The Ken Fisher portfolio in Q3 2025 reflects a demanding but durable belief: investing works best when it is treated as a long-term process rather than a sequence of decisive moments. With more than $276 billion invested across public markets, this portfolio is built to grow steadily, adjust calmly, and stay invested through changing conditions instead of reacting to them.

Ken Fisher has spent decades studying how markets behave across full cycles and how investor behavior often undermines long-term results. His portfolios are not constructed to forecast the next economic outcome or market move. They are designed to remain aligned with global growth over time while avoiding the emotional and structural mistakes that most investors repeat.

That mindset has been shaped by experience. Fisher has written a continuous market column since the early 1980s, giving him direct exposure to multiple bull markets, crashes, and recoveries. Seeing how expectations, fear, and optimism evolve across cycles has influenced how his portfolios are built today.

The Q3 2025 portfolio reflects that thinking clearly. It is broad by design, patient in execution, and intentionally diversified across sectors and regions. The objective is not to identify a single perfect investment, but to own many strong businesses and allow time and compounding to do the real work.

This approach sits firmly within long-only investing. Fisher Asset Management owns companies outright, holds them for extended periods, and relies on the steady growth of earnings and productivity to drive results. Trading activity is present, but it serves to maintain balance and alignment, supporting the portfolio’s structure rather than defining its returns.

In the sections that follow, we break down the Q3 2025 Ken Fisher portfolio in detail. We examine his top 15 holdings, explain why large-scale diversification is central to his strategy, and highlight the most meaningful adds and cuts of the quarter. We also connect these decisions back to Fisher’s broader investment philosophy and how it shows up in practice.

Key Takeaways

- Designed for long-term compounding. The portfolio is long-only and long-term, relying on business growth and time rather than forecasts, leverage, or tactical trading.

- Diversification is central to risk management. With over 1,000 holdings, risk is managed through breadth and balance, not concentration in a single idea or theme.

- Portfolio changes support structure and alignment. Additions and reductions are used to manage position size and overall exposure while keeping the long-term approach intact.

What Fisher Investments Actually Is (and Is Not)

Fisher Asset Management is not a hedge fund. This distinction matters.

The firm’s core strategies are long-only equities and multi-asset portfolios built around long-term ownership. Portfolio returns are primarily driven by exposure to business earnings, productivity, and economic growth over time rather than by frequent trading or tactical positioning.

Fisher Investments does not run structurally short or leveraged strategies as a source of return. Tools such as fixed income allocations and, in limited cases, derivatives may be used for portfolio implementation or risk management, but they are not central to how returns are generated.

Key characteristics of Fisher Investments:

- Predominantly long-only equity and asset allocation strategies

- No structural reliance on short selling

- Limited and non-core use of leverage or derivatives

- Broad diversification across sectors and regions

- Long holding periods

- Global investment scope

This structure places emphasis on portfolio construction and discipline. Individual positions are expected to perform differently over time, and some will disappoint. The approach assumes that long-term growth in earnings and productivity, combined with diversification and patience, remains the most reliable path to compounding capital.

The Core of Fisher’s Philosophy: Markets Are Behavioral Systems

Ken Fisher has built his investment philosophy around a simple observation drawn from decades of market history: markets are shaped as much by human behavior as by fundamentals. In the short term, prices are influenced by emotion, storytelling, fear, confidence, and crowd behavior. Investors react to headlines, extrapolate recent trends, and anchor on narratives that feel convincing in the moment.

Over longer periods, however, Fisher believes a different force takes over. Markets begin to reflect real economic progress. Productivity improves, businesses grow earnings, innovation spreads, and capital flows toward companies that create value. Time allows fundamentals to matter again.

This gap between short-term behavior and long-term outcomes sits at the center of Fisher’s thinking.

One idea he has repeated consistently in his writing and interviews captures it clearly:

“Stocks don’t move on what happens. They move on whether reality is better or worse than what investors already expected.”

This is more than a quote. It is a framework for how portfolios are built.

If prices already reflect what investors expect, then the biggest risk is not being wrong about the future, but being aligned with what everyone already believes. Fisher’s approach is designed to avoid that trap.

As a result, several patterns show up consistently in his portfolio construction:

- He avoids trying to predict macro events. Economic forecasts, interest rate paths, and political outcomes are uncertain and often already priced in. Fisher prefers not to anchor portfolios to predictions that can easily fail.

- He avoids concentration in single narratives. When a theme becomes dominant, expectations tend to rise faster than reality. Broad exposure reduces reliance on any one story playing out exactly as imagined.

- He avoids reacting to news cycles. Short-term headlines often amplify emotion rather than information. Fisher’s portfolios are structured to remain stable through periods of optimism and fear.

- He focuses on exposure to positive surprise. By owning a wide range of businesses across sectors and regions, the portfolio increases the likelihood that some holdings will exceed expectations, even if others fall short.

This philosophy explains why Fisher does not need to identify the single company that will define the future. He does not need perfect foresight. He needs diversified exposure to economic progress wherever it emerges.

In that sense, his portfolio is less a set of predictions and more a framework for participating in growth while minimizing the cost of being wrong.

Portfolio Overview: Q3 2025

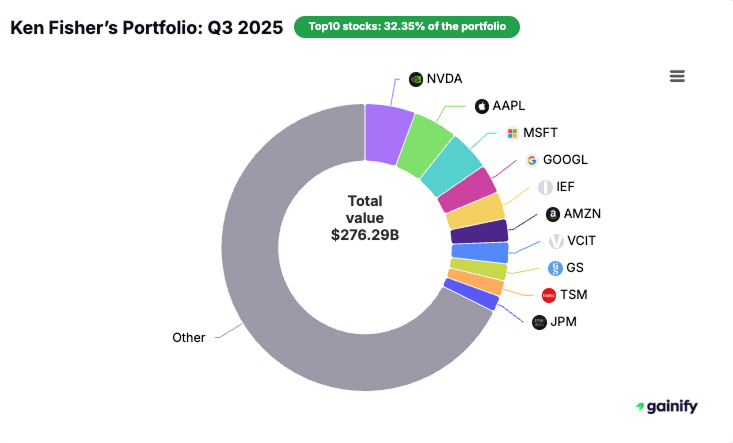

As of Q3 2025, Fisher Asset Management reported:

- Total reported equity value: $276.29 billion

- Number of public equity holdings: 1,014

- Average holding period: 21 quarters

- Top 10 holdings: ~32.35% of portfolio value

- Five-year cumulative performance: ~77%

These numbers tell you something important. This portfolio is not optimized for maximum upside in any single year. It is optimized to avoid catastrophic errors, survive drawdowns, and participate consistently in long-term equity growth.

Even within a portfolio holding more than 1,000 securities, capital still concentrates around a group of businesses that Fisher Asset Management has owned for years, often decades. These positions combine scale, durability, and long-term economic relevance, and many show holding periods exceeding 40 to 50 quarters. Together, the top 15 holdings account for a meaningful share of portfolio value while remaining individually modest in size, consistent with Fisher’s diversification-first approach.

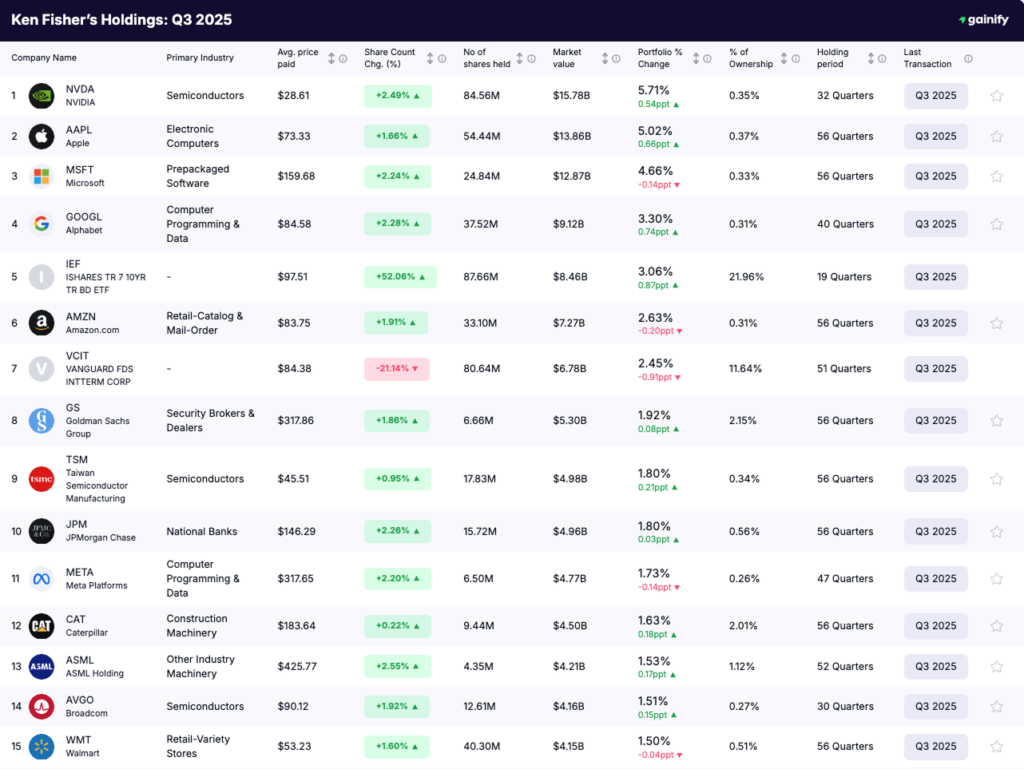

1. NVIDIA (NASDAQ:NVDA)

- Portfolio weight: 5.71%

- Market value: $15.78B

- Holding period: 32 quarters

- Portfolio change (Q3): +0.54 ppt

NVIDIA is the largest position in the portfolio and one of the few holdings with a weight above 5%. The position reflects long-term exposure to computing infrastructure and productivity growth rather than a short-term technology cycle. The incremental increase in Q3 suggests continued confidence without aggressive sizing.

2. Apple (NASDAQ:AAPL)

- Portfolio weight: 5.02%

- Market value: $13.86B

- Holding period: 56 quarters

- Portfolio change (Q3): +0.66 ppt

Apple has been held for more than 14 years, making it one of the longest-standing core positions. It represents global consumer scale, pricing power, and sustained cash generation. The added exposure in Q3 reinforces its role as a structural holding.

3. Microsoft (NASDAQ:MSFT)

- Portfolio weight: 4.66%

- Market value: $12.87B

- Holding period: 56 quarters

- Portfolio change (Q3): –0.14 ppt

Microsoft remains a core holding tied to enterprise software and cloud infrastructure. The slight reduction appears to be position management rather than a change in long-term view.

4. Alphabet (NASDAQ:GOOGL)

- Portfolio weight: 3.30%

- Market value: $9.12B

- Holding period: 40 quarters

- Portfolio change (Q3): +0.74 ppt

Alphabet provides long-term exposure to AI, advertising, and digital infrastructure. The sizable increase in portfolio weight during Q3 highlights renewed confidence in its long-term earnings power.

5. iShares 7–10 Year Treasury Bond ETF (IEF)

- Portfolio weight: 3.06%

- Market value: $8.46B

- Holding period: 19 quarters

- Portfolio change (Q3): +0.87 ppt

IEF is the largest non-equity holding among the top positions. Its significant increase during the quarter reflects portfolio-level risk balancing rather than a directional view on rates.

6. Amazon (NASDAQ:AMZN)

- Portfolio weight: 2.63%

- Market value: $7.27B

- Holding period: 56 quarters

- Portfolio change (Q3): –0.20 ppt

Amazon has been held for over a decade and remains a core exposure to commerce, logistics, and cloud services. The modest trim suggests sizing discipline, not reduced conviction.

7. Vanguard Intermediate-Term Corporate Bond ETF (VCIT)

- Portfolio weight: 2.45%

- Market value: $6.78B

- Holding period: 51 quarters

- Portfolio change (Q3): –0.91 ppt

VCIT complements IEF by adding corporate credit exposure. The large reduction in Q3 indicates rebalancing within fixed income rather than a shift away from bonds entirely.

8. Goldman Sachs (NYSE:GS)

- Portfolio weight: 1.92%

- Market value: $5.30B

- Holding period: 56 quarters

- Portfolio change (Q3): +0.08 ppt

Goldman Sachs reflects long-term exposure to global capital markets. The position has been held through multiple financial cycles, underscoring its role as a durable financial holding.

9. Taiwan Semiconductor Manufacturing (NYSE:TSM)

- Portfolio weight: 1.80%

- Market value: $4.98B

- Holding period: 56 quarters

- Portfolio change (Q3): +0.21 ppt

TSM provides essential semiconductor manufacturing exposure and has been held for more than a decade, reinforcing its role as infrastructure rather than a cyclical trade.

10. JPMorgan Chase (NYSE:JPM)

- Portfolio weight: 1.80%

- Market value: $4.96B

- Holding period: 56 quarters

- Portfolio change (Q3): +0.03 ppt

JPMorgan represents scale, balance sheet strength, and institutional durability within financials. Positioning has remained stable over time.

11. Meta Platforms (NASDAQ:META)

- Portfolio weight: 1.73%

- Market value: $4.77B

- Holding period: 47 quarters

- Portfolio change (Q3): –0.14 ppt

Meta has been held for nearly 12 years. The slight reduction reflects portfolio management while maintaining long-term exposure to digital advertising platforms.

12. Caterpillar (NYSE:CAT)

- Portfolio weight: 1.63%

- Market value: $4.50B

- Holding period: 56 quarters

- Portfolio change (Q3): +0.18 ppt

Caterpillar anchors industrial and infrastructure exposure, benefiting from long-term global investment cycles.

13. ASML Holding (NASDAQ:ASML)

- Portfolio weight: 1.53%

- Market value: $4.21B

- Holding period: 52 quarters

- Portfolio change (Q3): +0.17 ppt

ASML’s role as a critical supplier to the semiconductor industry makes it a long-duration holding aligned with technological progress.

14. Broadcom (NASDAQ:AVGO)

- Portfolio weight: 1.51%

- Market value: $4.16B

- Holding period: 30 quarters

- Portfolio change (Q3): +0.15 ppt

Broadcom combines semiconductor exposure with stable software revenues, fitting well within Fisher’s preference for diversified cash flow profiles.

15. Walmart (NASDAQ:WMT)

- Portfolio weight: 1.50%

- Market value: $4.15B

- Holding period: 56 quarters

- Portfolio change (Q3): –0.04 ppt

Walmart provides defensive consumer exposure at global scale and has been a long-standing holding through multiple economic cycles.

Q3 2025 Transactions: What the Changes Really Signal

In a portfolio of this size, activity needs to be interpreted carefully. With more than $276 billion invested, most quarterly trades are incremental by necessity. The transactions that matter are the ones involving large amounts of capital, where position size and portfolio balance are meaningfully adjusted.

Meaningful Adds (Over $50 Million)

- iShares 7–10 Year Treasury Bond ETF (IEF): ~$2.87B added

- NVIDIA (NVDA): ~$358M added

- Suncor Energy (SU): ~$287M added

- Microsoft (MSFT): ~$278M added

- Apple (AAPL): ~$200M added

These additions build on existing positions rather than introduce new themes. The largest increase went to IEF, reinforcing the role of fixed income in overall portfolio balance. Additions to NVIDIA, Microsoft, and Apple reflect continued emphasis on large, durable businesses with long-term earnings power. The increase in Suncor Energy adds incremental exposure to energy within a diversified framework.

Meaningful Cuts (Over $50 Million)

- Vanguard Intermediate-Term Corporate Bond ETF (VCIT): ~$1.80B reduced

- Canadian Natural Resources (NYSE:CNQ): ~$205M reduced

- Intuit (NASDAQ:INTU): ~$177M reduced

- Adobe (NASDAQ:ADBE): ~$120M reduced

These reductions reflect position sizing and portfolio-level risk management rather than a loss of confidence in the underlying businesses. In each case, meaningful exposure remains. The large trim to VCIT, in particular, appears to be a rebalancing decision within fixed income rather than a shift away from bonds as a whole.

New Positions and Full Exits

Q3 2025 also included new buys and complete sell-offs, but these were small relative to total assets under management. As a result, they do not materially alter the portfolio’s structure or long-term direction. These changes are best understood as opportunistic adjustments rather than signals of a broader strategic shift.

What This Portfolio Ultimately Teaches

Ken Fisher’s Q3 2025 portfolio is not about brilliance. It is about the process.

It assumes:

- You cannot predict the future with precision.

- Markets will overreact emotionally.

- Innovation will continue unevenly.

- Time rewards discipline more than insight.

For a young investor, the lesson is profound and simple:

You do not need to outsmart the market. You need to structure your behavior so the market cannot outsmart you.

This portfolio is calm by design. That calmness is not passive. It is engineered.