productivity.

The growing influence of artificial intelligence and digital transformation has also challenged traditional interpretations of EBITDA. As companies increasingly invest in software, cloud infrastructure, and intangible assets, the conventional depreciation and amortization schedules may fail to capture the economic reality of those investments. This can lead to EBITDA overstating profitability by ignoring the true cost and pace of technological reinvestment—an important consideration for investors evaluating the sustainability of earnings in innovation-driven sectors.

EBITDA is particularly influential in private equity, mergers and acquisitions, and credit analysis, where decision-makers prioritize normalized earnings to assess deal quality or debt serviceability. In these contexts, EBITDA acts as a common language between buyers, sellers, and lenders to evaluate a company’s core performance stripped of non-operating noise. While not a perfect measure, its consistency and simplicity make it a cornerstone in deal valuation, especially when comparing companies across capital structures and tax jurisdictions.

Final Thoughts

EBITDA remains a powerful tool for evaluating business performance, especially when analyzing core profitability and operational efficiency. By excluding interest, taxes, and non-cash accounting items, it allows investors and analysts to focus on a company’s ability to generate earnings from its regular operations.

However, EBITDA should not be used in isolation. It does not reflect capital expenditures, working capital requirements, or financing costs. To gain a complete picture of financial health, EBITDA should be considered alongside metrics such as net income, free cash flow, and cash flow from operations.

When used appropriately, EBITDA can provide meaningful insights that support better financial decisions. It remains a useful benchmark in a wide range of contexts, from investment analysis to performance tracking and valuation.