Leon Cooperman is not an investor who needs to chase relevance. After more than five decades in markets, his reputation was built long before speed, leverage, and narratives became dominant forces in investing. He is known for thinking independently, speaking plainly, and remaining willing to look wrong in the short term if the long-term math makes sense. While many managers adapt their style to what the market rewards at a given moment, Cooperman has spent his career doing the opposite, trusting valuation, cash flow, and patience even when they fall out of favor.

That mindset is clearly visible in how he allocates capital today. His Q3 2025 portfolio reflects the behavior of an investor who has already lived through multiple booms and busts and understands where excess eventually leads. With roughly 3.20 billion dollars invested across 41 public equities, this is not a portfolio designed to follow trends. It is designed to endure cycles.

The structure reinforces that intent. Nearly 68 percent of total value is concentrated in the top ten holdings, and the average holding period is about 15 quarters, a rare level of commitment in modern institutional investing. This long-term approach has produced results. Over the past five years, the portfolio has delivered cumulative gains of more than 160 percent, despite extended periods when value-oriented strategies were widely dismissed.

Activity in Q3 2025 shows conviction rather than hesitation. Cooperman deployed close to 180 million dollars into Tesla, made a substantial investment in Exact Sciences, and added selectively to semiconductors through AMD and Teradyne. At the same time, he exited Fiserv completely and trimmed several existing positions.

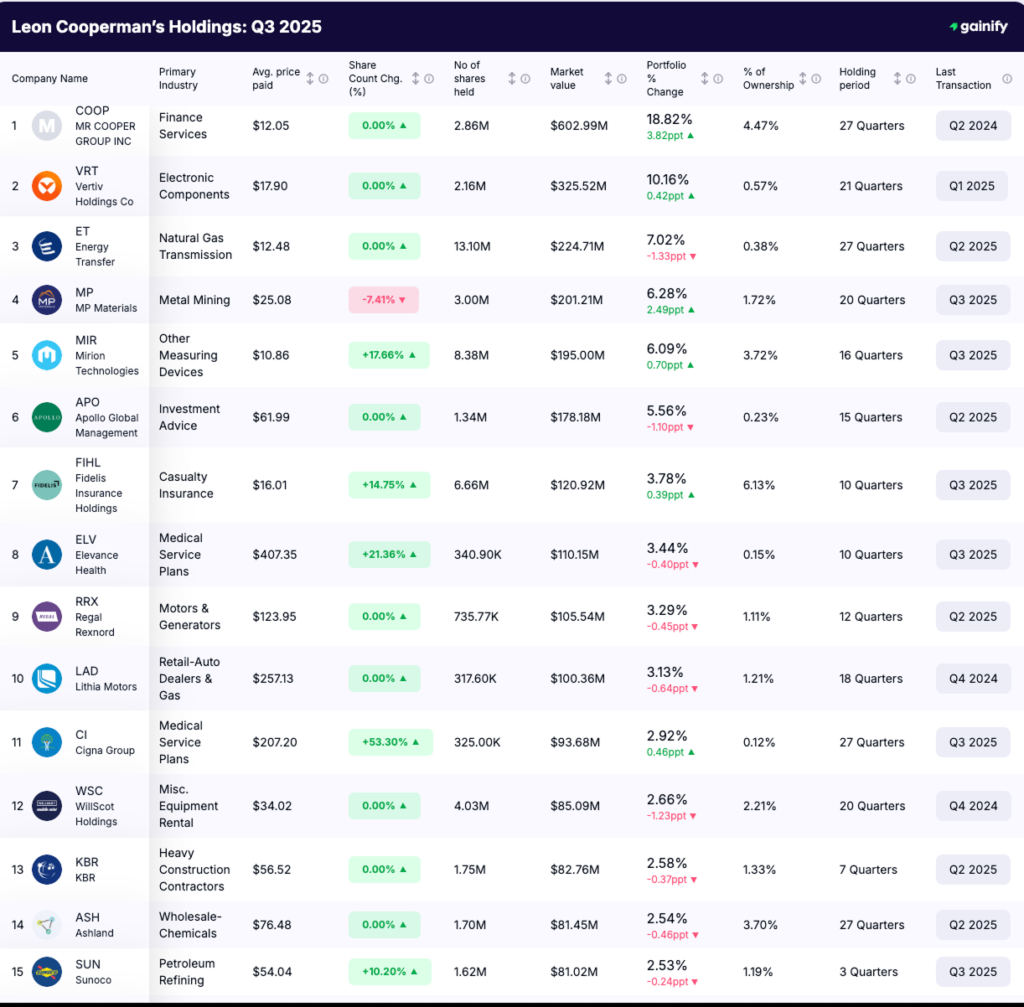

The largest holdings tell a consistent story. MR Cooper Group, Vertiv Holdings, and Energy Transfer anchor the portfolio, reflecting a preference for cash-generating businesses, infrastructure, and financial systems that sit at the core of the real economy. The individual names evolve, but the philosophy remains unchanged.

What follows is a closer look at Leon Cooperman’s investment philosophy and how it is being expressed, position by position, in his Q3 2025 portfolio.

Who Is Leon Cooperman and What Is His Investment Style

Leon G. Cooperman is one of the longest tenured and most recognizable value investors in U.S. markets. His career spans more than five decades, beginning at Goldman Sachs in 1967, where he ultimately rose to partner and served as chairman and CEO of Goldman Sachs Asset Management. During his 25 years at the firm, Cooperman built a reputation as a rigorous fundamental analyst, known internally for challenging consensus views and focusing relentlessly on valuation.

In 1991, he left Goldman to found Omega Advisors, a hedge fund that would become closely associated with concentrated, research-driven investing. Omega was never built as a high-turnover trading operation. Instead, it focused on owning businesses where Cooperman believed intrinsic value materially exceeded market price. At its peak, Omega managed more than 10 billion dollars, and for much of its history, it ranked among the more influential fundamentally driven hedge funds in the industry. In 2018, Cooperman converted Omega into a family office, citing regulatory burden and a desire to manage only long-term capital.

At the core of Cooperman’s investment philosophy is a traditional definition of value. He emphasizes intrinsic value, sustainable free cash flow, balance sheet strength, and management discipline. He has consistently argued that price matters as much as quality, and that even great businesses can be poor investments if purchased without a margin of safety.

Risk, in Cooperman’s framework, is not volatility. It is the possibility of permanent capital loss. This distinction is central to understanding his portfolios. It explains why positions are often large, why holding periods are long, and why he is willing to appear early or wrong in the short term. Cooperman has repeatedly stated that time is an ally when fundamentals are sound and valuation is supportive.

He has summarized this thinking in a line he has used publicly for years, including in interviews with CNBC: “The stock market is a market of stocks, not a stock market.”

The point is not rhetorical. It reflects his belief that broad indices, macro narratives, and momentum cycles matter far less than company-specific economics over time. For Cooperman, returns are created by buying individual businesses at discounts to intrinsic value, not by forecasting where the market will trade next quarter.

This philosophy remains clearly visible in his current portfolio. Concentration, patience, and selective aggression are not tactical choices. They are structural features of how he has always invested.

Leon Cooperman Portfolio Overview: Q3 2025

As of Q3 2025, Omega Advisors reported:

- Total equity value: 3.20 billion dollars

- Number of holdings: 41

- Average holding period: ~15 quarters

- Top 10 concentration: ~67.6% of portfolio value

- Five year performance: +160% cumulative

Core Holdings and Portfolio Anchors: Top 5 Positions

The top five holdings in Leon Cooperman’s Q3 2025 portfolio represent the structural core of the strategy. Together, they account for just under 50 percent of total equity value, and each position has been sized and held with long-term conviction. These are not tactical trades. They are the foundation around which the rest of the portfolio is built.

1. MR Cooper Group (COOP)

- Portfolio weight: 18.8%

- Estimated position value: ~600 million dollars

- Holding period: 6+ years

- Sector exposure: Financial services, mortgage servicing

- Investment rationale: Recurring fee income, asset sensitivity, and durable cash flow generation across interest rate cycles

MR Cooper Group remains the dominant holding by a wide margin. The extended holding period and position size suggest that Cooperman views the company as structurally undervalued relative to its earnings power and balance sheet optionality.

2. Vertiv Holdings (NYSE: VRT)

- Portfolio weight: ~10.2%

- Estimated position value: ~325 million dollars

- Holding period: 4+ years

- Sector exposure: Industrial infrastructure, data centers

- Investment rationale: Mission-critical power and cooling systems with long-term demand tied to data growth rather than software multiples

Vertiv offers exposure to digital infrastructure through tangible assets and services, aligning with Cooperman’s preference for cash-generative businesses with visible demand.

3. Energy Transfer (NYSE: ET)

- Portfolio weight: ~7.1%

- Estimated position value: ~225 million dollars

- Holding period: 5+ years

- Sector exposure: Energy infrastructure, pipelines

- Investment rationale: Stable cash flows, distribution yield, and essential energy transport assets

Despite modest trimming, Energy Transfer remains a core holding, functioning as a cash flow anchor within the portfolio.

4. MP Materials (NYSE: MP)

- Portfolio weight: ~6.4%

- Estimated position value: ~205 million dollars

- Holding period: 3+ years

- Sector exposure: Materials, rare earth mining

- Investment rationale: Strategic asset base, limited domestic competition, long-term supply relevance

The position has been reduced incrementally, but its continued size indicates ongoing confidence in the long-term asset value despite near-term volatility.

5. Mirion Technologies (NYSE: MIR)

- Portfolio weight: ~5.8%

- Estimated position value: ~185 million dollars

- Holding period: 4+ years

- Sector exposure: Industrial technology, nuclear and radiation detection

- Investment rationale: Niche market leadership, regulatory barriers, and long-duration contracts

Mirion rounds out the top five as a specialized industrial holding with defensible positioning and predictable demand.

The Biggest Moves in Q3 2025

Q3 2025 was defined by capital concentration rather than broad repositioning. Omega Advisors made a small number of high-impact decisions, reallocating meaningful capital where conviction strengthened while exiting or trimming positions where the risk-reward balance had shifted.

Adds: Increasing Exposure to High-Conviction Ideas

Q3 2025 additions were concentrated in a small number of positions, with capital deployed decisively rather than incrementally.

Cigna Group (NYSE: CI)

- Shares added: ~113,000

- Change vs prior quarter: +53.3%

- Capital deployed: ~33.4 million dollars

Cigna Group was the largest capital add among these four names. The increase meaningfully raised exposure to managed healthcare, lifting the position’s portfolio weight by roughly 0.46 percentage points. The scale of the purchase points to confidence in valuation and cash flow durability rather than short-term positioning.

Mirion Technologies (NYSE: MIR)

- Shares added: ~1.26 million

- Change vs prior quarter: +17.7%

- Capital deployed: ~27.2 million dollars

Mirion Technologies saw a sizable share accumulation, reinforcing its role as a core industrial technology holding. The add increased portfolio weight by about 0.70 percentage points, signaling continued conviction in Mirion’s niche leadership in radiation detection and nuclear-related markets.

Elevance Health (NYSE: ELV)

- Shares added: ~60,000

- Change vs prior quarter: +21.4%

- Capital deployed: ~18.7 million dollars

Elevance Health was increased despite a slight decline in overall portfolio weight due to relative price movement. The added shares suggest sustained confidence in the company’s long-term earnings power, scale advantages, and defensive characteristics within managed care.

GE HealthCare Technologies (NASDAQ: GEHC)

- Shares added: ~200,000

- Change vs prior quarter: +50.0%

- Capital deployed: ~14.9 million dollars

GE HealthCare Technologies experienced a sharp expansion in share count, boosting portfolio exposure by approximately 0.37 percentage points. The move reflects a valuation-driven increase in medical technology exposure tied to diagnostic equipment and healthcare infrastructure with durable demand.

New Buys: Selective and Intentional

New positions were few, reinforcing the portfolio’s conviction-driven structure.

Amrize Ltd (NYSE: AMRZ)

- Shares acquired: ~1.2 million

- Initial position value: ~45 million dollars

This new position added industrial materials exposure and fits within the portfolio’s broader infrastructure and real-assets tilt.

Occidental Petroleum (NYSE: OXY)

- Shares acquired: ~420,000

- Initial position value: ~15 million dollars

The position was sized conservatively and aligns with long-standing interest in energy assets with free cash flow leverage.

Sold Outs: Capital Recycled Decisively

Fiserv (NASDAQ: FISV)

- Shares sold: ~410,000

- Position reduction: 100%

- Capital realized: ~56 million dollars

Fiserv was exited entirely, representing the most decisive portfolio reduction of the quarter and a clear reassessment of opportunity cost within financial technology.

Cuts: Trimming Without Abandoning the Thesis

Reductions in Q3 were targeted and measured, aimed at managing risk rather than exiting core ideas.

OneMain Holdings (NYSE: OMF)

- Shares reduced: ~1.1 million

- Change vs prior quarter: –26%

- Capital reduced: ~48 million dollars

The trim lowered exposure to consumer credit while maintaining a meaningful remaining position.

MP Materials (NYSE: MP)

- Shares reduced: ~1.4 million

- Change vs prior quarter: –12%

- Capital reduced: ~36 million dollars

Despite the reduction, MP Materials remains a top-five holding, indicating profit management rather than a thesis reversal.

Arbor Realty Trust (NYSE: ABR)

- Shares reduced: ~1.6 million

- Change vs prior quarter: –18%

- Capital reduced: ~21 million dollars

The trim reflects portfolio risk balancing amid broader real estate exposure.

What These Moves Tell Us

The Q3 2025 transactions show clear prioritization of capital. Large dollar adds were paired with meaningful share accumulation in a few high-conviction names, while cuts and exits were executed decisively where upside appeared more limited.

This pattern reinforces a consistent Cooperman trait. He does not rebalance for appearances. He reallocates when valuation changes. The numbers show a portfolio that is actively managed, but never overmanaged, with every share change tied to conviction rather than noise.