Daniel Loeb has built his reputation as one of the most formidable investors in global markets by combining conviction with control. As the founder of Third Point, he is known for deploying capital aggressively when opportunity presents itself, while simultaneously hedging downside risk with equal intent. Loeb is not a pure buyer of assets. He is a portfolio constructor who balances exposure, catalysts, and protection in real time.

That balance is clearly visible in Q3 2025. While Third Point increased equity exposure to its highest level in roughly three years, Loeb did not abandon risk management to do it. Alongside large new equity positions and aggressive adds, the portfolio also carried a massive S&P 500 put position with a notional value approaching 600 million dollars, a reminder that this was not a blind bet on rising markets, but a structured expression of conviction with downside insurance.

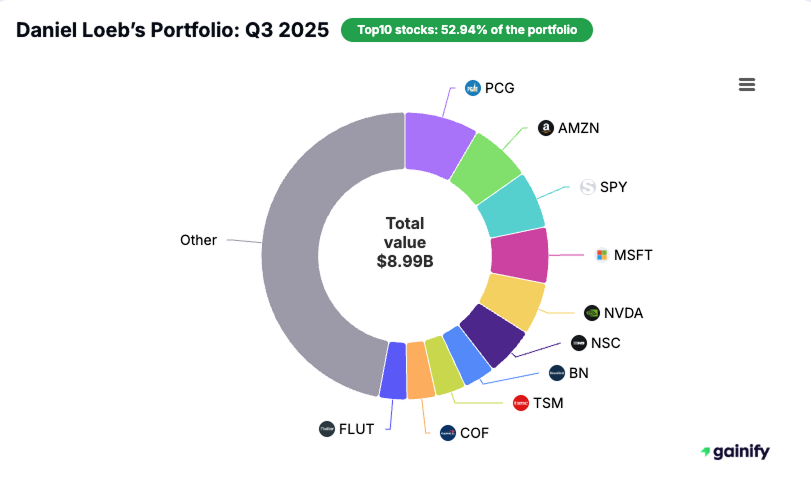

As of Q3 2025, Third Point reported approximately 8.99 billion dollars in public equities across 46 positions, with an average holding period of about five quarters. Equity exposure rose sharply through direct stock purchases, while the SPY put hedge provided protection against adverse market moves. Capital was deployed decisively, but not without safeguards.

This is what differentiates Loeb at moments like this. He is willing to lean in when the opportunity set expands, but he rarely does so without a hedge in place. Q3 2025 is not just about increased exposure. It is about how that exposure was built.

Key Highlights

- Equity exposure rose to a three-year high, reflecting increased conviction while maintaining downside protection through index hedges

- Capital was deployed at scale into large new positions and materially expanded core holdings

- Decisive exits and targeted cuts funded higher-impact opportunities and actively reshaped portfolio risk

Who Is Daniel Loeb and Why His Positioning Matters

Daniel Loeb founded Third Point in 1995 and built it into one of the most influential activist and event-driven investment firms in global markets. His investing career began in distressed credit, a background that still shapes how he evaluates risk, downside protection, and capital structure today. Unlike managers who operate exclusively in equities, Loeb has always approached investing with a multi-asset mindset, moving fluidly between credit, equities, derivatives, and special situations depending on where mispricing is most evident.

Over the years, Third Point has become closely associated with activism, but activism is only one expression of Loeb’s broader approach. At its core, his strategy is about identifying inflection points. Corporate change, balance sheet repair, asset sales, operational improvements, regulatory shifts, or strategic missteps that can be corrected. Loeb is willing to engage publicly with management and boards when he believes value is being constrained, but he is just as willing to act quietly when catalysts are already in motion.

What distinguishes Loeb from long-only managers is his view of time and risk. He does not rely on duration alone to generate returns. Instead, he looks for situations where timing matters and where the path to value realization is visible. When those conditions align, position sizing tends to be decisive, and capital is deployed quickly rather than layered in cautiously over years.

Third Point portfolios are therefore dynamic by design. Turnover is higher, holding periods are shorter, and exposure shifts meaningfully as opportunity sets expand or contract. Loeb is comfortable increasing gross exposure when he believes the probability-weighted outcome favors active capital, and just as comfortable reducing or hedging when that balance changes.

Q3 2025 reflects this approach clearly. The rise in equity exposure is not a passive response to market strength. It is a signal that Loeb sees a richer set of actionable opportunities, supported by catalysts and protected by hedges, that justify deploying capital more aggressively at this point in the cycle.

Daniel Loeb Portfolio Overview: Q3 2025

As of the Q3 2025 filing, Third Point reported a public equity portfolio valued at approximately 8.99 billion dollars, spread across 46 holdings. While the number of positions remains broadly consistent with recent quarters, the level of capital deployed into equities increased meaningfully, pushing equity exposure to its highest point in roughly three years.

This increase was not the result of passive appreciation or index drift. It came from deliberate positioning. Large new equity stakes were initiated, several existing positions were expanded aggressively, and capital was actively recycled through exits and reductions elsewhere in the portfolio. The average holding period stands at roughly five quarters, reinforcing Third Point’s event-driven orientation rather than a long-duration compounding approach.

Concentration also rose modestly at the top of the portfolio. The top ten holdings now account for just under 53% of total equity value, reflecting a shift toward fewer, higher-impact ideas. This level of concentration is intentional. When Loeb sees a dense opportunity set, he prefers to express it through size rather than breadth.

Importantly, the rise in equity exposure was paired with active risk management. Alongside long equity positions, Third Point maintained significant index hedges, including a large S&P 500 put position with a notional value approaching 600 million dollars. This structure allowed Loeb to increase gross exposure while preserving flexibility in the event of broader market dislocation.

Taken together, the Q3 2025 portfolio reflects a manager leaning into opportunity without abandoning discipline. Capital is more exposed than it has been in years, but it is exposed selectively, dynamically, and with protection in place.

The Biggest Moves in Q3 2025

Q3 2025 was one of the most active quarters for Third Point in recent years. Capital was not adjusted at the margins. It was reallocated decisively, with large new positions initiated, existing holdings expanded aggressively, and several long-standing exposures reduced or exited to fund redeployment. These moves explain both the rise in equity exposure and the shift in portfolio composition more clearly than any single holding.

New Buys: Capital Deployed at Scale

Several new positions were initiated at sizes large enough to immediately influence portfolio outcomes. These were not exploratory stakes. They were expressions of conviction.

SPDR S&P 500 ETF (SPY)

Third Point initiated a large position in SPY with an initial value of approximately 561 million dollars. This move directly increased market exposure and worked in tandem with the portfolio’s equity buildup. Importantly, it sat alongside a substantial SPY put hedge, reinforcing that this was a structured exposure rather than an unhedged directional bet.

Norfolk Southern (NYSE:NSC)

Norfolk Southern entered the portfolio as one of the largest new holdings, with an initial position valued at roughly 458 million dollars. The size reflects confidence in operational normalization and long-term asset value following a period of disruption.

Somnigroup International (NYSE:SGI)

A new position of approximately 236 million dollars was established in Somnigroup International, marking a meaningful allocation to consumer and travel-related recovery themes.

Union Pacific (NYSE:UNP)

Third Point initiated a position worth around 197 million dollars in Union Pacific, adding further exposure to North American rail infrastructure and pricing power.

MasTec (NYSE:MTZ)

MasTec was added with an initial investment of approximately 133 million dollars, reflecting interest in infrastructure, energy transition, and construction-related spending.

Together, these new positions represent a significant shift in capital toward infrastructure, industrials, and hedge against broad market exposure.

Adds: Increasing Exposure to Existing Convictions

Alongside new buys, Third Point added aggressively to several existing positions, further increasing portfolio concentration.

Microsoft (NASDAQ:MSFT)

The Microsoft position was increased by approximately 175%, with about 357 million dollars of additional capital deployed. This move elevated Microsoft into the top tier of the portfolio and signals a reassessment of long-term optionality rather than a short-term trade.

Casey’s General Stores (NASDAQ:CASY)

The position in Casey’s was increased by roughly 39%, representing an additional 73 million dollars invested. The add reflects confidence in execution, pricing power, and cash flow durability.

Meta Platforms (NASDAQ:META)

Meta saw an increase of approximately 47%, with about 52 million dollars deployed. The addition aligns with broader exposure to large-cap technology platforms where cash generation and valuation appear favorable.

Cuts: Funding New Conviction

Some of the most informative activity in Q3 came from sharp reductions in existing holdings. These cuts were meaningful and clearly linked to funding new opportunities.

Taiwan Semiconductor Manufacturing (NYSE:TSM)

The position was reduced by approximately 23%, freeing up around 81 million dollars of capital.

Apollo Global Management (NYSE:APO)

Apollo was cut by roughly 49%, with about 88 million dollars removed from the position.

Danaher (NYSE:DHR)

Danaher saw one of the sharpest reductions, with the position cut by approximately 90%, reducing exposure by around 90 million dollars.

Live Nation Entertainment (NYSE:LYV)

The Live Nation position was reduced by roughly 32%, freeing up approximately 99 million dollars.

These reductions were not incremental. They reflect a conscious decision to rotate capital away from positions where expected returns appeared less compelling relative to new opportunities.

Sold Outs: Clearing the Deck

Several positions were exited entirely during the quarter as part of broader capital reallocation.

- Corpay (NYSE:CPAY): approximately 218 million dollars realized

- Intercontinental Exchange (NYSE:ICE): approximately 170 million dollars realized

- RB Global (NYSE:RBA): approximately 78 million dollars realized

- Workday (NASDAQ:WDAY): approximately 69 million dollars realized

- DocuSign (NASDAQ:DOCU): approximately 48 million dollars realized

These exits were clean and decisive. While none individually defined the quarter, collectively they provided meaningful funding for the large new positions and aggressive adds elsewhere in the portfolio.

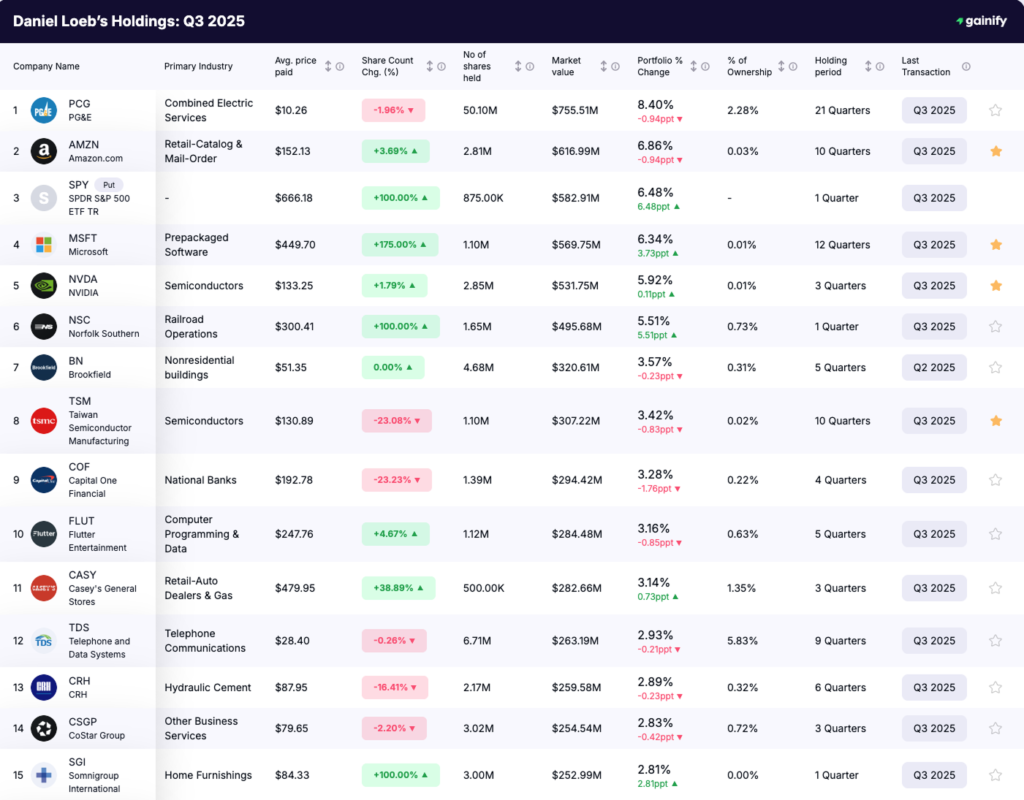

Top 10 Holdings: Daniel Loeb Portfolio Q3 2025

Even with elevated turnover and active capital rotation, Third Point’s portfolio in Q3 2025 remains meaningfully concentrated at the top. The ten largest holdings account for just under 53% of total equity value, reflecting Loeb’s preference for expressing conviction through position size rather than breadth.

These positions anchor the portfolio and provide insight into where Third Point’s highest-confidence capital is currently deployed.

1. PG&E (PCG)

- Estimated value: ~756 million dollars

- Portfolio weight: ~8.4%

PG&E remains the largest holding in the portfolio. The position reflects confidence in the utility’s restructuring progress, regulatory framework, and long-term asset value. It is a classic Third Point investment where complexity and transition create opportunity.

2. Amazon (AMZN)

- Estimated value: ~617 million dollars

- Portfolio weight: ~6.9%

Amazon continues to serve as a core exposure to global commerce and cloud infrastructure. The position provides scale, optionality, and long-duration cash flow potential within the portfolio.

3. SPDR S&P 500 ETF (SPY)

- Estimated value: ~583 million dollars

- Portfolio weight: ~6.5%

The SPY position is notable for its size and its role in portfolio construction. Rather than a standalone bullish bet, it sits alongside a substantial SPY put position with a notional value approaching 600 million dollars.

4. Microsoft (MSFT)

- Estimated value: ~570 million dollars

- Portfolio weight: ~6.3%

Microsoft moved into the top tier following a substantial increase during the quarter. The position reflects confidence in durable platform economics, recurring revenue, and long-term optionality.

5. Nvidia (NVDA)

- Estimated value: ~532 million dollars

- Portfolio weight: ~5.9%

Nvidia remains one of the portfolio’s largest technology holdings. The position offers exposure to structural demand in semiconductors and AI-related infrastructure, balanced within a diversified portfolio.

6. Norfolk Southern (NSC)

- Estimated value: ~496 million dollars

- Portfolio weight: ~5.5%

Norfolk Southern entered the portfolio as a large new position and immediately ranked among the top holdings. The size underscores confidence in normalization, pricing power, and long-term rail asset value.

7. Brookfield (BN)

- Estimated value: ~321 million dollars

- Portfolio weight: ~3.6%

Brookfield provides exposure to global real assets, infrastructure, and alternative investment management. It adds diversification while maintaining a focus on asset-heavy, cash-generative businesses.

8. Taiwan Semiconductor Manufacturing (TSM)

- Estimated value: ~307 million dollars

- Portfolio weight: ~3.4%

Despite a meaningful reduction during the quarter, TSM remains a top ten holding. The position continues to reflect confidence in its strategic importance within the global semiconductor supply chain.

9. Capital One Financial (COF)

- Estimated value: ~294 million dollars

- Portfolio weight: ~3.3%

Capital One represents exposure to consumer finance with leverage to credit normalization and improving returns on capital.

10. Flutter Entertainment (FLUT)

- Estimated value: ~284 million dollars

- Portfolio weight: ~3.2%

Flutter rounds out the top ten, offering exposure to global gaming and sports betting with scale advantages and regulatory complexity that can create mispricing.

What the Q3 2025 Portfolio Ultimately Says

The Daniel Loeb Portfolio in Q3 2025 reflects a deliberate increase in equity exposure shaped by valuation, catalysts, and risk structure. Capital was deployed at scale into situations where expected returns appeared attractive, while hedges were used to manage downside at the portfolio level. The result is a portfolio that carries higher exposure without relying on a single outcome.

The most informative feature of the quarter is the way capital moved. Large new positions in infrastructure, railroads, and index exposure were funded through clean exits and meaningful reductions elsewhere. Position sizing increased where conviction strengthened, and exposure was reduced where the opportunity set narrowed. These changes point to an active reallocation process rather than passive drift.

Risk management remains embedded in the structure. The combination of long equity positions with a substantial SPY put hedge indicates that exposure was added with explicit downside parameters. Portfolio construction reflects attention to gross and net exposure, liquidity, and flexibility as conditions evolve.

Taken together, the Q3 2025 portfolio shows an investor responding to opportunity through sizing, structure, and timing. Capital was allocated where the probability-weighted outcome improved, and protected where uncertainty remained. The portfolio reflects a focus on execution rather than prediction, with decisions grounded in positioning rather than narrative.